It’s been a rough couple of months for the Gold Miners Index (GDX), with the ETF giving up most of its Q2 gains and sliding back towards support near the $31.00 – $32.00 level. While this has been quite disappointing for fully committed investors that were hoping for a meaningful move higher, it’s a blessing for investors that have been sitting on an ample amount of cash, waiting for a chance to buy back their favorite names in the space. Currently, many names are trading at very reasonable valuations, but a select few are sitting at dirt-cheap valuations, with more than 40% upside to their conservative fair value. In this update, we’ll look at a few that look like compelling buys currently.

Some investors view the GDX as the preferred trading vehicle for gaining leverage to the gold (GLD) price, but given that there are several poorly run companies in the ETF, the performance of the worst names can drag significantly on the GDX’s returns. This is why I believe the best way to get leverage to the gold price is by investing in some of the best-run companies trading at the deepest discounts to fair value. An investment in individual miners allows investors to get complete exposure to names with the most favorable reward/risk ratios without picking up unnecessary exposure to names that consistently under-deliver. Kirkland Lake Gold (KL), Pretium Resources (PVG), and Integra Resources (ITRG) are three of the most intriguing ideas in the large-cap, mid-cap, and micro-cap space as of this week. All of them should perform quite well even if the gold price remains in a range between $1,725/oz and $1,925/oz over the next 12 months, given that a large margin of safety is baked in at current levels.

(Source: Company Filings, Author’s Chart)

