It’s been a wild start to 2020 thus far with the Nasdaq Composite (QQQ) adding another 5% to its already impressive 2019 gains, and the S&P-500 (SPY) starting the year off with a 4% return. While several technology stocks are beginning to get overbought after running up for months following breakouts, two names were busy building bases throughout 2019, and have now finally broken out. Therefore, if the market does see a correction as we head into February, these are two buy candidates that should be on one’s watchlist for potential purchases.

(Source: TC2000.com)

At first glance, one would argue that there’s very little in common with Salesforce.com (CRM) and Facebook (FB), but Salesforce.com and Facebook do have one big thing in common, fresh multi-year breakouts and powerful annual EPS growth. Both Facebook and Salesforce.com emerged from massive breakouts in late 2019, and are both expecting to see strong earnings growth in FY-2020. Based on growing earnings and two powerful looking long-term charts, I believe both names are worth considering if the market does see a 5% or larger correction into February. Let’s take a closer look below:

(Source: YCharts.com, Author’s Chart)

Beginning with Salesforce.com’s earnings trend, we can see that annual earnings per share have grown massively since FY-2013, up over 500% from $0.41 to $2.56 in FY-2019. If we look out to FY-2020 estimates, annual EPS is expected to grow 13% year-over-year, after lapping a massive year in FY-2019 with over 60% growth. This is incredible growth from a mega-cap company, with FY-2021 annual EPS also expected to hit new highs. While the stock may look expensive at a forward P/E ratio above 60 currently, there are few mega-caps out there with this type of sustainable growth and solid double-digit growth rates. Therefore, I believe that any 10% dips in Salesforce.com would provide an opportunity to start a long position, moving the valuation closer to a P/E ratio of 50.

