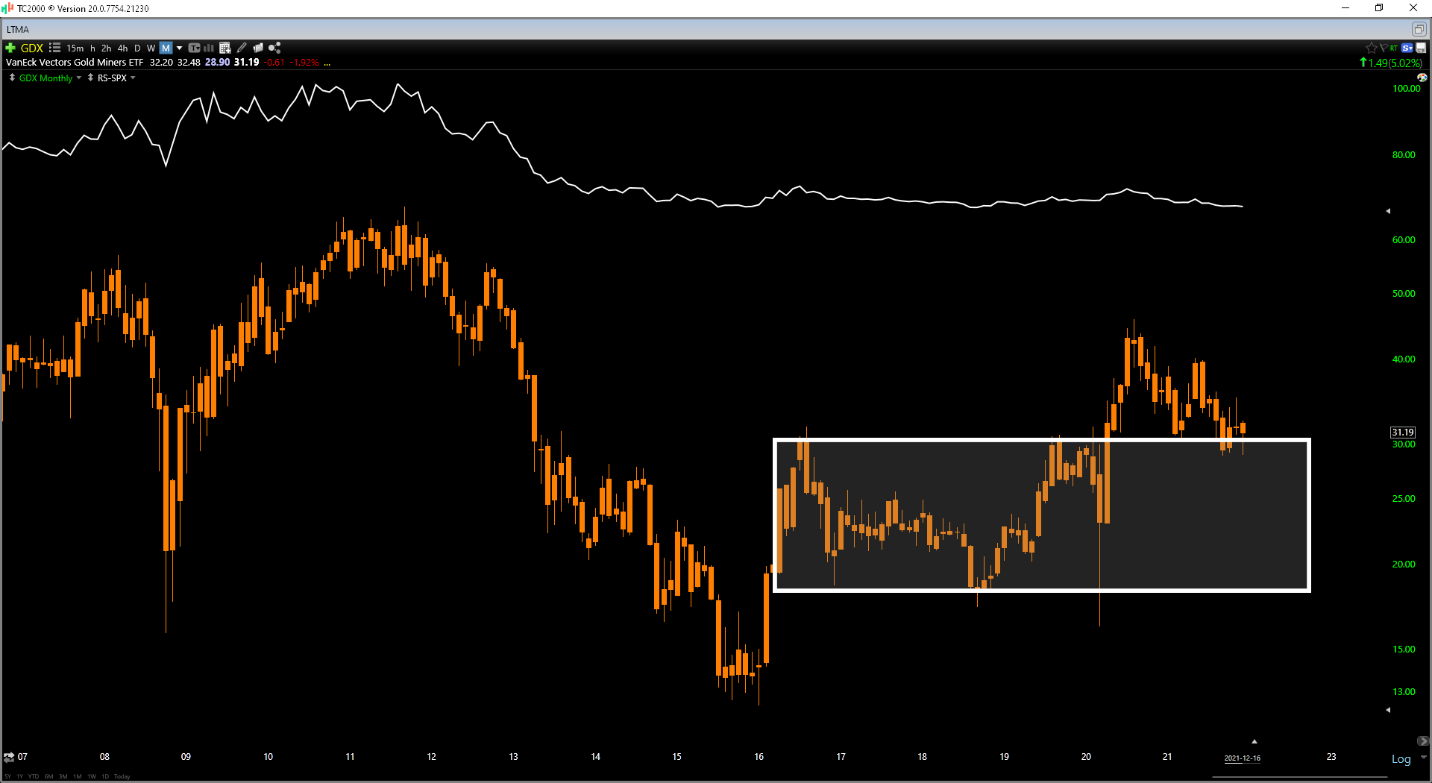

It’s been a tough year for investors in the Gold Miners Index (GDX), with the ETF down more than 10% year-to-date and massively underperforming the S&P-500 (SPY). However, while the performance has been disappointing, it has contributed to the worst sentiment readings we’ve seen in years for gold miners, and it has left their valuations at their most attractive levels in several years. Meanwhile, though the GDX remains in an intermediate downtrend and a deep correction, we’ve seen no real damage to the long-term technical picture. This is because the GDX is simply back-testing a multi-year breakout, and so far, finding support in this key area. Let’s take a look below:

(Source: TC2000.com)

As shown in the chart above, while the miners’ performance has been depressing, the setup for the GDX remains very constructive. This points to a higher probability of dips being bought near the $30.00 level in the future and suggests that investors should be looking at starting positions in some of the highest-quality names. Three names that stand out as very reasonably valued with solid management teams are Agnico Eagle Mines (AEM), B2Gold (BTG), and Skeena Resources (SKE). While all three have very different business models, they all own world-class mines, have industry-leading margins or projected industry-leading margins, and management teams that continue to under-promise and over-deliver.

