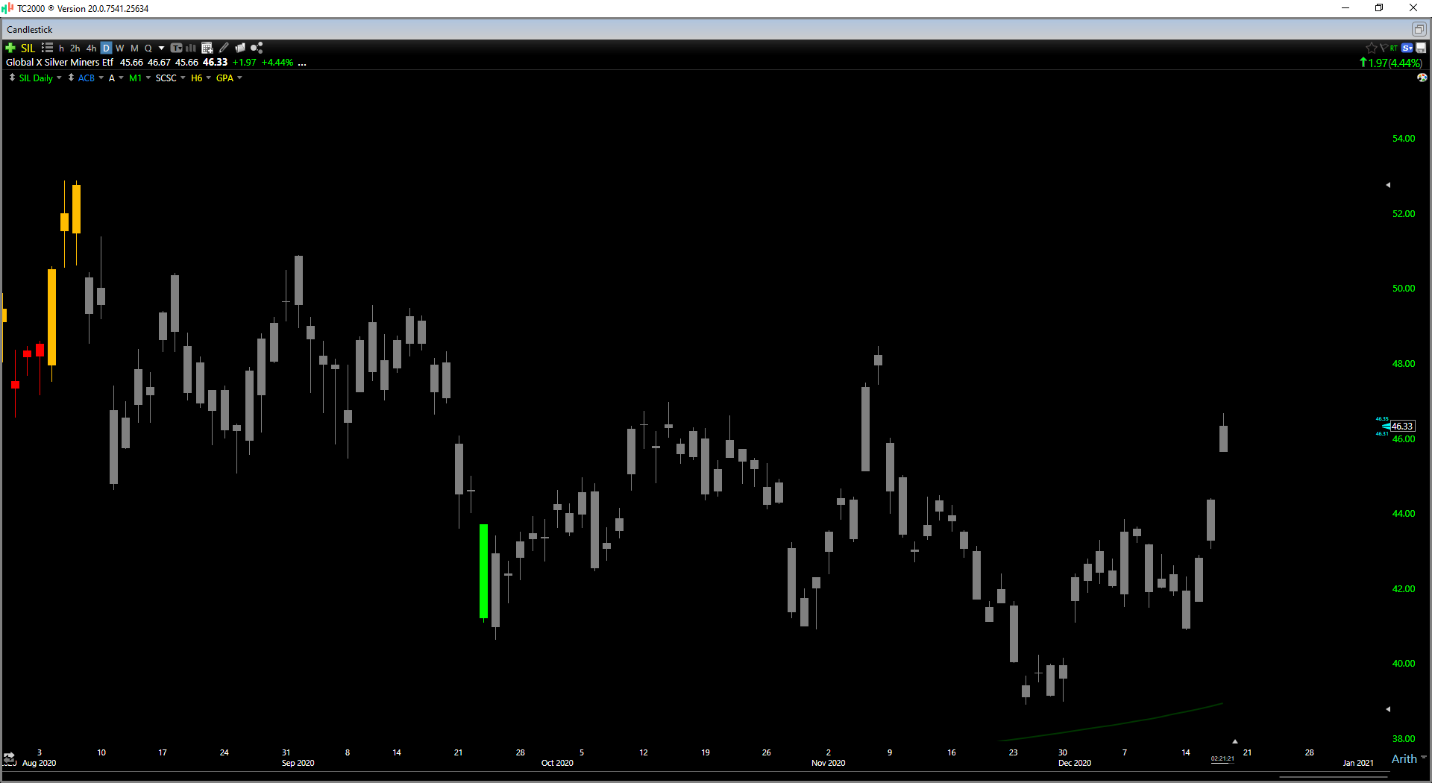

The Silver Miners Index (SIL) reversed sharply in August before beginning a more than 20% correction, but many silver miners are finally waking back up, with a few already hitting new year-to-date highs. Generally, the silver producers in the index offer much better leverage than the metal itself, as well as dividends, with roughly one-third of the sector paying a yield of 0.50% or more. While this might not seem like much, the group is likely to increase their dividends substantially over the next year if the price of silver (SLV) holds above $25.00/oz.

This is precisely what we’ve seen from the Gold Miners Index (GDX) over the past year. However, it’s imperative to select the right silver producers because one-third of the index pays no dividend and is known for serially destroying shareholder value. In this article, we’ll examine three names that are not only low-risk but also offer substantial earnings growth, even if silver heads back below $22.50/oz.

