We’ve seen a much better start to the month of May for the Silver Miners (SIL), and not surprisingly, several of the better names in the sector have launched to new multi-year highs on the back of this strength. This significant outperformance vs. other sectors is thanks to continued strength in the price of silver (SLV), with the metal up 15% during May alone. The robust rally we’ve seen is a marked improvement from its previously negative year-to-date return heading into the month, and its massive underperformance vs. gold (GLD) in Q1. While there are several silver miners available to buy for investors, there are only a few in the sector actually worth buying, with many operating out of sub-par jurisdictions or generating almost no free-cash-flow due to their minuscule margins. Three names worth watching for investors, however, are Pan American Silver (PAAS), Silvercrest Metals (SILV), and Wheaton Precious Metals (WPM), and we’ll take a look at what makes these three so unique in this article.

While many of the miners in the sector regularly dilute shareholders and have struggled to generate positive annual earnings per share, SILV, PAAS, and WPM have produced significant returns for shareholders, and have either grown their profits or their resources exponentially. In Silvercrest Metals’ case, this is the second stint in Mexico for the company, as the company’s prior discovery, Silvercrest Metals 1.0, was bought out in 2015 for $154 million, generating a 400% plus return in less than five years for shareholders. Meanwhile, for Pan American Silver and Wheaton Precious Metals, these companies have continued to responsibly grow their annual earnings, with annual EPS sitting near all-time highs. Let’s take a look at these three names below:

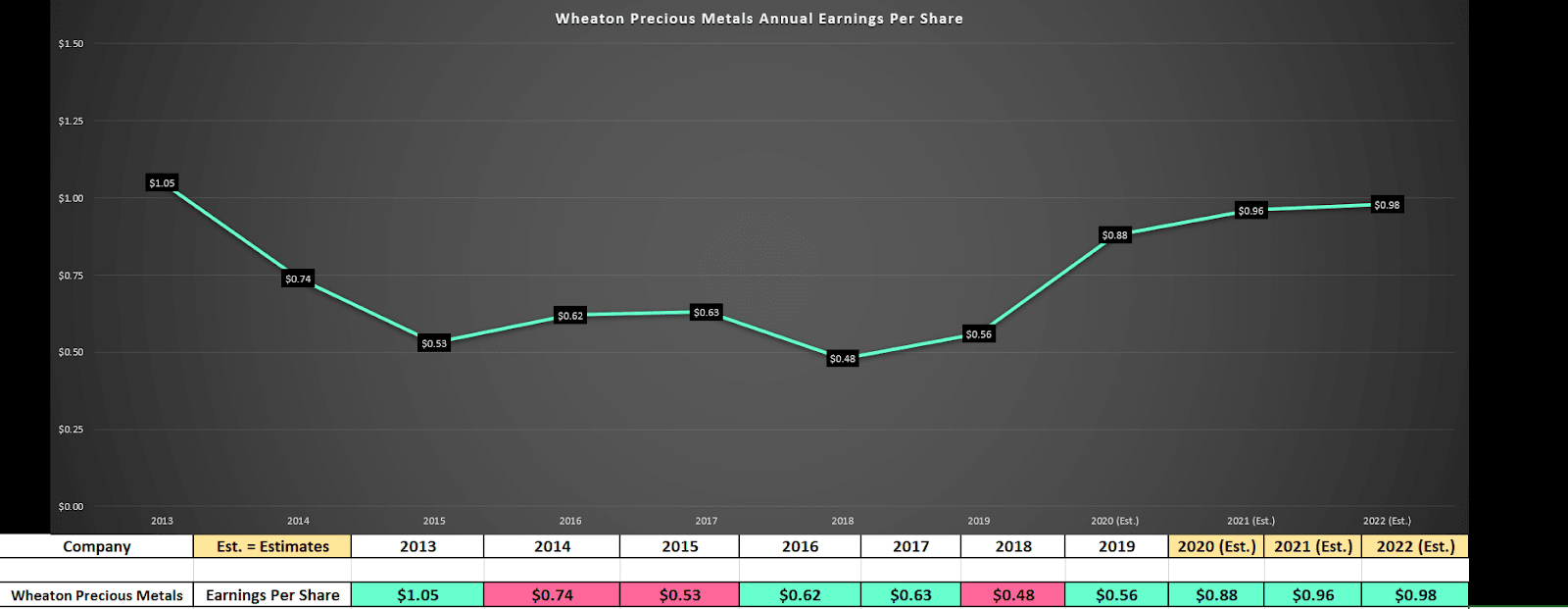

Beginning with Wheaton Precious Metals, the company is the only real large-cap royalty company with significant exposure to silver, and the royalty model is the most attractive model for investors given the high margins and low capital expenditures. While most miners require capex of $50 million to $100 million per year to replace mined ounces and upkeep their operations, Wheaton Precious Metals does not have this burden. Instead, the company provides capital to whom it believes to be the best companies in the sector, and Wheaton then takes a royalty on all ounces produced from providing this capital upfront. As we can see, this strategy is clearly paying off for the company, with annual EPS growth of 17% year last year, and expected annual EPS growth in FY-2020 of 53%. This is incredible growth for any company, let alone a $20 billion-dollar company. I believe these estimates of $0.86 in annual EPS are likely on the conservative side as well for FY-2020, assuming that metals prices remain strong as they have been. This mix of low-risk given the royalty model, industry-leading after-tax margins above 40%, and high-growth is a recipe for robust long-term returns for investors. Therefore, while the stock is getting a bit expensive here at $46.00 per share, it would begin to get very attractive below $39.00 if we could see a correction.

(Source: YCharts.com, Author’s Chart)

If we move over to Pan American Silver, we can see a healthy earnings trend, as the company should see annual EPS hit a new all-time high in FY-2020 at $0.55. The company is one of the largest primary silver producers in the sector, and assuming the company hits these forecasts; this would translate to 34% growth year-over-year. When it comes to margins, the company is a leader in the space, with all-in sustaining costs of $10.46/oz last year, more than 10% below the industry average, and a healthy margin considering silver prices have hovered near $16.00/oz the past year. The company enjoyed gross margins of 41.5% and 43.3% in the most recent two quarters, and this translated to the third quarter in a row of margin expansion, a tailwind for earnings going forward. It is worth noting that these margins were achieved despite the volatility in silver during Q1, with the metal falling below $13.00/oz briefly.

(Source: YCharts.com, Author’s Chart)

(Source: Author’s Chart)

