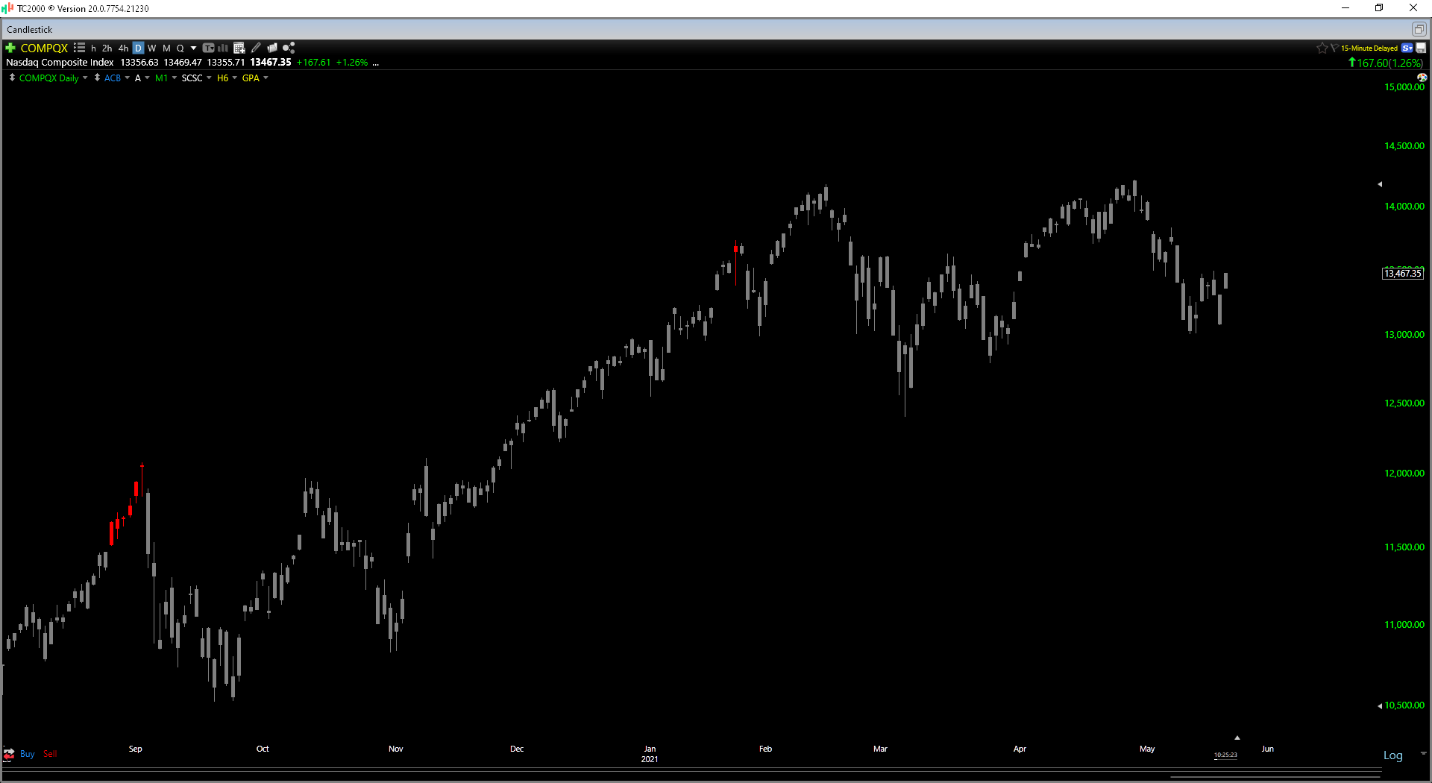

Thus far, it’s been a turbulent year for the Nasdaq Composite, with the index starting 2021 with a 15% gain, before wiping out all of its year-to-date gains with inflation and the prospect of higher rates spooking the market. Currently, the Nasdaq is trying to find its footing near its 100-day moving average, but with minimal fear out there and still a significant amount of complacency, it’s unclear whether the bottom is in yet. While many stocks remain expensive after being bid up relentlessly last year, two QQQ constituents are reasonably valued after blowout Q1 earnings reports. So, if the market weakness continues, they look like two potential ideas to buy on dips.

