It’s been a volatile year thus far for the Nasdaq 100 Index (QQQ), which was briefly staring down a more than 20% loss as of last week. However, the index has recovered sharply over the past several days, clawing back nearly half of its losses and now making a run towards its declining 200-day moving average. While much of the bull camp is convinced that we are headed higher, the recent bottom did not have many of the ingredients we typically see at major bottoms, suggesting a possibility that we could see a re-test of the lows near $325.00.

(Source: TC2000.com)

Given the risk of a re-test or pullback towards the $325.00 level on QQQ, it’s more difficult to justify aggressively adding exposure here. However, it is worth building a shopping list in case the market does retrace some of its recent gains. There are currently several names with compelling stories, and in this update, we’ll look at one beaten-up name that’s finally looking cheap and one with explosive earnings growth. Let’s take a closer look below:

Pure Storage (PSTG) and DocuSign (DOCU) have little in common from a technical standpoint, with one name recently making new multi-year lows and the other racing towards new all-time highs. However, both companies boast strong sales growth and steady earnings growth from a fundamental standpoint, and are leaders in their industry. In DOCU’s case, the company doesn’t expect to see much earnings growth in 2023 but will see nearly 50% earnings growth over the next two years. In PSTG’s case, the company just came off a year of 290% earnings growth and expects to follow this up with double-digit growth in FY2023. Let’s look at DocuSign first.

While DocuSign was one of the clear pandemic winners and posted a more than 200% return in 2020, the stock has come under significant pressure since, with sales decelerating meaningfully from FY2020 levels and on a sequential basis. This was evidenced by 35% sales growth in the most recent quarter, one of the weakest sales growth rates in the past two years. Given that the stock was priced for near perfection heading into its Q3 report, it’s no surprise that the stock fell more than 40% following the deceleration. The most recent quarter confirmed this trend in deceleration (35% vs. 42%).