Beginning with B2Gold, the company had a very strong quarter, reporting record quarterly production of ~295,700 ounces or ~310,300 ounces when including contribution from its interest in Calibre Mining. This was helped by record production from Fekola and Otjikoto and led to a nearly 20% increase in gold production year-over-year. Given the strong performance, B2Gold raised its FY2021 guidance to ~1.04 million ounces of gold and continues to have some of the lowest costs sector-wide, with all-in sustaining costs coming in at $777/oz, translating to nearly 60% margins at the current gold price.

Unfortunately, the one negative for B2Gold is that it lacks immediate growth. This is because it does not currently have any major projects under construction, and its most advanced non-producing asset, Gramalote, is still at least three years away from production. The low-growth outlook from a previous high-growth profile has led to a significant compression in B2Gold’s earnings and NAV multiple, with the stock correcting more than 40% from its highs.

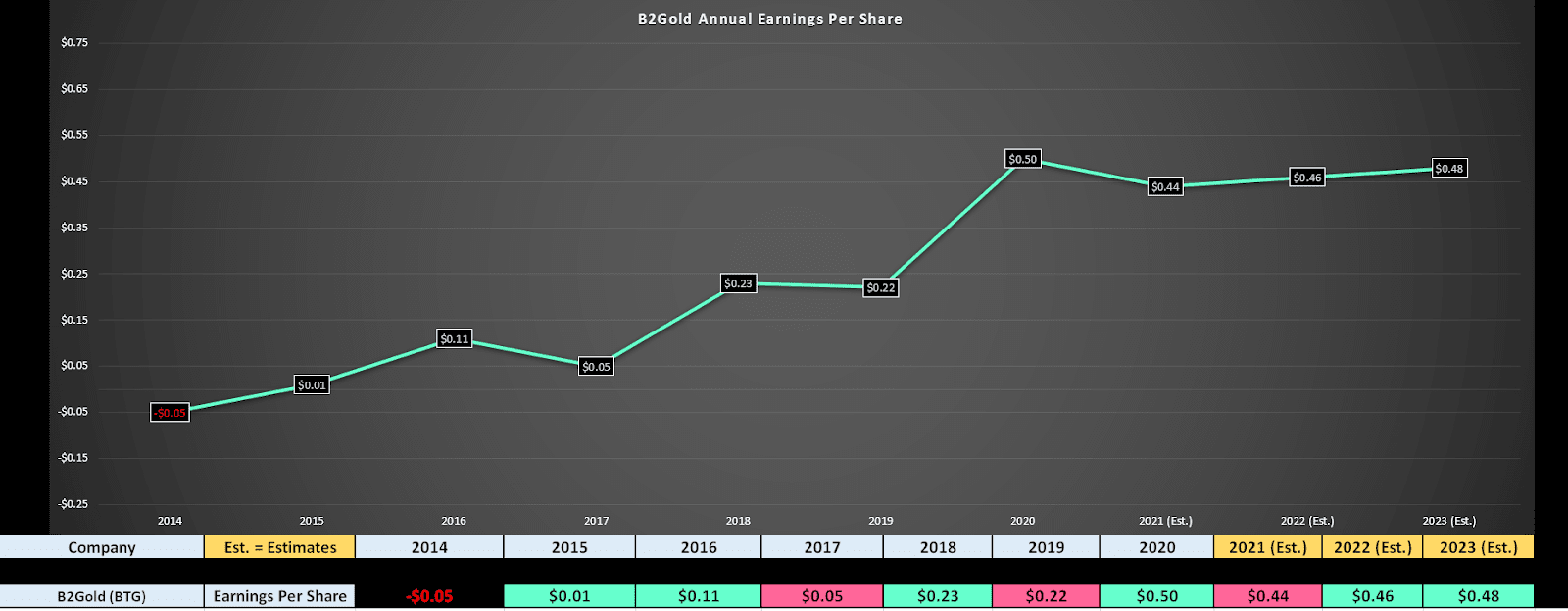

(Source: YCharts.com, Author’s Chart)

