As if investors didn’t have enough to worry about right now, last week the media began throwing lots of scary headlines at us about the Fed “buying hundreds of billions worth of bonds in the repo market for the first time since the Financial Crisis.”

The market didn’t much react to that news since it was obsessed with what the Fed would do on Wednesday regarding its Federal Funds Rate or FFR.

But plenty of doomsday prophets were out in force, warning that another 50+% crash in the S&P 500, Dow Jones Industrial Average or Nasdaq might be nigh (Glenn Beck was the most notable example).

Fear leads to terrible investing decisions. In fact, Jeff Miller, one of my personal economic gurus goes as far as to say that “Trying to time the market using headlines is a road to ruin.”

Since the cure for fear is facts, here are three facts you need to know about what the Fed is actually doing with the repo market, why, and most importantly, why a huge market crash is almost certainly not coming soon.

Fact 1: What the Repo Market Is

The repo market is about $3 trillion in size and possibly the most important large financial market most people have never heard of.

Repurchases, or repos, are just what most big financial companies use to ensure adequate short-term liquidity to process payments and make sure their books are balanced each financial day.

For example, a company like JPMorgan Chase processes tens of millions of transactions each day thinks like check cashing, and credit card payments. So here’s an example of how repo works and how the Fed plays a role.

The Fed Fund Rate or FFR is the rate Wall Street is obsessed with, serving as a proxy for short-term interest rates. What the FFR actually is, on a literal basis, is the overnight inter-bank lending rate the Fed wants the repo market to operate at.

For example, if JPMorgan needs a quick case to cover daily credit card charges, then it may sell $100 worth of US Treasury bonds it owns as part of its reserves to Bank of America. In exchange for $100 in cash (from BAC’s short-term liquidity reserves) JPMorgan is basically selling its bonds to BAC with an agreement to buy them back the next day at a slightly higher price (2.25% interest rate but charged for one day).

The FFR is actually a 25 basis point range, that was just lowered to 1.75% to 2.0%. What that means is that now whenever a bank (or other financial company) needs to access the repo market, they will sell high-quality, super liquid collateral (such as US treasury bonds) to another financial company, and then buy them back the next day for a small premium.

So what happened last week to make the Fed flood the repo market with over $200 billion by purchasing bonds with money it conjured from thin air?

Fact 2: Why The Fed Is Buying Hundreds of Billions of Bonds to Stabilize the Repo Market

What happened during the Financial Crisis was that most big banks were gambling with dangerous amounts of sub-prime mortgage-based bonds and credit default swaps. These toxic assets were used as collateral for repo loans.

When the housing market began to implode, US mortgage defaults soared and suddenly the cash flow streams supporting the fundamental value of those loans began to collapse.

Banks had no idea what subprime based loans were actually worth, and thus the repo market seized up.

(Source: Cullen Roche)

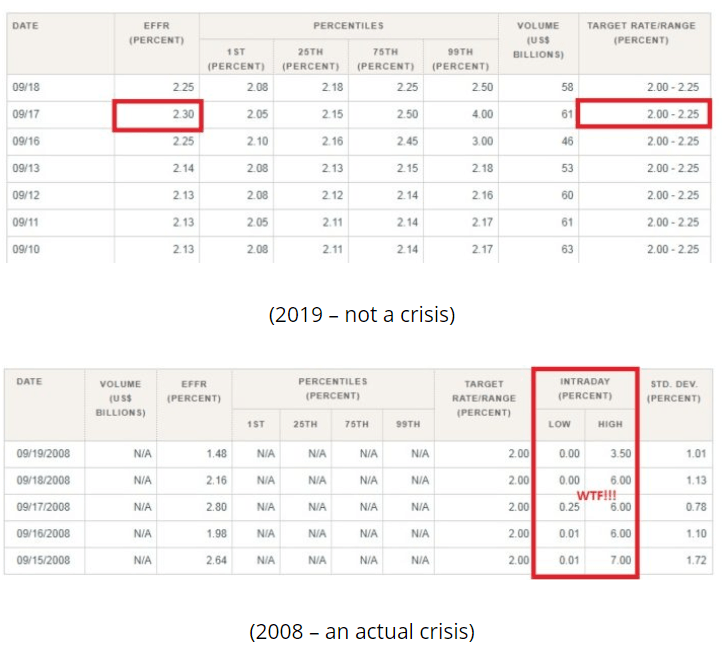

Here is a good example of what happened in 2008 and what happened last week. In 2008 the effective fed funds rate was actually pretty stable, day to day (thanks to the Fed’s repo actions at the end of each day). But note what happened intraday. At the time 2.0% was the target FFR, or what financial companies were supposed to charge each other for overnight lending in the repo market.