(Source: TC2000.com)

Couer Mining (CDE), Hecla Mining (HL), and Wheaton Precious Metals (WPM) don’t have a ton in common with two being producers and one being a royalty name, but they all share three key characteristics: safe operating jurisdictions, relatively low-risk industry-leading earnings growth. In Hecla’s case, the company is the only silver producer with more than 90% of its output coming from Tier-1 jurisdictions (U.S. & Canada). Meanwhile, Couer Mining also operates out of safe jurisdictions, with 70% of its metals production coming from the U.S. and Canada. Finally, while Wheaton PM might not have the safest jurisdictions like Hecla and Couer, but it has significantly lower risk as it is not actually operating the mines.

Instead, Wheaton Precious Metals finances miners to help them build their projects and then receives a royalty or stream on the mine indefinitely in the process. Therefore, while it may not benefit from jurisdictional safety, it benefits from having 80% plus margins and a lack of operating risk. This is because it has more than 15 projects it pulls revenue from each quarter, which decreases the risk of any single mine having an issue. Let’s take a look at Hecla first:

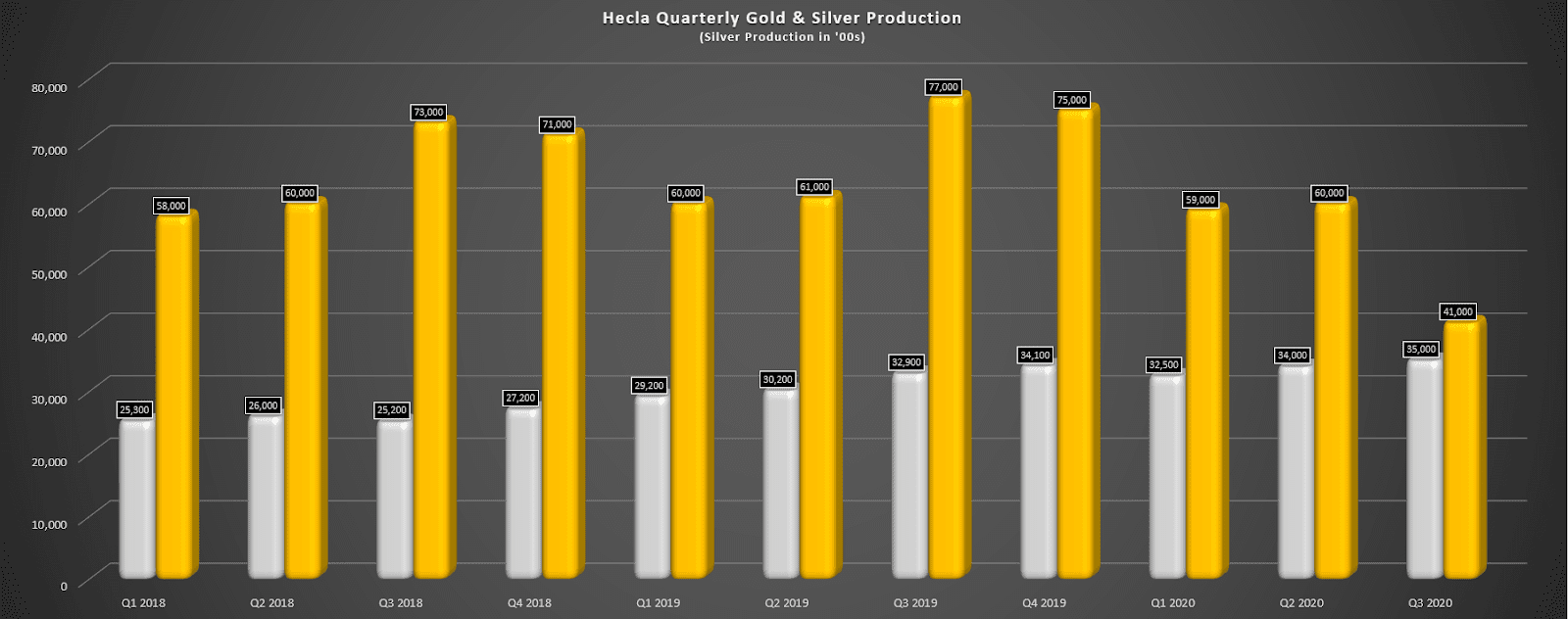

(Source: Author’s Chart)

Beginning with Hecla, the company had an exceptional quarter in Q3 with silver production of 3.5 million ounces and gold production of 41,000 ounces. While gold production was down year-over-year due to lower grades from its Casa Berardi Mine in Quebec, silver production increased by over 20% sequentially to hit a new multi-year high. This is because the company’s Lucky Friday Mine in Idaho is finally beginning to ramp-up to full capacity after a 2.5-year strike shuttered the operations temporarily.