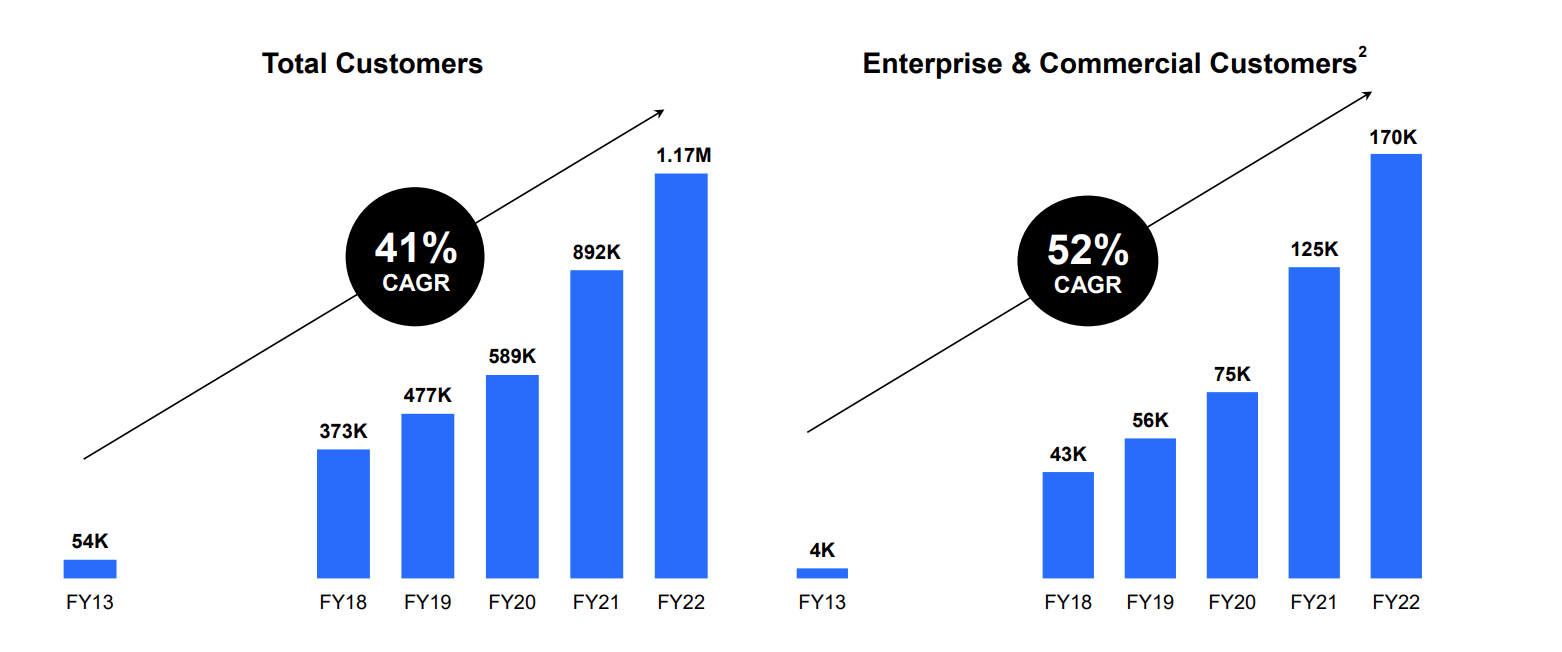

(Source: Company Presentation)

Having said that, this sell-off looks to be caused more by the fact that the stock was priced too richly heading into this period of deceleration vs. a fatal flaw in the business model. In fact, as shown above, DOCU continues to put up impressive growth in its customer count, with total customers coming in at 1.17MM in FY2022, up 25% year-over-year. The company saw even more impressive growth in its enterprise/commercial customer count, which soared 40% year-over-year despite lapping nearly 70% growth in FY2021.