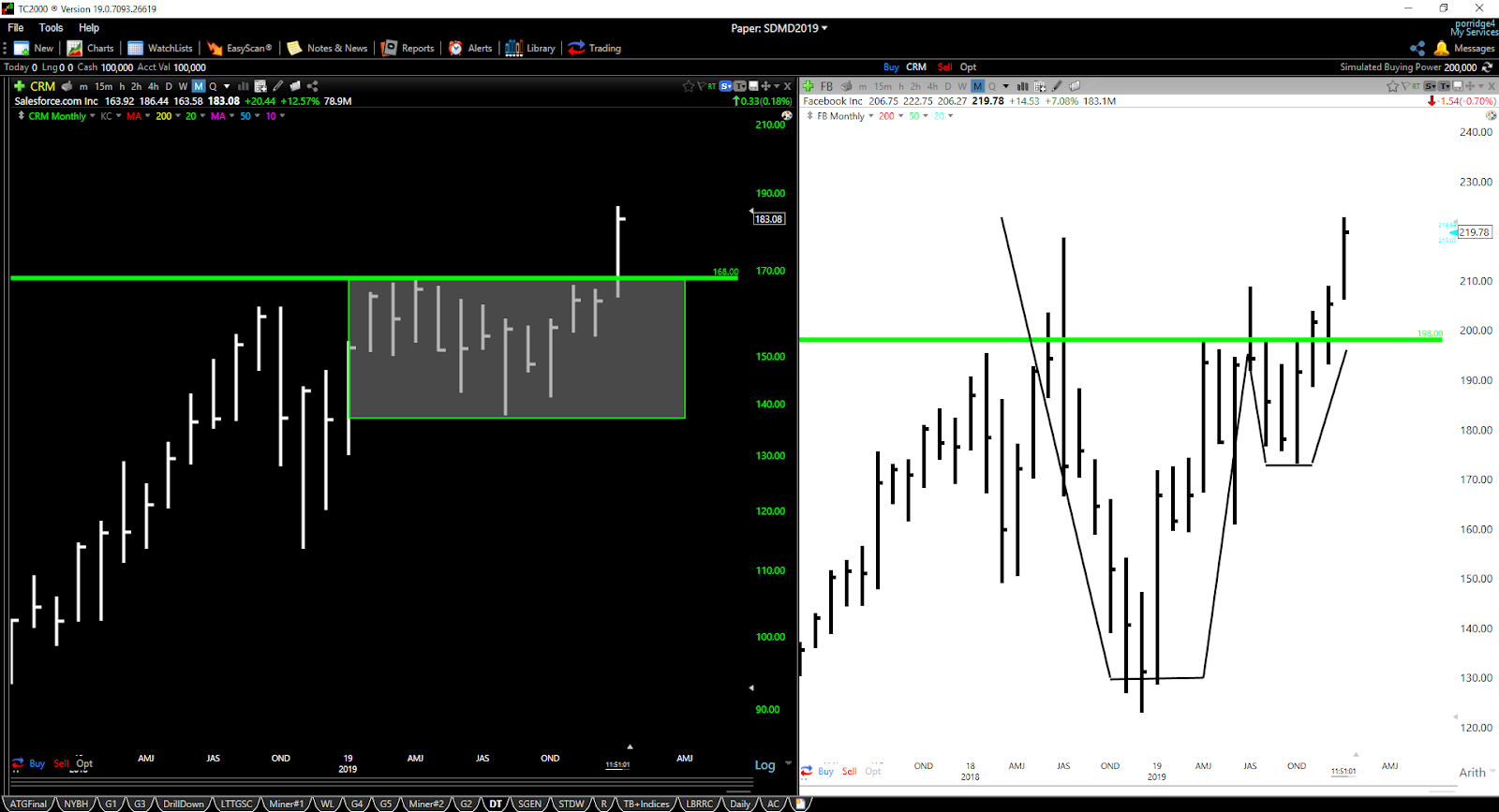

(Source: TC2000.com)

If we look at the chart above, we can see that Salesforce.com just broke out of a massive multi-year base, and this technical breakout is being confirmed by annual earnings per share continuing to make new highs. Based on this, I believe that any pullbacks towards the top of this base near $168.00 would provide buying opportunities. The popular adage is “the bigger the base, the higher the space,” and Salesforce.com certainly has a long runway for outperformance as long as this breakout holds. Therefore, as long as the Salesforce.com bulls can defend the $168.00 level on any pullbacks, I would view long positions in the $165.00 – $168.00 area as low-risk spots to take a position.

(Source: YCharts.com)

Moving over to Facebook, the company is heading into an election year, which should boost top and bottom-line growth substantially, and analysts are indeed forecasting this based on estimates. As we can see in the chart above, Facebook’s annual EPS growth slowed materially to estimates for only high single-digit growth in FY-2019. However, FY-2020 is expected to accelerate back to mid-double-digit levels, and resume the prior trend of robust annual EPS. Based on the current FY-2020 annual EPS estimates for Facebook of $9.20, analysts are forecasting roughly 12.5% growth, a nearly 500 basis point acceleration from the 8% growth projected in FY-2019. If we look out to FY-2021 estimates, this earnings growth is anticipated to accelerate even further, with forecasts of $11.10. Therefore, Facebook should put up solid double-digit growth for both FY-2020 and FY-2021, with earnings accelerating sequentially in both years.

