It’s been a volatile year for the Nasdaq-100 (QQQ), with the index trading in a more than 22% range from its March low to its recent high. Fortunately, the volatility has been to the upside more recently, with the QQQ up 13% in the past 30 days alone. For investors already in the market, this has provided an opportunity to book some profits into strength. However, it’s left many names trading at lofty valuations for those anxious to put money to work, with some tech names trading at sub 2% free cash flow yields and as high as 50x sales. While most growth names are pricey, some names look interesting, with one being a growth story at a more reasonable price and another being a mega-cap that is worth keeping on one’s shopping list if it re-tests its recent breakout. Let’s take a look at a couple of names below:

(Source: TC2000.com)

Lightspeed POS Inc (LSPD) and Amazon (AMZN) have little in common, with LSPD having a market cap of $10BB and in the early stages of its growth story and AMZN sporting a $1.8TT market cap and being much more mature. However, both do share one trait, impressive revenue growth and projected earnings growth, with AMZN set to double annual earnings per share between FY2020 and FY2023. Meanwhile, Lightspeed is set to be earnings positive in FY2023 ($0.04), with the potential for quadruple-digit annual EPS growth in FY2024 ($0.46). Notably, both companies are disruptors with LSPD powering the future of commerce, intending to be a commerce platform for the entire value chain with its recent acquisition of NuOrder and Ecwid.

Beginning with Lightspeed, the company just came off a massive quarter in fiscal Q4 2021 with revenue of $82.4MM, translating to 127% growth year-over-year. This is the strongest quarter of growth for the company since it went public in Q3 of last year, with its previous best quarter coming in at 78% growth. On a sequential basis, this 127% growth rate translated to a 4900 basis point acceleration from the most recent quarter (fiscal Q3 2021), with a much higher gross transaction value ($33.7BB in FY2021 vs. $22.3BB) driven by a sharp increase in total customer locations. As of the end of FY2021, Lightspeed had ~119,000 total locations, with this figure increasing to ~140,000 with the recent acquisition of Vend. Notably, average revenue per user also increased materially, and subscription/transaction-based revenue represented 91% of all revenue in the most recent quarter.

(Source: YCharts.com, Author’s Chart)

While FY2021 was a massive year, and some might assume it will be difficult to replicate these results, estimates would suggest differently. As shown above, LSPD is set to report revenue of more than $460MM in FY2022, translating to more than 100% sales growth after lapping 82% growth last year. This would be a material acceleration on a year-over-year basis and reduce the company’s revenue multiple from 44x to closer to barely 22x. If we look ahead to FY2023, revenue is expected to increase by 45%, leaving LSPD at barely 15x FY2023 sales estimates. Generally, I would not be interested in any stock trading above 40x sales, but when the company is projected to enjoy triple-digit growth in the current fiscal year, the revenue multiple is less relevant. Given this growth story, a revenue multiple of 22 is not unreasonable, and this would translate to a market cap of more than $15.2BB based on estimates of ~$690MM in revenue in FY2023.

(Source: TC2000.com)

If we look at LSPD’s technical picture, we can see that the stock looks to be building a cup base, and a shakeout in this handle could present a low-risk buying opportunity. This would translate to a dip towards the $70.00 level, which would shake out any investors hoping for a shallow handle as we see currently. A pullback of this magnitude would also reel in the stock’s market cap a little, leaving LSPD trading at closer to 20x FY2022 revenue estimates of ~$460MM. Of course, there’s no guarantee that the stock pulls back this sharply, but if we do see a drop below $69.50, I would view this as a low-risk buying opportunity.

The second name worth keeping a close eye on is Amazon, which also came off a massive quarter with sales up 44% year-over-year to $108.5BB. This matched the company’s previous two-year high revenue growth rate of 44% in the previous quarter. In addition to high double-digit sales growth, operating margins have continued to strengthen, coming in at 10.0% vs. 5.3% in the year-ago period. This contributed to a nearly 10% increase in free cash flow despite significant investments and a 69% jump in operating cash flow. The strong performance was driven by an acceleration in Amazon Web Services revenue growth, with the consumer business robust as well, especially internationally.