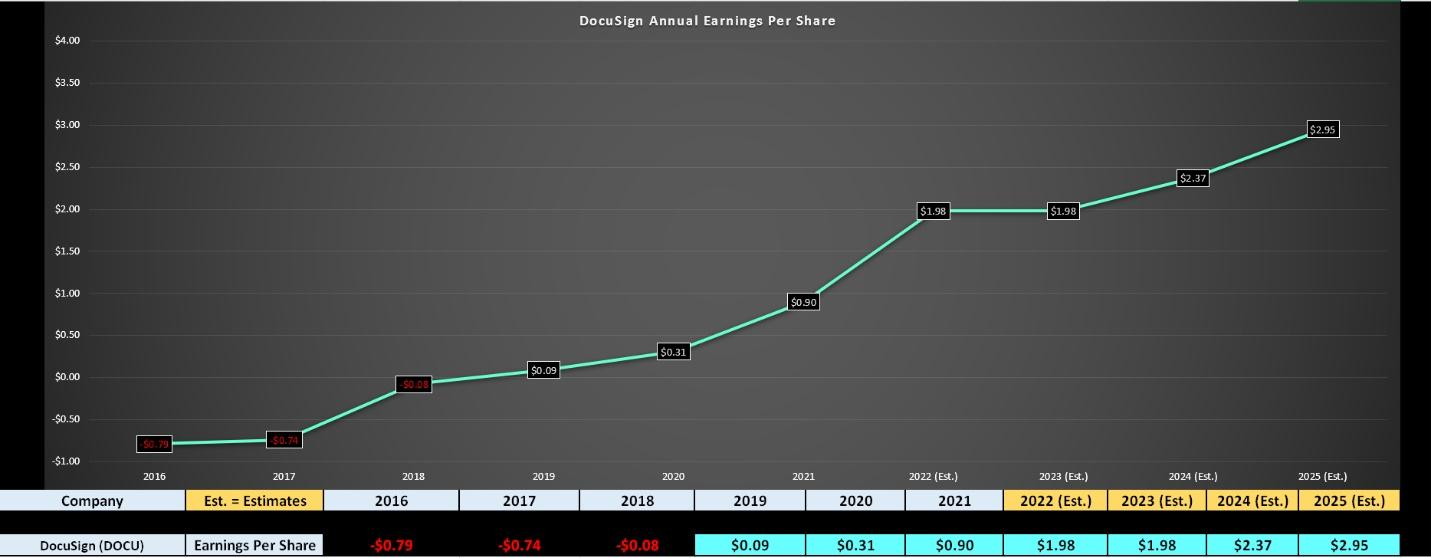

With the world continuing to move towards digital and DocuSign’s Electronic Signature product becoming a more household name, I would expect this growth to continue at a steady pace, which suggests that the stock is still in the middle earnings of its growth story. However, with relatively tepid FY2023 revenue guidance of $2.48BB, the stock has struggled to gain much traction. The good news is that while FY2023 should be a softer year for the stock, there is growth on the horizon in FY2024 and FY2025. In addition, with the stock falling out of favor, the valuation has become much more reasonable if the company can meet these current estimates.

If we look at the earnings trend below, we can see that DOCU is forecasted to earn $2.37 in FY2024 and $2.95 in FY2025, translating to 49% growth from FY2022 levels. While this pales compared to some of the higher-growth large-cap tech names, this is still very respectable growth. Based on a current share price of $101.00, it leaves DOCU trading at 42 FY2024 earnings estimates. I would argue that a fair earnings multiple for the stock is 50x earnings, which translates to a fair value for DOCU of $118.50.

(Source: FactSet.com, Author’s Chart)

While this points to upside, I prefer to buy at a minimum 35% discount to fair value to bake in a margin of safety, especially when it comes to sector laggards that are out of favor. In DOCU’s case, this means that the stock would need to dip below $77.00 to become more attractive from a fundamental standpoint. Notably, a pullback to this level would place the stock within 15% of a major support level for the stock, which represents its breakout level at $65.00 – $67.00.

(Source: TC2000.com)

If the market continues to climb, DOCU may not re-visit this support area. However, with the recent rally occurring in a V-fashion, I would not be surprised to see DOCU retrace closer to its recent lows at $71.00 per share. Assuming a pullback within 5% of this level ($75.00), DOCU would trade at just ~31x earnings and would be quite attractive from a swing-trading standpoint. So, while I have no interest in buying DOCU, I think the stock is worth keeping a close eye on for a re-test or near re-test of its recent lows at $75.00 per share or lower.