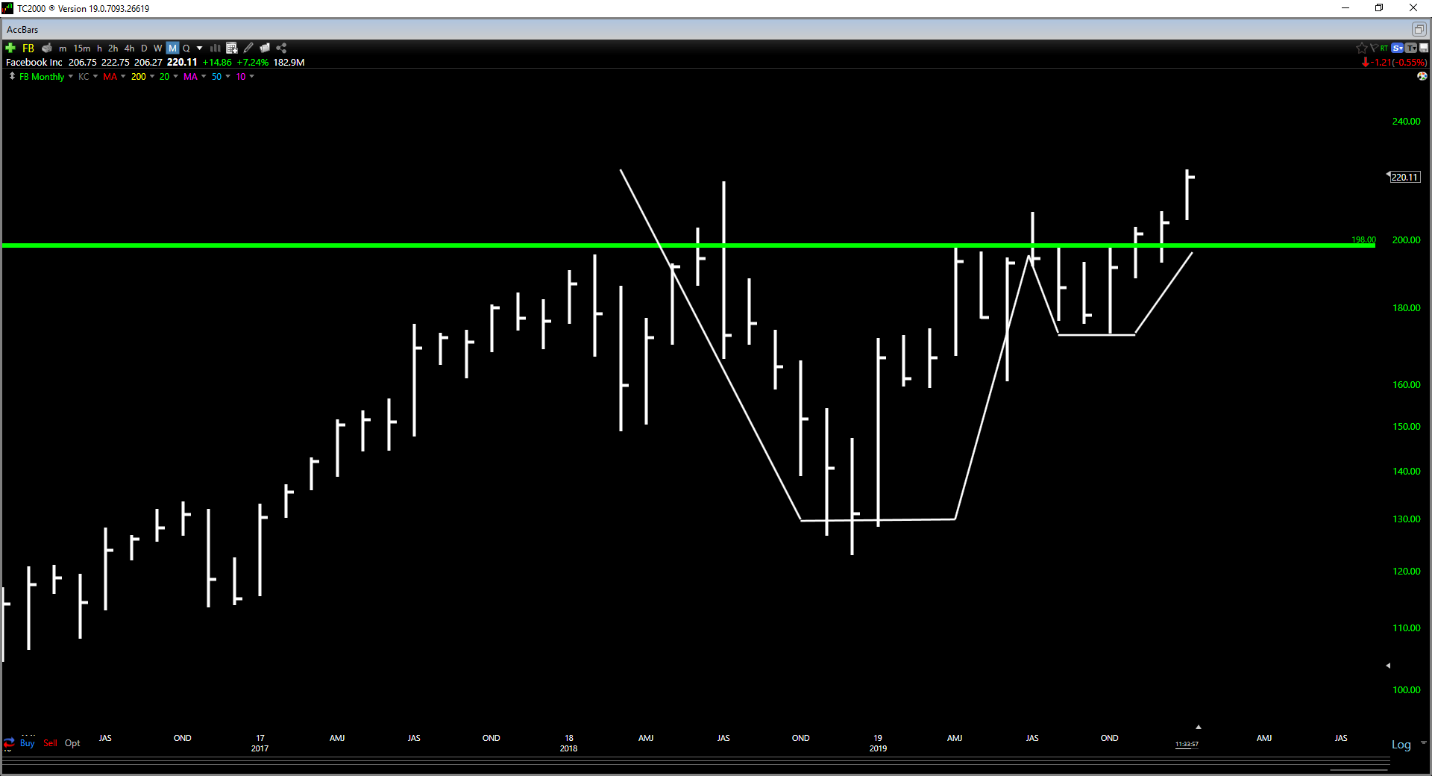

(Source: TC2000.com)

Similar to Salesforce.com, Facebook is sporting a massive monthly breakout, with this breakout occurring near the $198.00 level. If the stock could pull back over the next month or two towards this level, I believe this would provide an excellent opportunity for investors to start a position at less than 23x FY-2020 earnings estimates. This is a more than reasonable valuation for a leading tech name with accelerating earnings growth, and I would not be surprised to see Facebook hit $250.00 at some point this year.

While I would not be chasing Facebook or Salesforce.com here with the market over-extended, I do believe that both companies would provide exceptional buying opportunities if we see some weakness over the coming month or two. The ideal spot for Facebook would be a pullback to the $195.00 – $200.00 zone, with the ideal spot for Salesforce.com being a pullback to the $165.00 – $168.00 zone. Generally, prior resistance levels become new support levels, and I’d expect the bulls to play strong defense here. In summary, for investors looking for ideas in tech that aren’t at exorbitant valuations, Facebook and Salesforce.com are two ideas with further upside potential in 2020.

FB shares . Year-to-date, FB has gained 7.07%, versus a 3.06% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| FB | Get Rating | Get Rating | Get Rating |

| CRM | Get Rating | Get Rating | Get Rating |