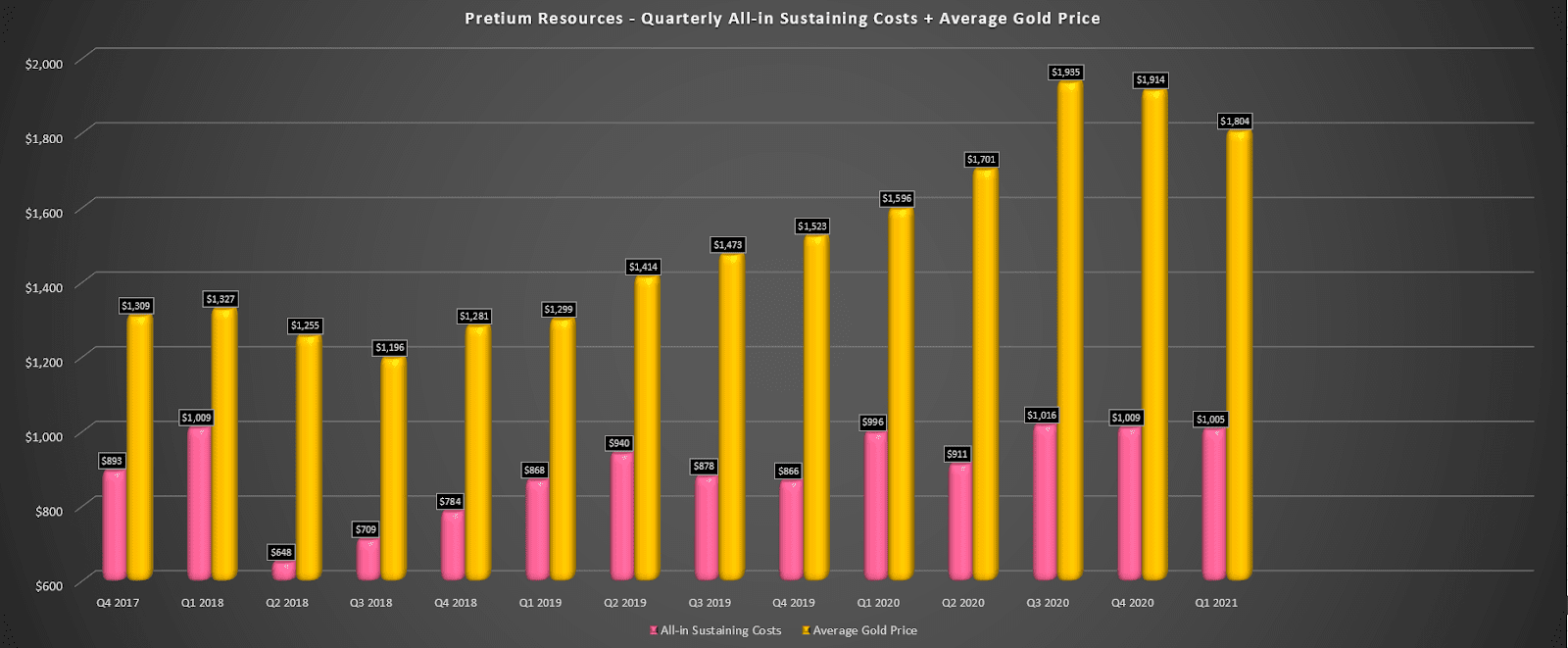

Beginning with Pretium Resources, the company has been punished severely thus far this year, with PVG down 22% year-to-date. This poor performance can be attributed to a higher-cost and higher-capex year in 2021, combined with currency headwinds from a stronger Canadian Dollar. During Q1, the company produced ~85,000 ounces of gold at costs of $1,005/oz, with throughput rates slightly below budget due to a COVID-19 breakout in February. The issue has since been resolved, and COVID-19 vaccinations have increased considerably in the workforce. However, this led to lower production than planned in Q2 and a soft Q2 ahead due to weaker grades than expected in three stopes. Having said that, while costs are expected to increase year-over-year, PVG still has impressive margins, with a high likelihood of $725/oz in AISC margins based on FY2021 costs of $1,075/oz and an average realized gold price of $1,800/oz.

(Source: YCharts.com, Author’s Chart)

