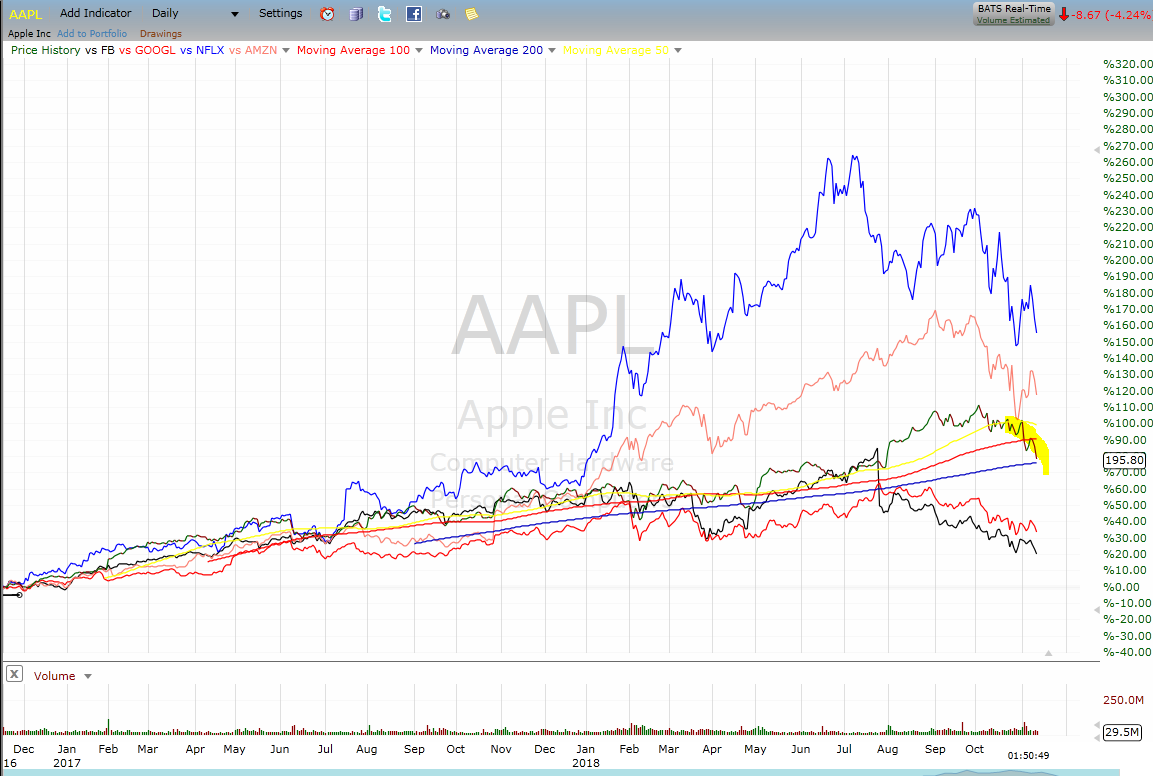

Apple (AAPL) is catching up to rest of FANG (Facebook, Amazon, Netflix, Google) but not in a good way. After today’s drop, it’s down about 10% from its highs. Is this a buying opportunity? Or a sign the whole market is turning rotten?

Apple is not only the largest component of the tech-heavy Nasdaq 100, in which it accounts for over 12% but also one of the largest influences on the price-weighted Dow Jones Industrial Average S&P 500.

Apple’s importance is not mathematical but also psychological for a wide swath of investor sentiment. It’s owned in both growth and value funds, dividend and buyback funds, tech sector funds and consumer-driven strategies. Needless to say, it’ll be the stock to watch as November grinds on.

After initially holding up better than its FANG brethren during a brutal October, Apple is now also in full correction mode.

(Source:freestockcharts.com)

The sell-off started following the 11/1/18 earnings report in which the company not only delivered small misses on the top and bottom line but also lowered guidance.

And then it announced it would no longer provide metrics on units sold of the iPhone, tablets, and laptops. Apple claimed the decision was made to give more focus on the overall ecosystem and growing importance its services.

But investors took the decrease in transparency as a worrisome sign. Indeed in the past week, we have seen key component suppliers such as Skyworks Solutions (SWKS) and Lumentun (LITE) issue disappointing reports and these stocks each sold off over 15%. And now that selling has spilled over is Apple which was down more than 5% at one point on Monday.

From a technical standpoint, $195 level could be a great spot to get long(buy), as it brings you back to the level it was trading at prior to the Q2 earnings report, that propelled AAPL above $200 for its largest one day gain ever.

(Source:stockcharts.com)

From a fundamental standpoint, many consider Apple cheap. Not just an absolute basis versus the overall market but especially compared to the rest of the FANG gang.

It trades at just 14x forward p/e and has over $120 billion in cash, which allows it to keep paying a dividend whose yield is now 2.5% and keep $500 million per quarter share repurchase program in place.

I think given the above technical and fundamental set up this could be a good time to take a bullish bite into shares of Apple.

About the Author: Steve Smith

Steve has more than 30 years of investment experience with an expertise in options trading. He’s written for TheStreet.com, Minyanville and currently for Option Sensei. Learn more about Steve’s background, along with links to his most recent articles. More...

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Best & Worst Performing Mega Cap Stocks for July 11, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 34.37%.

Best & Worst Performing Mega Cap Stocks for July 10, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 9, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 8, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.