However, while annual EPS did peak in FY2020 and will remain below the peak until at least FY2023 (unless B2Gold sees help from the gold price) the stock has now priced in much of this negativity. This is because the stock currently trades at just 8.25x earnings at a share price of $3.80, and this is despite having nearly $0.65 in net cash. This is a dirt-cheap valuation for a million-ounce gold producer with 50% plus margins. Finally, if we look at the technical picture, the stock is back-testing its prior breakout, showing that both the fundamental and technical picture is nearing a buy zone. In summary, I would view any pullbacks below $3.65 as low-risk buying opportunities.

(Source: TC2000.com)

The next name on the list is Agnico Eagle Mines, one of the largest gold producers globally if it successfully completes its merger with Kirkland Lake Gold. Unlike B2Gold, Agnico Eagle Mines has more than 90% of its gold production coming from Tier-1 ranked jurisdictions, with mines in Finland, Canada, and Australia. This makes the stock much lower risk than its peers, with the major differentiator being AEM’s massive growth pipeline. As it stands, AEM has multiple development projects in the wings that could add nearly 800,000 ounces of annual production, and the company owns some of the highest-grade gold mines globally, giving it one of the highest margin profiles among its peers.

Following the merger of Kirkland Lake Gold and Agnico Eagle, the combined company will be a nearly 3.4-million-ounce gold producer with costs below $925/oz, with a platform to grow production to more than 4.5 million ounces per year over the next 5-6 years. This is a rarity in the gold space, given that most of the multi-million-ounce producers have no growth and have costs above $1,000/oz. So, from an investment standpoint, Agnico Eagle checks every single box, having industry-leading grades, industry-leading margins, industry-leading growth, and an exceptional ESG rating, with some of the lowest greenhouse gas emissions per ounce of gold produced. Therefore, for investors interested in the sector, AEM is a must-own name.