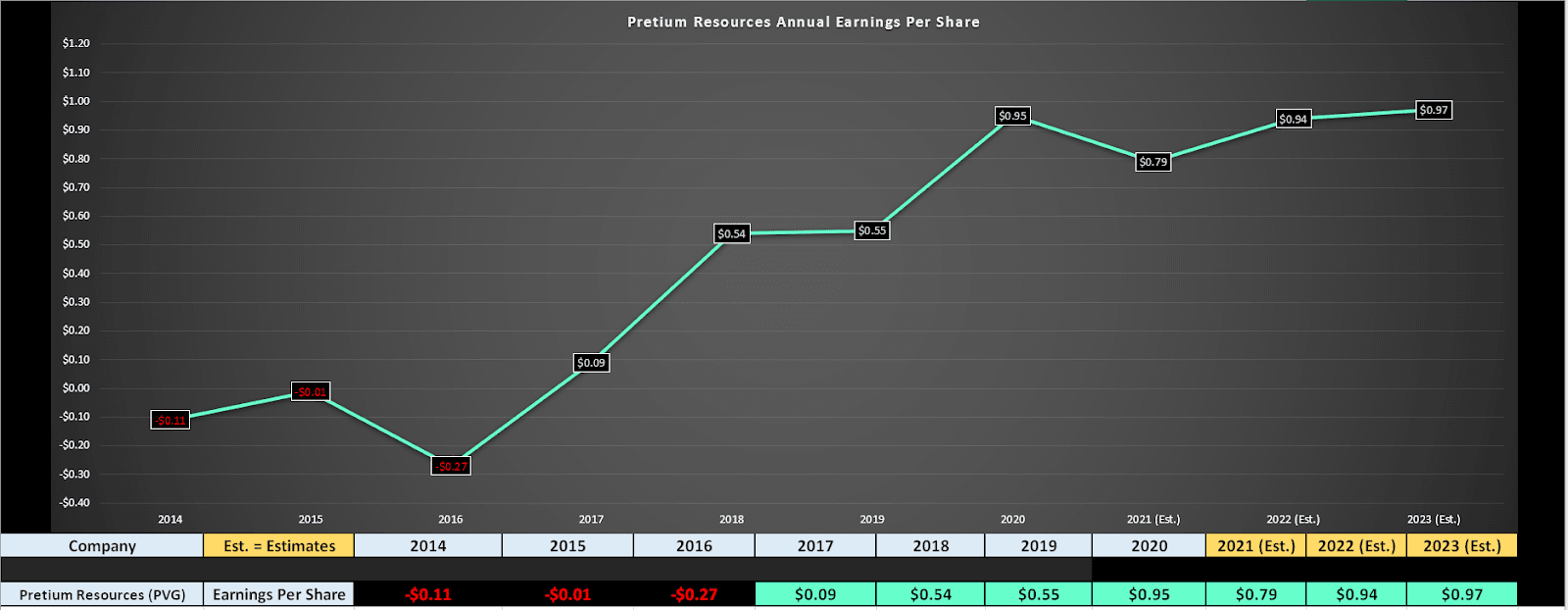

While some investors are disappointed in the slightly lower than expected margins and the weaker gold price than anticipated in 2021, the sharp correction in PVG’s stock looks to have priced in these lower expectations. This is because PVG is currently trading at less than 10x FY2022 annual EPS estimates ($0.94) and less than 9.3x FY2023 estimates of $0.97. This is a very reasonable valuation for a company with 30% plus margins, especially given that annual EPS would come in well above $1.10 in FY2022 if the gold price can head back towards its highs near $2,000/oz. Based on what I believe to be a fair multiple of 13, I see a fair value for PVG of $12.61, translating to more than 40% upside from current levels.

(Source: Company Filings, Author’s Chart)