The intraday repo rates ranged from 0.01% to 7% on September 15th, 2008, showing that the repo market was not just broken, but shattered.

Now contrast September 17th, 2019. the effective FFR (repo rate) closed that day at 2.3%, 5 basis points above the Fed’s target range. For a very brief time, the intraday repo rate hit as high as 4%, but the Fed stepped in with $75 billion in bond buying from financial institutions, to stabilize the repot market which settled down the next day.

What caused the repo market to go slightly crazy at all? Four main factors

- stricter capital requirements for major banks (which limits how much of their reserves can be used to cover short-term liquidity needs)

- the Fed’s $500 billion in recent bond roll-offs (tightened the money supply a bit)

- timing of companies needing to pay corporate taxes by October 15th

- extra issuances of US treasury bonds due to the higher budget deficit (which soaked up bank liquidity)

Last Friday the New York Fed said it planned to do daily repo bond buys up to $75 billion per day and possibly also $30 billion per week in longer duration (14 day) repo deals, to stabilize the market until October 10th.

But here’s the most important fact of all to know, which is that no financial crisis, recession or market crash is likely barreling down on us.

Fact 3: This Is Almost Certainly NOT the Start of Another Financial Crisis

It’s important to know that small spikes in short-term credit markets are quite common as you can see in the first chart.

(Source: Cullen Roche, Jeff Miller)

Second, it’s important to know that while the Fed’s much larger balance sheet (from $4.5 trillion in bond-buying) meant that no repo actions were needed in the last 10 years, the Fed’s bond-buying to stabilize repo is nothing new.

Prior to the Financial Crisis, the Fed was doing overnight repo stabilization bond buys very frequently, thousands of times over many years. Remember that what broke the liquidity markets in 2008 and 2009 was the toxic nature of the collateral used in the repo market, not the repo market itself.

Here’s Cullen Roche (author of Pragmatic Capitalism) summarizing the “drama” of last week very well

On the 17th of September, 2019 the rate was a measly 5 bps off. In other words, while the rate was higher than the Fed might have liked, it was actually very close to target. This is not indicative of a panic or a crisis or really anything other than what seems to be a very short-term liquidity squeeze that the Fed resolved in a timely manner. So, for now I wouldn’t overreact to all of this. It sounds fancy and scary, but it’s pretty much a garden variety leak in our financial plumbing. That sort of stuff happens every now and then so don’t let your local financial newspaper scare you into thinking that 2008 is right around the corner.” – Cullen Roche

Remember that we live in an uncertain era when the Fed wasn’t sure how large its balance sheet needed to be to ensure adequate liquidity to financial markets. Now the Fed knows, more than it is now.

And as the Fed showed last week, with over $200 billion in bond buying (undoing 40% of its two year QT initiative) and now pledging to potentially push up the balance sheet to record highs if need be, there is very little cause for concern that short-term credit, the lifeblood of modern commerce, is going to grind to a halt anytime soon.

Bottom Line: Keep Calm And Carry on, Market Doomsday Isn’t Here

Ever since the financial crisis ended, investors have been waiting for signs of another huge crash. The media knows this and so many outlets and pundits will hype up any scary-sounding risk to imply another Great Recession (or worse) is right around the corner.

The repo market is especially easy to do this with since very few people know what it is, how it operates or that the Fed has historically done overnight repo bond buys not just a few times, but thousands of times, as a normal part of its mandate to ensure a stable financial system.

Hopefully, the 3 facts presented in this article can keep you calm and rational, and help you avoid making knee-jerk, fear-based portfolio decisions that you’ll likely regret later.

SPY shares were trading at $299.48 per share on Tuesday morning, up $1.27 (+0.43%). Year-to-date, SPY has gained 20.94%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Adam Galas

Adam has spent years as a writer for The Motley Fool, Simply Safe Dividends, Seeking Alpha, and Dividend Sensei. His goal is to help people learn how to harness the power of dividend growth investing. Learn more about Adam’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| SPY | Get Rating | Get Rating | Get Rating |