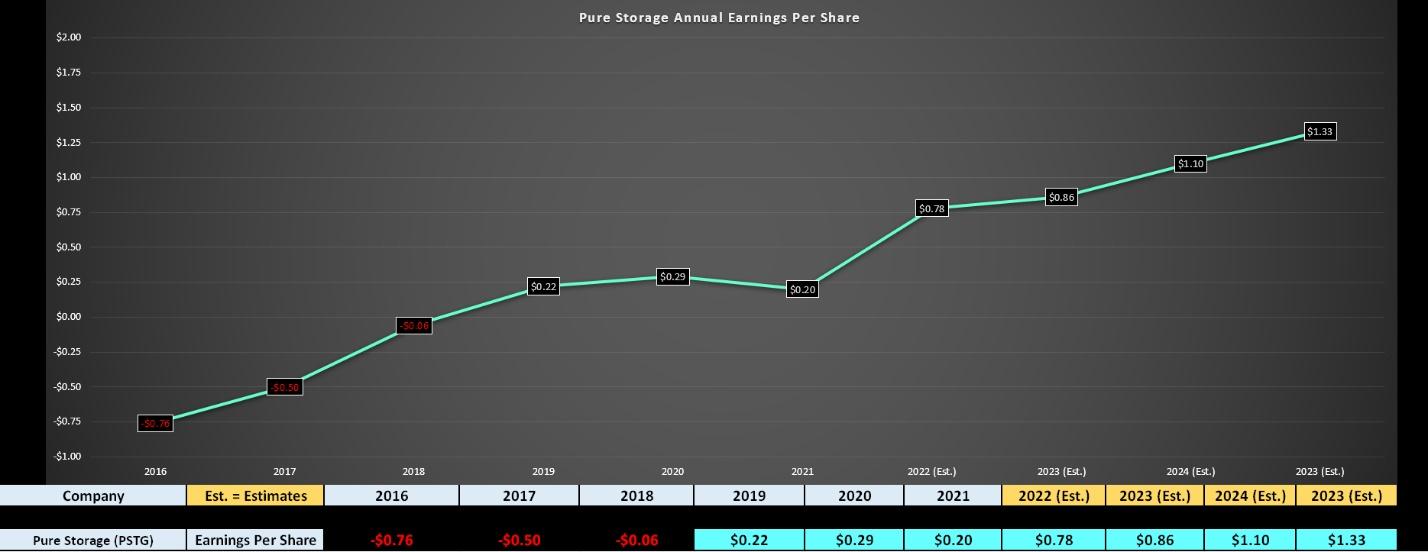

Moving over to Pure Storage, the company had a blowout year in FY2022 and a solid Q4 report. The company reported revenue of $709MM, up 41% year-over-year, which marked a third consecutive quarter of acceleration from 12%, 23%, and 37%, respectively, in Q1, Q2, and Q3 2022. These strong results combined with meaningful margin expansion (940 basis point increase) helped the company to report 177% growth in quarterly EPS and 290% growth in annual EPS ($0.78 vs. $0.20).

This growth was driven by strong demand for the company’s products and solutions, with the Storage-as-a-Service model clearly gaining traction. In fact, the company now calls 52% of Fortune 500 companies customers and added more than 470 new customers in Q4 2022 alone. Long-term, the company has estimated its total addressable market at $60BB, meaning that if it meets FY2023 sales guidance of $2.5BB, it’s still knocking on the door of just ~4% of its total TAM, suggesting long-term upside for this mid-cap data storage company.

(Source: TC2000.com)

Looking ahead to FY2023, FY2024, and FY2025 earnings estimates, we can see that annual EPS is expected to increase 10% next year and more than 65% over the next three years. This is exceptional growth for a company that just lapped 290% growth year-over-year and has difficult comps ahead. Based on a current share price of $34.50, this leaves PSTG trading at just 31x FY2024 earnings estimates, a reasonable valuation for a company with this growth profile.

(Source: TC2000.com)

Finally, there’s a lot to like here from a technical standpoint, with PSTG breaking out of a massive base at the same time as the market is struggling to get back above its 200-day moving average. This relative strength is quite encouraging, and it suggests that PSTG could be a new market leader. Having said that, the stock is a little bit extended short-term above its strong support level of $27.50 – $28.00. So, while I think this is a solid buy-the-dip candidate, I believe the ideal buy point is at $29.50 or lower. At these levels, the stock would trade at less than 27x FY2024 earnings estimates and offer a larger margin of safety.

With the Nasdaq 100 up more than 10% off its lows, I do not see this as the time to be rushing in to add new exposure. However, DOCU and PSTG are trading at reasonable valuations, and if we do see market weakness, both will drop into buy zones at $75.00 and $29.50, respectively. This is why I am not invested in either stock at current levels. Still, I believe these names should be at the top of one’s shopping list if they retrace a portion of their recent gains and relieve their overbought conditions.

Disclosure: I have no positions in any stocks mentioned

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one’s portfolio.

Want More Great Investing Ideas?

DOCU shares were trading at $104.55 per share on Thursday afternoon, up $4.38 (+4.37%). Year-to-date, DOCU has declined -31.36%, versus a -4.86% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| DOCU | Get Rating | Get Rating | Get Rating |

| PSTG | Get Rating | Get Rating | Get Rating |

| QQQ | Get Rating | Get Rating | Get Rating |