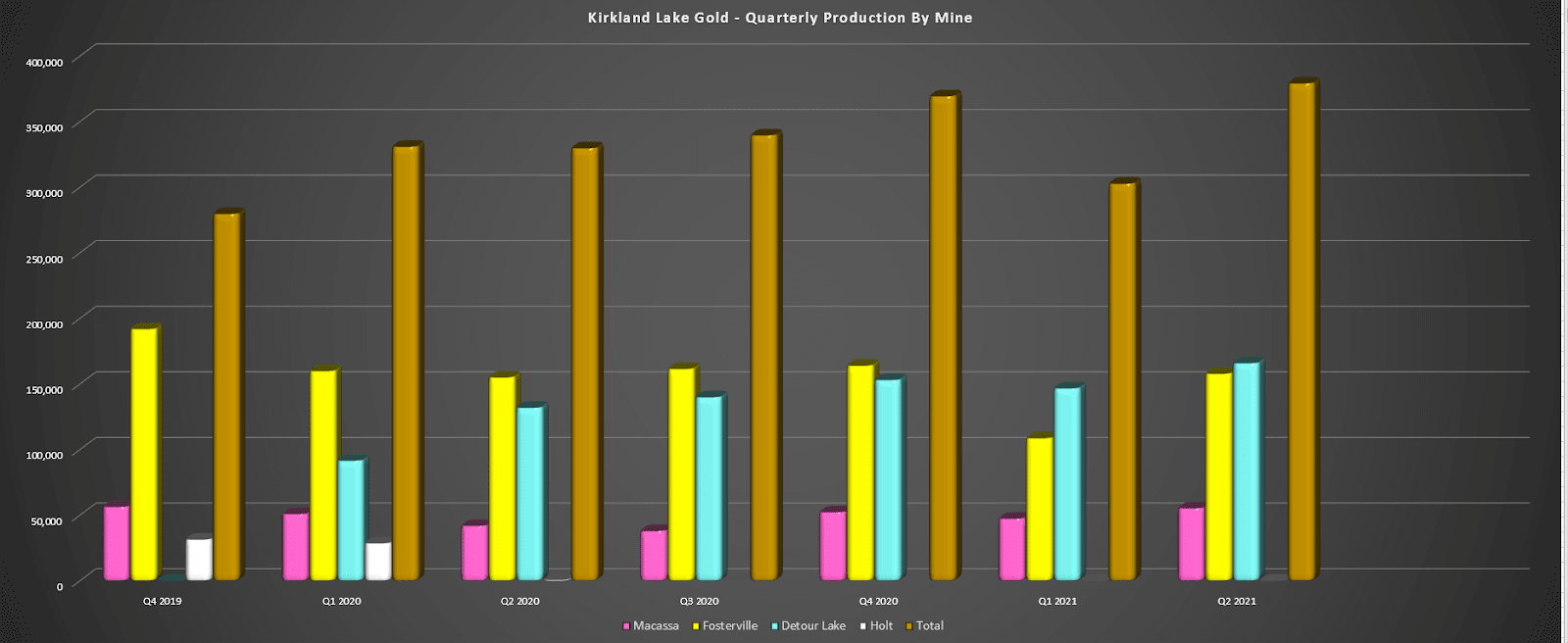

The next name on the list is Kirkland Lake Gold (KL), a company that just came off a massive quarter, with record production of ~379,200 ounces, a 15% increase from the year-ago period. This massive beat relative to expectations was placing its smaller Holt Mine on care and maintenance, which was a small contribution in Q2 2020. However, the company did benefit from easy year-over-year comps due to temporary COVID-19 related shutdowns at the company’s two Canadian mines. Importantly, while this was a less comparable quarter to the year-ago period, KL finished H1 2021 with ~682,000 ounces produced in what is scheduled to be a back-end weighted year. This has set the company up to easily meet the top end of its guidance of 1.4 million ounces. In fact, there’s the potential to trounce this guidance with an annual output of up to 1.42 million ounces if we get another strong quarter out of Fosterville.

(Source: YCharts.com, Author’s Chart)