Once in full production, Lucky Friday should be able to produce nearly 5 million ounces of silver per year, which will lead to over 30% growth in silver production for the company by FY2023. While the strike between 2017 and 2020 was certainly a pain for investors stuck in the name, it was actually a blessing in disguise, it seems. That’s because these ounces would have been sold for below $18.00/oz if the mine was in operation, but they stayed in the ground instead. Based on a 30% higher silver price than last year and a more than 7% compound annual production growth looking out to FY2024, the company is set to become a cash-flow machine.

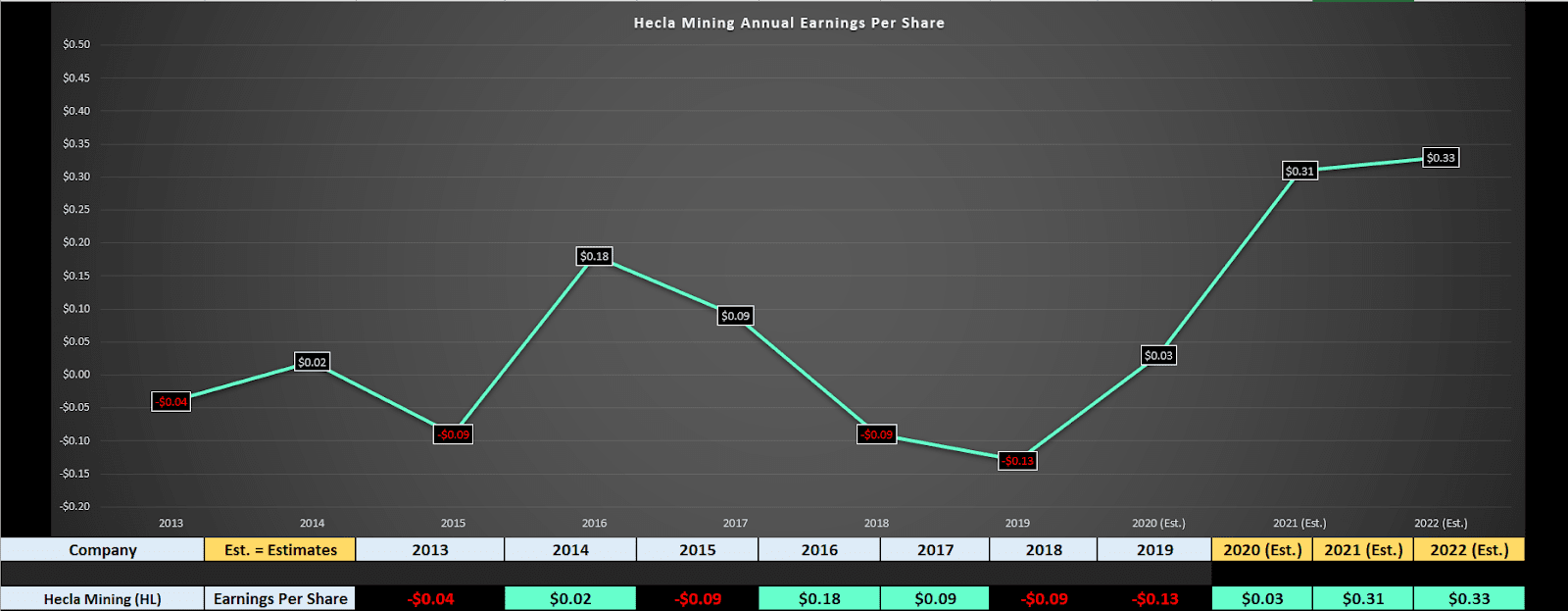

(Source: YCharts.com, Author’s Chart)

As shown in the chart above, Hecla posted net losses per share in FY2018 and FY2019 as it relied on its lower-grade mines without the benefit of bonanza grade Lucky Friday ore. However, annual EPS estimates for FY2020 are sitting at $0.03 with its first year of profitability since FY2017, and FY2021 annual EPS are currently sitting at $0.31. Assuming the company meets these estimates, which look conservative, the company will grow annual EPS by over 1000% year-over-year. This is one of the highest earnings growth rates in the whole US Market currently. Therefore, if we were to see the stock pullback below $5.00, I would expect this to be a low-risk buying opportunity.