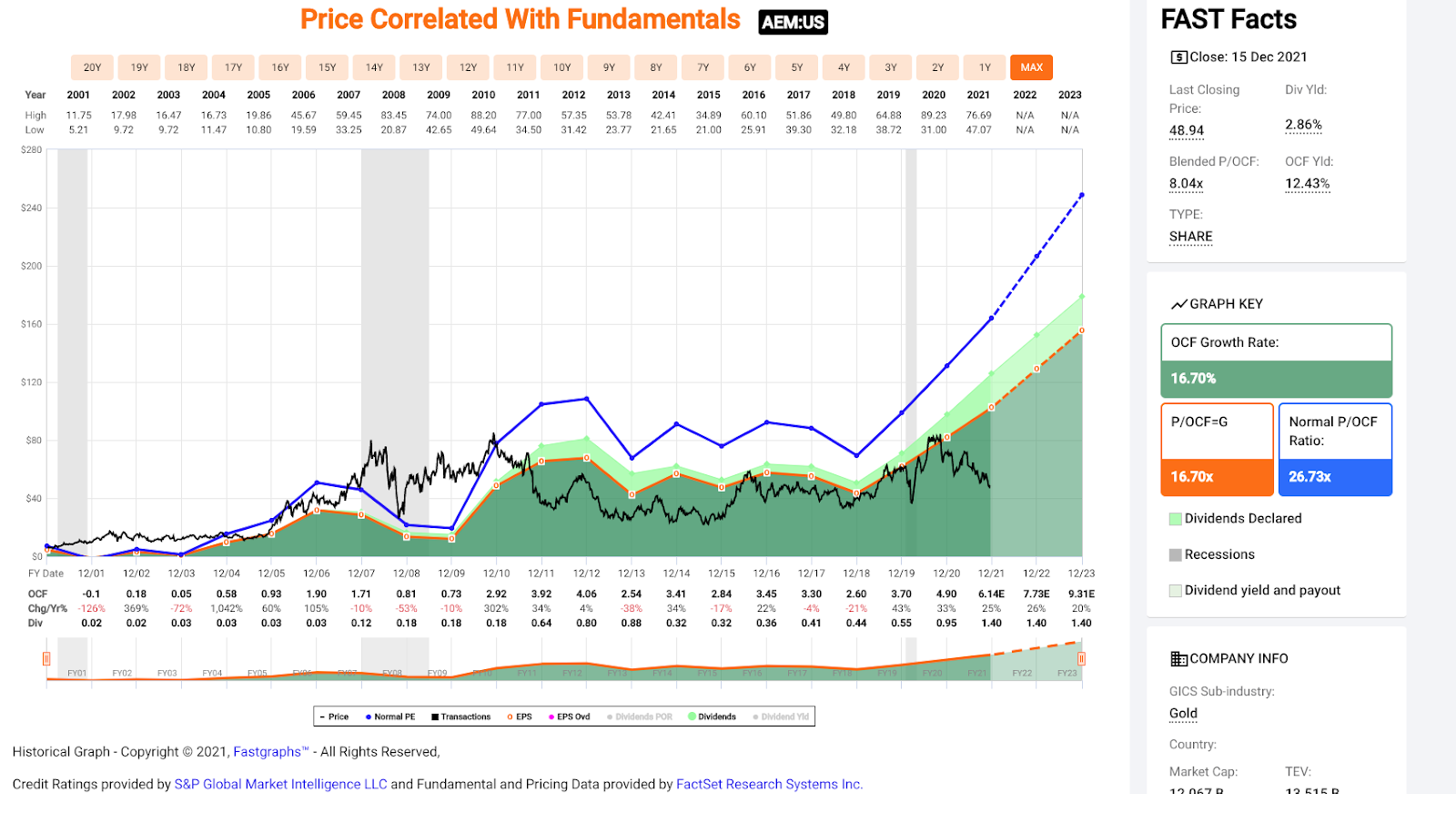

(Source: FASTGraphs.com)

Despite this improved outlook, AEM is currently trading at less than 8x operating cash flow. This is before a merger that should reduce this multiple to less than 7x operating cash flow, given KL’s significant cash flow generation. If we look at the chart above, the stock has historically traded at nearly double this cash flow multiple, pointing to a fair value for the stock closer to $90.00 if it were to re-rate to its historical multiple. Meanwhile, the stock looks to be building a handle in a 15-year base, with this correction nearly complete from a technical standpoint. Given AEM’s strong forward outlook, nearly 3.0% dividend yield, and a nearly double-digit free cash flow yield, I see the stock as a steal at current levels.

(Source: TC2000.com)

