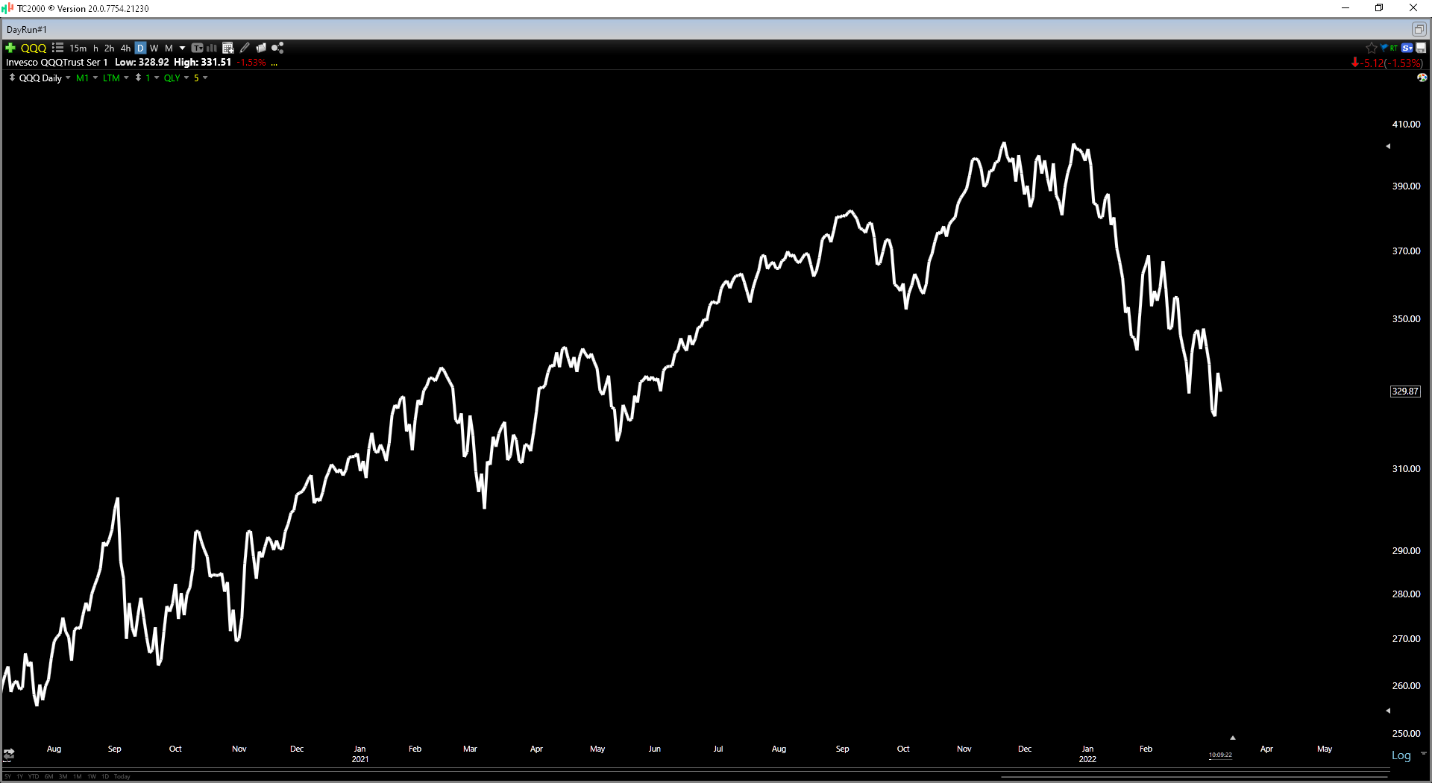

It’s been a turbulent start to the year for the Nasdaq 100 Index (QQQ), with the ETF finding itself down 18% year-to-date. This is one of the worst starts for the index in history, with geopolitical tensions, elevated valuations, and rising rates putting a dent in several Nasdaq constituents. While this has certainly been painful, it’s creating an opportunity for investors that have been patient and have maintained cash positions to take advantage. Given that we still have not seen panic selling, I’m in no rush to add exposure just yet. However, with the market already down more than 15%, it’s worth adding high-quality names to one’s shopping list, and we’ll look at two names worthy of consideration below:

(Source: TC2000.com)

Microsoft (MSFT) and Qualcomm (QCOM) were two of the better performing tech stocks in Q4 2021, up 41% and 19% after strong years from both companies and strong forward guidance. In QCOM’s case, the company grew annual EPS by more than 90% last year on the back of healthy margin expansion, while MSFT enjoyed a 38% increase in annual EPS to $7.97 per share. Despite this impressive growth, both companies are expected to see meaningful growth in annual EPS over the next two years, making them two of the highest-growth companies in the US market, despite their high market caps. Let’s take a closer look at both companies below:

As the chart below shows, Microsoft has enjoyed years of steady growth in earnings, growing EPS at a compound annual growth of more than 20% since 2015. This is incredible for a company of its size, and MSFT’s most recent quarter was no different, reporting revenue growth of 20% ($51.7BB) and 22% growth in annual EPS to a record $2.48. The major news for the company was the acquisition of out of favor Activision Blizzard (ATVI) for $68BB in cash, an accretive deal that will add more than $9BB in revenue per annum with no additional share dilution.

(Source: YCharts.com, Author’s Chart)

While the premium paid for ATVI of more than 40% may appear steep, I believe MSFT paid the right price for the company, waiting for ATVI to be significantly out of favor amid walkouts and strikes and degraded company culture. It’s also a very logical acquisition for Microsoft from a synergistic standpoint, given that MSFT will bring iconic franchises like Warcraft, Diablo, Overwatch, Call of Duty, and Candy Crush in-house and add significant potential in the burgeoning E-Sports market.