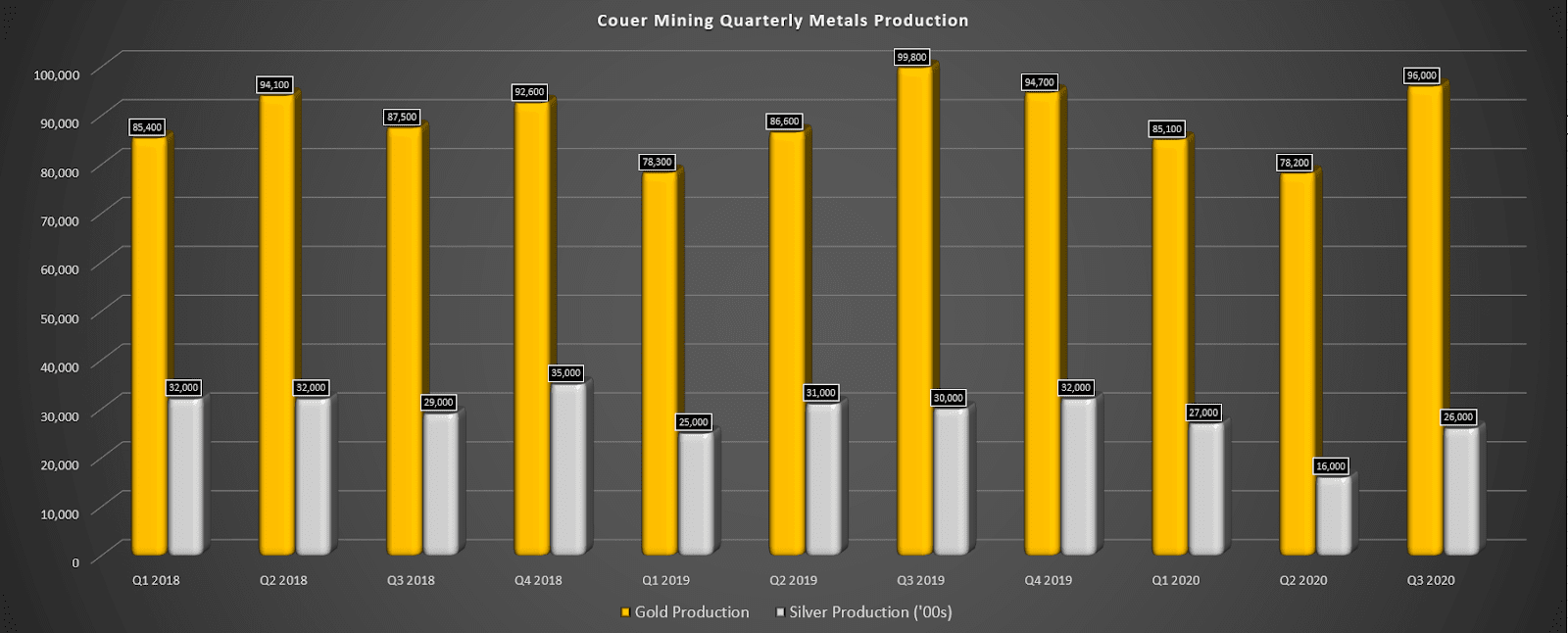

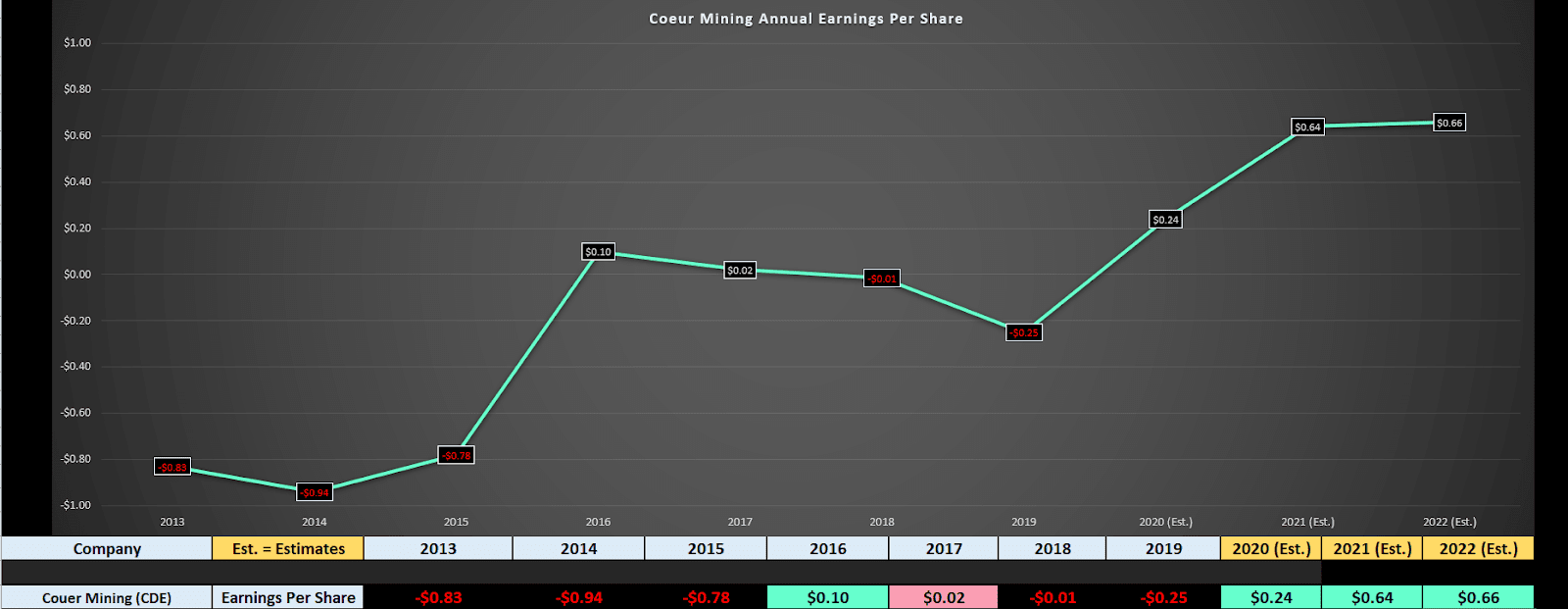

The next name on the list is Couer Mining, a silver producer that operates out of Canada and the U.S., but its flagship mine is located in Mexico. Similar to HL, Couer Mining had a solid Q3 report with quarterly gold production coming in at 96,000 ounces and silver production of 2.6 million ounces. While silver production was down year-over-year due to a weak performance from its Rochester Mine in Nevada, the Palmarejo and Wharf mines picked up the slack. This solid operating performance allowed the company to generate significant free-cash-flow, improve its leverage ratio, and the company’s cash balance is now up to over $70 million.

(Source: YCharts.com, Author’s Chart)

Couer Mining is also a turnaround story, with the company set to return to profitability this year from an earnings per share standpoint. As shown below, FY2020 annual EPS estimates are sitting at $0.24, translating to a new multi-year high.

However, the company is on track for significant growth in FY2021 as well, with estimates currently sitting at $0.64. This would translate to more than 160% growth year-over-year, and these estimates are based on a $25.00/oz silver price. Therefore, if we do see more upside in the silver price, we could see CDE generate over $0.70 in annual EPS in FY2021. The stock has gone on a massive run this week, up over 20%, but if we were to see a pullback below $8.80, I believe this would be a low-risk buying opportunity.