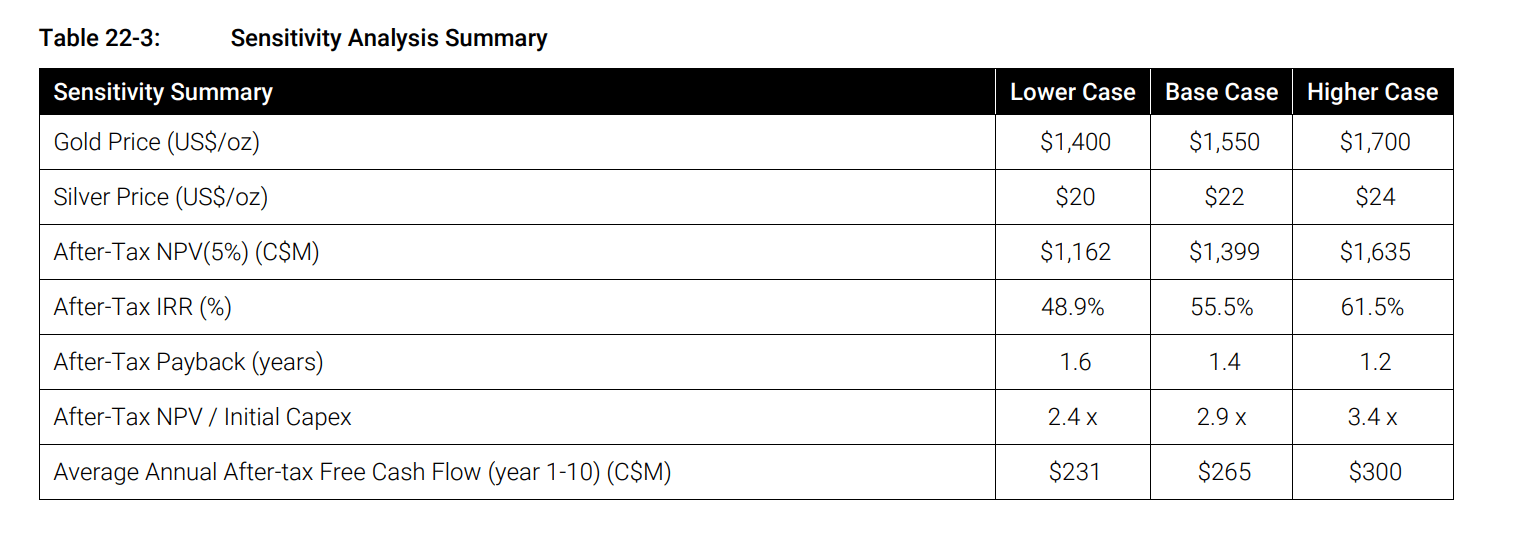

The final name worth keeping an eye on is Skeena Resources (SKE), a development-stage company that’s busy advancing its Eskay Creek Project in British Columbia, Canada. While there are several developers with solid projects in Canada, Eskay Creek is head and shoulders above the majority, given that it has the potential to produce up to 400,000 gold-equivalent ounces per annum at costs below $700/oz once in production. This makes it one of the largest undeveloped gold projects sector-wide, with costs set to come in 30% below the sector average.

Given this rare combination of scale and high margins, I continue to see Skeena as a top takeover target sector, with a high likelihood that a large producer will come along and snap the company up for a meaningful premium. However, despite Skeena having an incredible project in a safe jurisdiction, the company trades at ~0.50x NPV (5%), with a market cap of ~$760MM and an estimated After-Tax NPV (5%) of $1.55BB when including exploration upside. Recently, we saw another developer acquired for more than 0.80x NPV (5%), and if we were to see a similar bid for Skeena, this would translate to a buyout price north of $15.00 per share.

(Source: Company Presentation)

Obviously, there’s no guarantee that Skeena will be acquired, and I would never buy a stock only because it’s a takeover target. However, if Skeena ends up heading into production in 2025, the fair value would be even higher, with a Tier-1 producer with sub $700/oz costs easily commanding an NPV (5%) multiple of 1.10. This would translate to a fair value closer to $20.00 per share as it approaches production. So, in either scenario, I see meaningful upside for the stock, but a takeover would certainly lead to a faster re-rating.

(Source: TC2000.com)

Looking at Skeena’s technical picture below, the stock appears to be trading in a broadening pattern, with support at C$11.00 [US$8.80] and resistance at C$19.00 [US$15.20]. With the stock finding strong support at the bottom of its broadening formation, there is meaningful upside if this uptrend continues. So, with Skeena checking all three boxes as being a takeover target, being in a clear uptrend with momentum at its back, and being in a safe jurisdiction, I see the stock as one of the best ways to play the junior gold sector. Therefore, I would view pullbacks below US$9.20 as low-risk buying opportunities.

After more than a year of bloodshed in the Gold Miners Index, it’s no surprise that many investors have given up, and some don’t even want to hear about gold stocks. However, it’s when the majority are throwing in the towel that the best opportunities arise, and I struggle to recall a better reward/risk scenario for owning gold producers and top-ranked gold developers in the past six years. In fact, the last time was at the end of the bear market in Q4 2015. So, I see AEM, SKE, and BTG as three top ideas to buy on dips for investors looking for exposure to the space.

I am long GLD, SKE, AEM, BTG

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

GLD shares were trading at $168.54 per share on Friday morning, up $0.38 (+0.23%). Year-to-date, GLD has declined -5.51%, versus a 25.07% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| GLD | Get Rating | Get Rating | Get Rating |

| GDX | Get Rating | Get Rating | Get Rating |

| AEM | Get Rating | Get Rating | Get Rating |

| BTG | Get Rating | Get Rating | Get Rating |

| SKE | Get Rating | Get Rating | Get Rating |