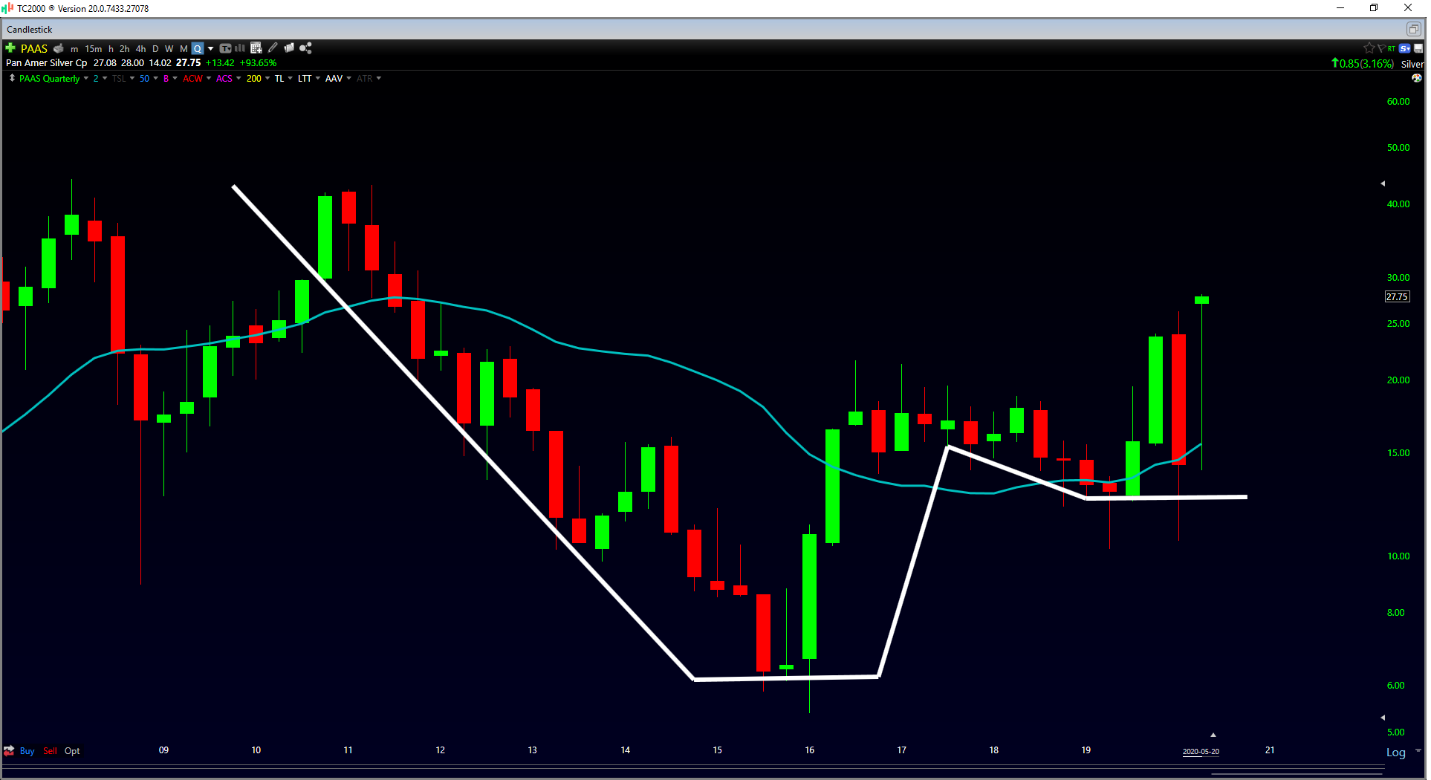

If we take a look at the technical chart of PAAS, we can see that the stock looks to be trying to build a multi-year cup base, and the stock seems to be breaking out of the handle portion of this base. This is a bullish development, as the $21.00 level has been a brick wall of resistance since $2013, and we are now back above it. Ideally, the bulls are going to want to see a close above $23.00 for the quarter-end for PAAS to confirm this breakout. However, similar to Wheaton Precious Metals, PAAS is a little extended here; therefore, I believe it would be wiser to wait for 10% pullbacks to add any exposure.

(Source: TC2000.com)

Last but not least, we have Silvercrest Metals, an exploration company in the sector with a robust balance sheet of over $175 million that’s awaiting a potential construction decision in Q3. The company has a massive high-grade resource in Mexico of over 110 million silver-equivalent ounces, and the grade on this resource comes in above 600 grams per tonne silver. The company’s Las Chispas Project is one of the highest-grade silver resources globally, not currently in production, and the Preliminary Economic Assessment last year showed incredible economics. Based on the study, we can see a very modest initial capital outlay of just $100.5 million that would generate over $135 million in after-tax free-cash-flow. It’s important to note that since this resource was completed, the company continues to make new high-grade discoveries, with recent drill intercepts of over 5000 grams per tonne silver, more than quadruple the grades of the current resource. Assuming we continue to see results like this, this would bolster the overall resource grade and allow for an even quicker payback on the initial investment.

(Source: Silvercrest Metals Company Presentation)

It’s also worth noting that while most silver companies are producing at just over $12.00/oz, Silvercrest Metals has some of the lowest costs in the industry, with projected all-in sustaining costs per silver-equivalent ounce of only $7.52 over the life of mine, and $4.89 for the first four years. I believe that these costs can come down as low as $4.00/oz for the first four years, including the discoveries, suggesting that the company could enjoy nearly 75% margins at just $16.00/oz for silver. Based on the massive exploration upside at the company’s Las Chispas Project, as well as the potential transformation from explorer to producer over the next 15 months, I see Silvercrest Metals as a low-risk, high-reward play in the sector. Ultimately, I would not be surprised to see the stock trade up to $12.25 per share by the time the miner is in production, hopefully by Q4 2021.

While the Silver Miners ETF offers many options for companies to invest in, I believe PAAS, WPM, and SILV are the three most attractive names in the sector from a risk/reward standpoint. I would not be in a rush to buy any of these names at current prices, but I will be looking to take advantage of any healthy corrections to add to my position in Silvercrest Metals, and potentially start new positions in PAAS and WPM. Many investors are lured into buying the highest-cost silver miners as they will finally be profitable if silver breaks out. However, I think the more prudent move is to buy the lowest-cost silver miners as they will thrive in any situation, regardless of what the silver price does. In the case of PAAS, WPM, and SILV, it’s wiser to have quality than quantity, being a basket of sub-par miners, and I believe these three names are all one needs to effectively position for upside in the silver market.

(Disclosure: I am long SILV)

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “BUY THE DIP” Growth Stocks for 2020

7 “Safe-Haven” Dividend Stocks for Turbulent Times

PAAS shares were trading at $27.70 per share on Friday morning, up $0.65 (+2.40%). Year-to-date, PAAS has gained 17.44%, versus a -8.21% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| PAAS | Get Rating | Get Rating | Get Rating |

| SILV | Get Rating | Get Rating | Get Rating |

| WPM | Get Rating | Get Rating | Get Rating |