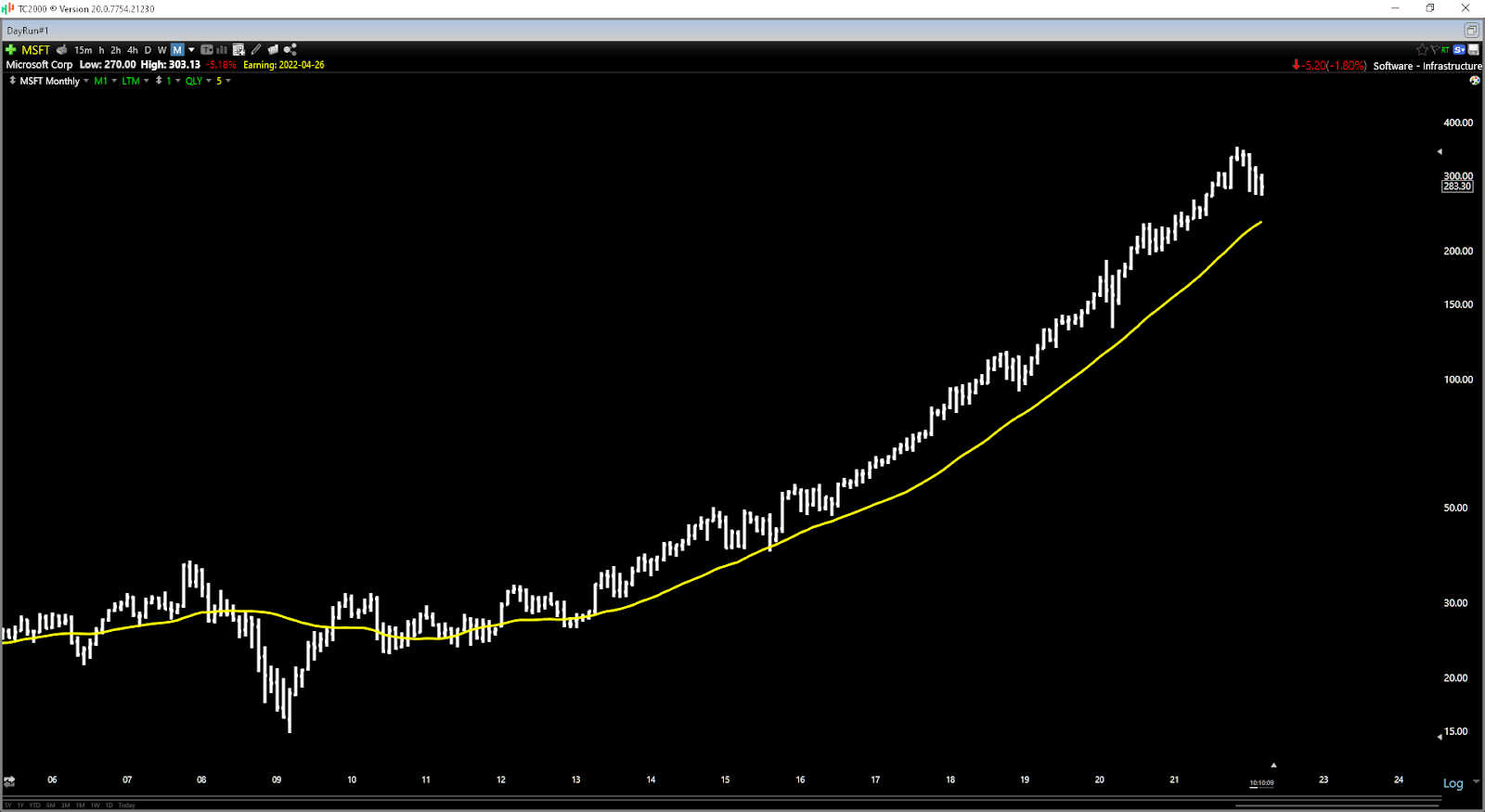

If we look at the chart below, this transaction combined with MSFT’s legacy business is expected to help the company maintain its ~20% compound annual EPS growth rate, with FY2023 and FY2024 earnings estimates sitting at $10.86 and $12.85, respectively. Assuming Microsoft meets these estimates, its compound annual growth rate will maintain its recent growth trajectory, which is an incredible feat for a company of its size with a $2TT market cap. The only problem is that while this growth is impressive, MSFT still doesn’t appear to offer enough of a margin of safety, hence why investors should be patient when it comes to buying the dip.

(Source: TC2000.com)

The chart above shows that MSFT remains in a strong uptrend despite its recent correction and trades at approximately 22x FY2024 earnings estimates. I believe a more reasonable valuation that would bake in a margin of safety is 19x FY2024 estimates or less, and this level happens to line up with the stock’s monthly moving average (yellow line), where it’s found strong support in the past.

So, while I am neutral on MSFT currently, given that the stock does not offer a meaningful margin of safety, I believe it’s a name to keep a very close eye on if we see continued market weakness. Based on my view that MSFT to find support at its rising monthly moving average and the fact that the valuation would become more attractive at 19x FY2024 earnings, I believe the ideal buy-point is at $237.00 or lower.

Moving over to Qualcomm, the company is a rare breed. This is because QCOM offers not only growth but also value after its recent correction. The company is firing on all cylinders from a growth standpoint, reporting 30% revenue growth in its most recent quarter and meaningful margin expansion. This growth was driven by growth in handsets (+ 42% year-over-year) and the Internet of Things (41%). It’s worth noting that this 30% revenue growth rate lapped 62% growth in the year-ago period, making the growth even more impressive.