(Source: TC2000.com)

Alphabet (GOOG) and Tesla (TSLA) have little in common other than being neighbors in the Nasdaq-100 Index, focusing on making self-driving a reality over the long run, and delivering solid results in their Q1 reports. In Alphabet’s case, the company smashed revenue estimates and reported $55.3BB in revenue, a massive beat vs. consensus of ~$52BB. This translated to 34% growth year-over-year and the company’s strongest quarter for sales growth in over two years. In Tesla’s case, the company beat revenue by more than $110MM with revenue of $10.4BB while also posting a massive beat on automotive gross margins of more than 200 basis points. Let’s take a look at Alphabet below:

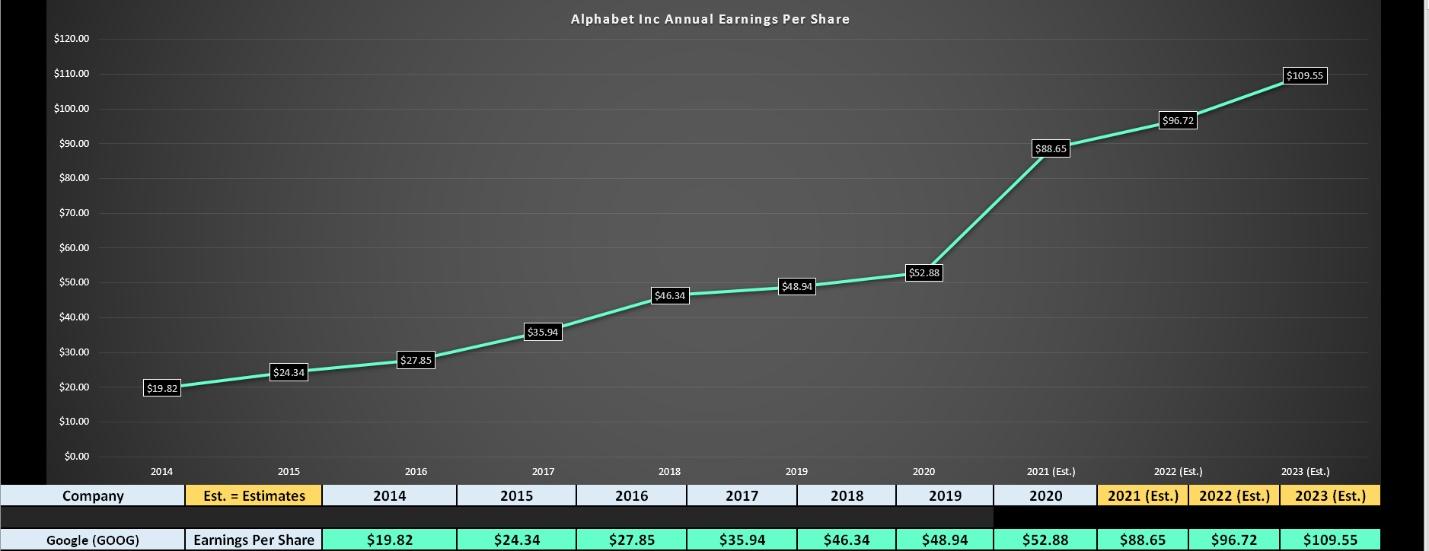

Alphabet had an incredible quarter in Q1 with annual EPS up 98% year-over-year to $21.58, and revenue soaring by 34% to $55.3BB. This solid quarter was helped by the third quarter in a row of accelerating ad growth for the tech giant, with a strong recovery since the tough period in April to May of last year when things were looking a bit dicier. Based on FY2021 estimates, Alphabet is expected to see a massive acceleration in annual EPS this year, with estimates sitting at $88.65 vs. $52.88 reported last year. This would translate to high double-digit growth vs. two years in a row of single-digit growth. The stock looks to be beginning to price some of this in, with Alphabet being a top performer in the Nasdaq-100 with a 34% return year-to-date.

(Source: YCharts.com, Author’s Chart)

Despite an incredible compound annual EPS growth rate of more than 22% for Alphabet based on FY2021 estimates ($88.65 vs. $19.82), the stock is trading at less than 27x forward earnings. This is a dirt-cheap valuation for a diversified tech giant, especially when the stock is coming off one of its best quarters in the past two years. Even if we assume a conservative earnings multiple of 30 and FY2022 annual EPS of $96.72, this gives us a fair value of $2,900, or more than 20% above current levels. Ideally, if baking in a 25% margin of safety to fair value, this would line up with a buy zone below $2,190.

(Source: TC2000.com)

If we look at the above chart, we can see that GOOG has support near $2,090, where the stock spent several weeks consolidating, and where its medium-term uptrend comes in. For investors looking to buy the dip, this would be the best spot to start a position, as it would line up with technical support and inside the fundamental buy zone. For now, I see GOOG as a Hold, but further weakness should present a buying opportunity. Let’s take a closer look at Tesla below:

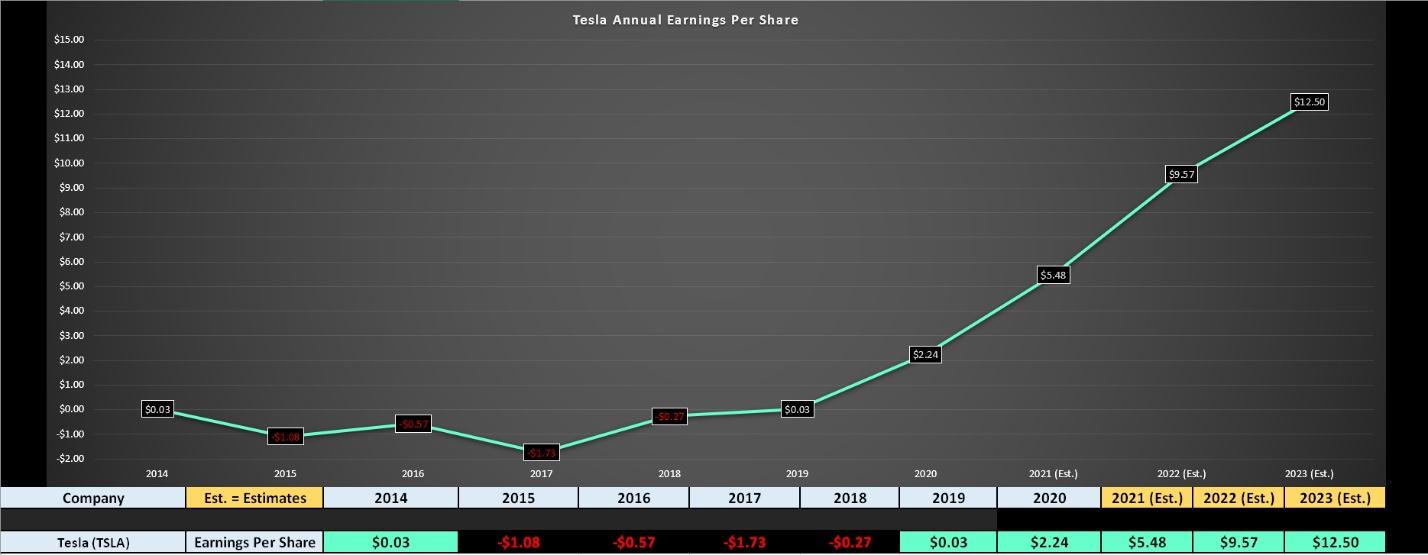

While Tesla might appear expensive on a price to earnings basis, the market leader in a rapidly growing industry typically trades at a premium valuation, and assuming an earnings multiple of 70 and earnings estimates of $9.57 in FY2022, the stock is actually trading at a decent discount to fair value ($669.90). Looking ahead further to FY2023, annual EPS estimates are sitting at $12.50, moving fair value to $875.00. Obviously, there is a lot of time between now and the FY2022 and FY2023 estimates, but with the market looking ahead by 12-18 months, it makes no sense to be valuing the stock on either the FY2020 results ($2.24) or FY2021 estimates ($5.48) and proclaiming the stock is expensive.

During Q1, Tesla reported 74% revenue growth year-over-year, which is unheard of for a company of its size, and also posted record vehicle production of ~180,300. This was a 76% increase year-over-year despite supply chain inefficiencies due to COVID-19. While the company’s average realized sales price was down, TSLA posted automotive gross margin that was up 100 basis points year-over-year to 26.5%, while storage deployed soared to 445 MWh. With the company continuing to trounce most analyst estimates on deliveries and production, I would not be surprised by a big beat on current FY2022 estimates.

(Source: YCharts.com, Author’s Chart)

So, is the stock a Buy here?

Generally, I prefer at least a 30% discount to fair value to buy, and with a fair value of $669.90, this would translate to ~$469.00 per share. This also lines up with the stock’s most recent breakout level, which should act as new support if the stock’s correction continues. Obviously, there’s no guarantee that the stock heads this low, but the $470.00 – $495.00 area would be a much lower-risk area to get involved in the stock. So, for investors looking for the best way to play the EV Market with the industry leader, TSLA is a name to watch if we do see a lower low in the ~$500.00 area.

(Source: TC2000.com)

The Nasdaq-100 has pulled back considerably from its highs, and GOOG and TSLA look to be two great ways to play the dip if this correction continues. At current levels, I still don’t see enough fear to suggest a sustainable bottom is in, so I continue to hold elevated cash and would begin to get interested in TSLA and GOOG if we see a pullback closer to $500 and $2100, respectively.

Disclosure: I have no positions in any stocks mentioned

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

TSLA shares were trading at $575.18 per share on Thursday afternoon, up $11.72 (+2.08%). Year-to-date, TSLA has declined -18.49%, versus a 11.25% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| TSLA | Get Rating | Get Rating | Get Rating |

| GOOGL | Get Rating | Get Rating | Get Rating |

| GOOG | Get Rating | Get Rating | Get Rating |