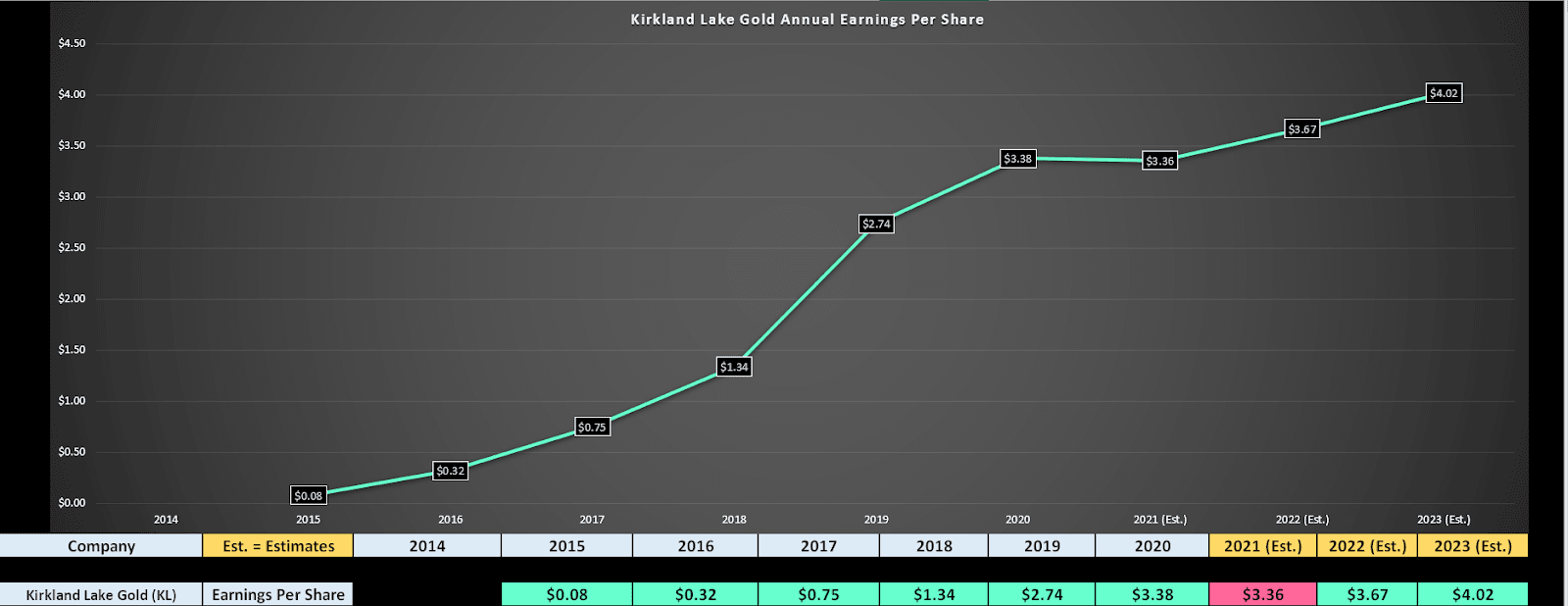

Despite KL being the highest-margin million-ounce producer in the sector with a compound annual EPS growth rate above 40%, the company is currently trading at just over 10x FY2022 annual EPS estimates of $3.67. If we subtract out more than $4.00 per share in net cash to finish FY2021, this valuation drops to barely 9x earnings, with the company also paying a dividend of nearly 2.00%.

It’s worth noting that KL’s payout ratio is less than 25%, so the company could easily increase its dividend by 50% with ease, even at the current gold price. Based on what I believe to be a fair earnings multiple of 15 and FY2023 earnings estimates of $4.02, I see a fair value of $60.30, translating to over 50% upside from current levels. The bonus is a potential ~2.80% yield on cost if KL raises its dividend to $1.10 per by FY2023, which would not surprise me.

The final name on the list is Integra Resources, a micro-cap exploration company that sold its previous exploration company (Integra Gold) for nearly $500MM in 2017. This translated to a massive win for shareholders, and the company looks intent on repeating its success at its DeLamar Project in Idaho, having already proven up over 4 million gold-equivalent ounces, and releasing a very robust Preliminary Economic Assessment in 2019. As shown below, the payback period comes in an incredible 1.48 years at a $1,800/oz gold price and $22.53/oz silver price, with an After-Tax NPV (5%) of $675.4 million. This figure dwarfs ITRG’s current market cap of $151MM.

(Source: Integra Resources Company Presentation)

Typically, developers trade at 0.4x – 0.50x NPV (5%) at this stage of the development cycle. Even assuming just 0.40x NPV (5%) and a more conservative metals price assumption of $1,700/oz gold and $21.28/oz silver, this would translate to a fair value of $242MM. If we divide this by 56MM shares outstanding, this translates to a fair value of $4.32 per share, or more than 60% upside from current levels. This makes ITRG one of the most undervalued names in the sector, with a very significant margin of safety baked in at current levels.

While all of the above names could continue to trade in a volatile manner if gold prices can’t get back above $1,800/oz before the end of summer, the comforting news is that the gold price weakness looks to be priced into each name. This is especially true for KL, which has one of the top-200 highest compound annual earnings growth rates on the US Market yet trades at a single-digit PE based on FY2023estimates. KL looks like the best for risk-averse investors, and I continue to see the stock as a Strong Buy even after the rally from $33.00 to $38.00.

Disclosure: I am long GLD, KL

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

KL shares were trading at $39.57 per share on Wednesday afternoon, up $0.24 (+0.61%). Year-to-date, KL has declined -4.12%, versus a 18.35% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| KL | Get Rating | Get Rating | Get Rating |

| GDX | Get Rating | Get Rating | Get Rating |

| PVG | Get Rating | Get Rating | Get Rating |

| ITRG | Get Rating | Get Rating | Get Rating |