Further evidence that a recession isn’t coming soon (most likely late 2020 or early 2021 at the earliest), comes from the bond market, which has been the most accurate recession predictor yet discovered. The bond market is driven by large institutional money flows, from things like asset managers, pension funds, insurance companies, and sovereign wealth funds. These are the people whose job it is to keep a pulse on the US and global economy and protect billions of people’s money during such downturns.

The way the bond market warns us about recessions is via the yield curve, which is the difference between short and long-term bond yields. When short-term yields exceed long-term ones, the curve is said to be inverted. According to a study by the San Francisco Federal Reserve an inverted yield curve has “correctly signaled all nine recessions since 1955 and had only one false positive, in the mid-1960s, when an inversion was followed by an economic slowdown but not an official recession.”

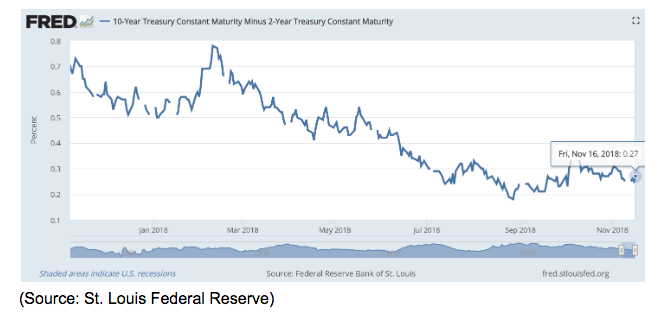

Specifically, when the 2-year and 10-year yield curve inverts, 90% of the time within six to 24 months a recession begins (average lead time 17 months). The 2/10 yield curve has indeed been falling (flattening) for years now. BUT in the last few weeks, despite falling long-term yields (flight to safety) the curve has actually remained stable.

In fact, the 2/10 yield curve (there are actually dozens of yield curves), bottomed on August 18th at 0.18% and has since recovered to 0.27%. More importantly, in recent weeks, it’s actually been stable, despite 10-year yields falling. Why is that so significant? Because while it’s normal for long-term rates to fall when stocks decline (flight to safety), it’s NOT normal for the 2-year yield to decline. Not when it’s been rising rapidly for over a year on expectations that the Fed would continue hiking (five or six more times per the latest dot plot).

About the Author:

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Top 4 Tech Companies Poised for Explosive Returns

Amid rising digitalization efforts among businesses and continued innovation, the technology industry is witnessing steady growth and expansion. Given the industry tailwinds, investors could consider buying top tech stocks HP (HPQ), Teledyne Technologies (TDY), TD SYNNEX (SNX), and Dropbox (DBX) for solid returns. Read on…

3 Gold Stocks to Buy Delivering Exciting Returns

The gold market is poised for solid long-term growth thanks to surging gold demand for jewelry, backed by its appeal as an investment amid geopolitical concerns and potential interest rate cuts. Thus, investors could consider buying quality gold stocks DRDGOLD (DRD), Harmony Gold Mining (HMY), and Centamin (CELTF) for exciting returns. Continue reading…GOOGL Earnings Breakdown and Optimizing Your Portfolio Strategy

With Alphabet's (GOOGL) earnings drawing near, investors eagerly await the potential earnings from its key services like Google Search, YouTube ad revenue, and Google Cloud. Join us as we delve into GOOGL's performance, offering insights to fine-tune your portfolio strategy...

Best & Worst Performing Stock Industries for April 24, 2024

Led by ticker KGJI, "Fashion & Luxury" was our best performing stock industry of the day, with a 1,301.22% gain.