(Source: YCharts.com, Author’s Chart)

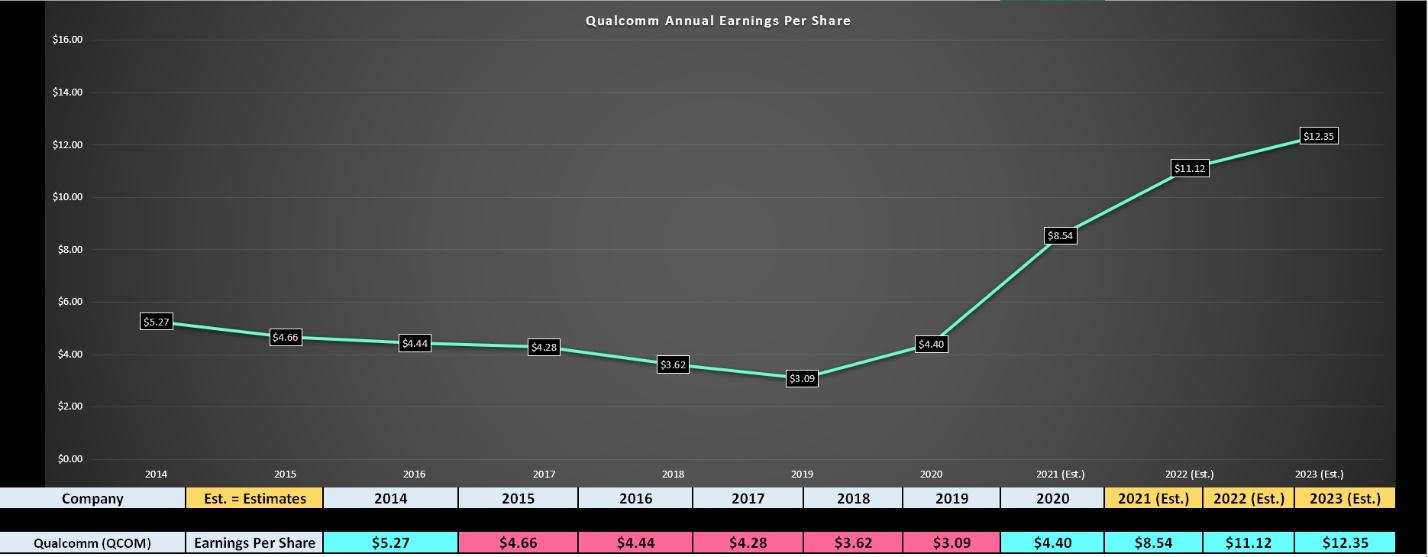

If we look at the company’s earnings trend below, we can see that this combination of strong sales growth and margin expansion has led to significant growth in annual EPS, with annual EPS up 94% year-over-year ($8.54 vs. $4.40). Importantly, this growth is expected to persist, with FY2023 earnings estimates sitting at $12.35, translating to more than 45% growth vs. last year. Assuming QCOM can meet these estimates, the company would have a compound annual EPS growth rate of 41% (FY2019 to FY2024).

Despite this outstanding growth and what’s a very exciting story, QCOM trades at a dirt-cheap valuation of just 12.3x FY2024 earnings estimates, making it one of the most attractively priced tech stocks globally. Based on what I believe to be a conservative earnings multiple of 17, I see a fair value for the stock closer to $210.00 per share. So, if the stock sees any further weakness and heads lower to re-test its monthly moving average near $130.00, I would view this as a very low-risk buying opportunity, and I would strongly consider starting a position in the stock.

(Source: TC2000.com)

While several high-flying tech names continue to trade at more than 15x sales despite the violent correction in the tech space, MSFT and QCOM are becoming more reasonably valued and look like great buy-the-dip candidates. Given that I would not be surprised to see further weakness in the market and a new low, I am not in a rush to purchase either stock, but I do have them near the top of my watch lists. For now, I see the low-risk buy points for both stocks being at $237.00 and $140.00, respectively.

Disclosure: I have no positions in any stocks mentioned

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one’s portfolio.

Want More Great Investing Ideas?

MSFT shares were trading at $285.49 per share on Thursday afternoon, down $3.01 (-1.04%). Year-to-date, MSFT has declined -14.94%, versus a -10.62% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| MSFT | Get Rating | Get Rating | Get Rating |

| QQQ | Get Rating | Get Rating | Get Rating |

| QCOM | Get Rating | Get Rating | Get Rating |