(Source: YCharts.com, Author’s Chart)

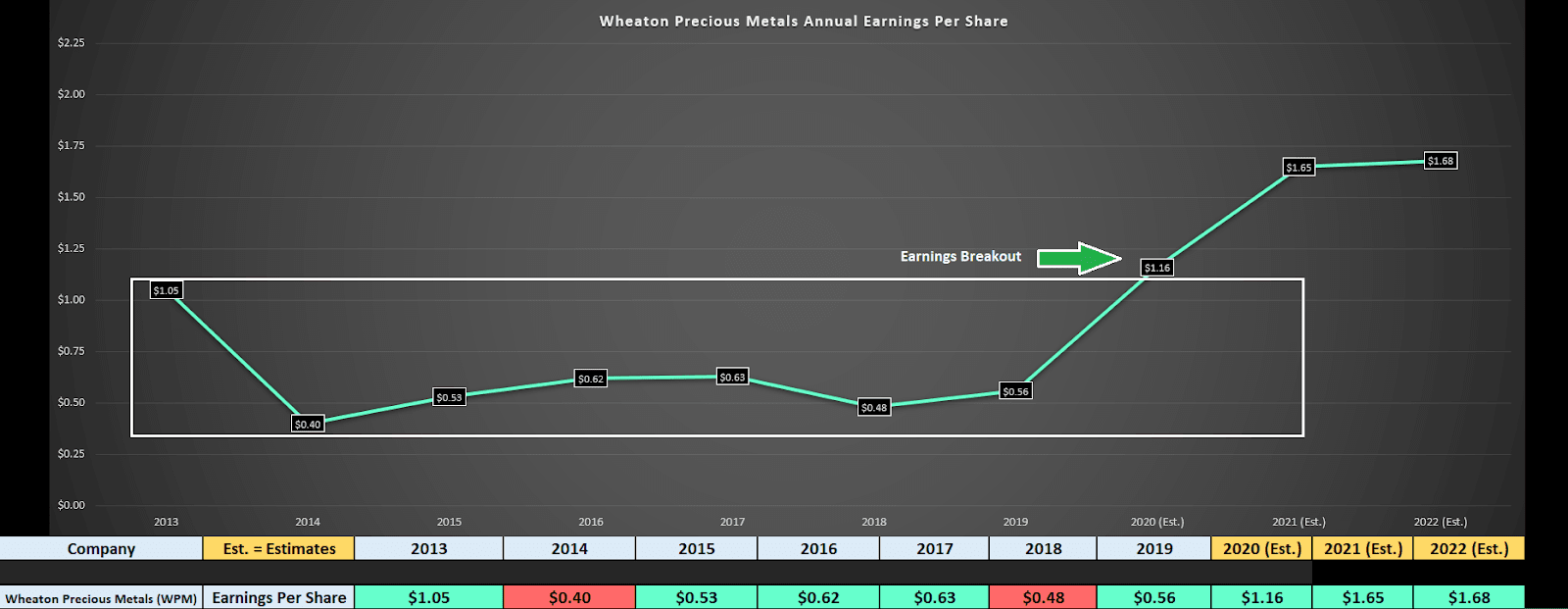

Finally, Wheaton PM has been in a terrible slump the past few months after the stock got ahead of itself in August. Fortunately, this correction has pushed the stock down to a much more reasonable valuation, with Wheaton PM now trading at just 27x FY2021 annual EPS estimates ($1.65).

While this might seem high, it’s important to note that WPM has 80% plus margins due to its royalty & streaming model and is set to grow annual EPS by over 40% next year. Besides, this strong double-digit growth rate is lapping a triple-digit growth rate that’s projected in FY2020 ($1.16 vs. $0.56). It’s rare that the stock ever pulls back below its 200-day moving average in bull markets, so this correction looks like a buying opportunity.

(Source: YCharts.com, Author’s Chart)

While there are tons of silver miners to choose from, the silver space is much riskier than the gold space as 70% of silver producers hail from unfavorable jurisdictions. This is because most of the silver mined globally comes from China, Mexico, and South America, with none of these jurisdictions being favorable relative to the United States and Canada.

Therefore, while these silver producers might not offer the most upside, they are relatively safe in a sector where so much can go wrong given the risky nature of mining. In summary, if we see HL drop below $5.00, CDE drop below $8.80, or WPM drop below $43.00, I believe these would be low-risk buying opportunities.

Disclosure: I am long WPM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

WPM shares were unchanged in after-hours trading Thursday. Year-to-date, WPM has gained 46.34%, versus a 17.31% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| WPM | Get Rating | Get Rating | Get Rating |

| SIL | Get Rating | Get Rating | Get Rating |

| Get Rating | Get Rating | Get Rating | |

| HL | Get Rating | Get Rating | Get Rating |

| SLV | Get Rating | Get Rating | Get Rating |

| CDE | Get Rating | Get Rating | Get Rating |