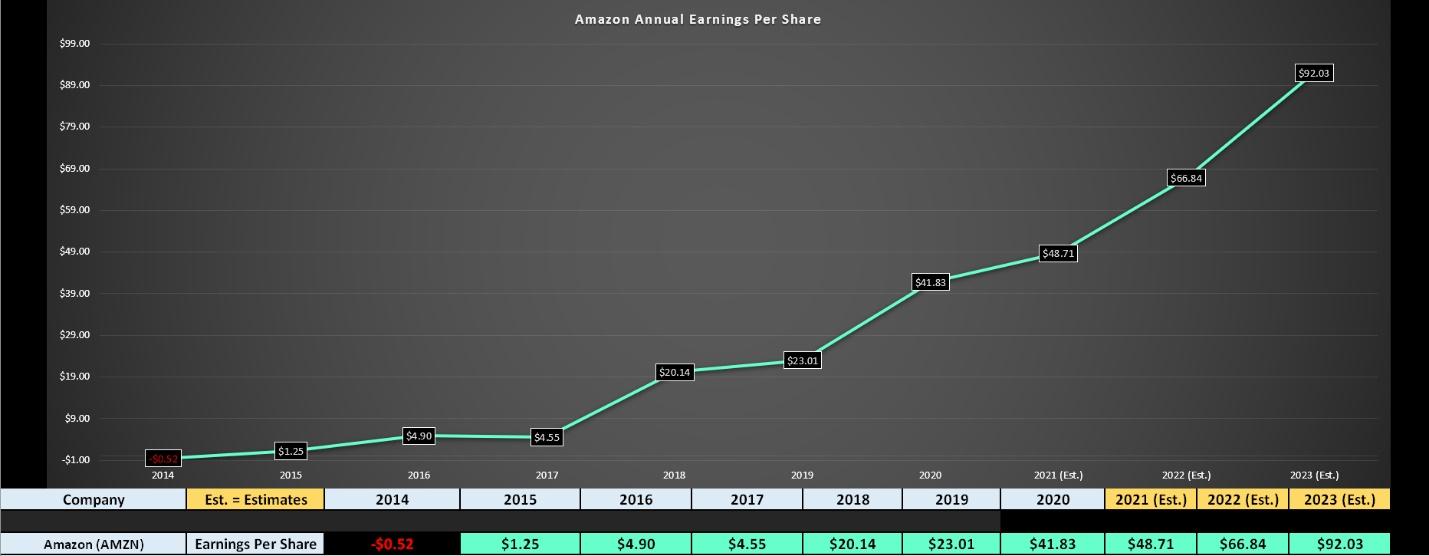

When it comes to recent investments that will pave the way for future growth, Twitch is up to 35MM daily visitors, and Prime Video streaming hours were up 70% year-over-year, with Amazon Studios having a solid award season. The addition of more titles on Prime Video and the addition of Prime Music has improved the value proposition for Prime members, increasing the potential for retention down the road in this steadily growing segment. Given the exceptional Q1 results, annual EPS estimates for FY2021 have increased to $48.71, with some estimates as high as $60.00.

This would translate to more than 16% growth at the lower end of estimates (FY2020: $41.83) and ~44% growth at the high end of current forecasts. If we look ahead to FY2022, estimates have increased as well, and the lower range estimates of $66.84 are looking conservative. Even if AMZN only meets these figures, this would translate to another year of high double-digit earnings growth, paving the way for up to $100.00 in annual EPS in FY2023. So, while some investors might argue that AMZN looks expensive at more than 65x trailing EPS, the stock looks very reasonably valued if we factor in the potential for $100.00 in annual EPS in FY2023, leaving AMZN at barely 35x earnings for a mega-cap with a robust growth rate.

(Source: YCharts.com, Author’s Chart)

If we look at AMZN’s technical picture, the stock seems to be leading annual EPS to new highs, with AMZN continuing its strong uptrend from its massive base breakout last year and recently breaking out of a multi-month base near $3,350. With AMZN more than 10% above this breakout, the stock is no longer at a low-risk buy point, but if the stock re-tested this breakout level, this would represent a low-risk spot to add to one’s position. In addition, a dip to $3,350 would leave the stock trading at an even more attractive valuation. So, while I don’t plan to add to the stock here, I may look to add to my position bought at $1,900 if we do see a multi-week pullback and some weakness in the general market. As shown below, AMZN has room to a share price of $5,000 in the next 2 years if it were to test its upper channel line.

(Source: TC2000.com)

With the Nasdaq Composite up nearly 15% year-to-date, I don’t see this as the time to be rushing to add new long exposure. However, AMZN and LSPD look like solid buy-the-dip candidates if we do see some general market weakness, given their exceptional growth rates and market-leading positions. Therefore, I see them as two names to keep near the top of one’s shopping list if some turbulence arrives. For now, I remain long AMZN and may look to start a position in LSPD at $69.50 or lower.

Disclosure: I am long AMZN

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

AMZN shares were trading at $3,630.93 per share on Thursday afternoon, down $50.75 (-1.38%). Year-to-date, AMZN has gained 11.48%, versus a 16.63% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| AMZN | Get Rating | Get Rating | Get Rating |

| Get Rating | Get Rating | Get Rating | |

| QQQ | Get Rating | Get Rating | Get Rating |