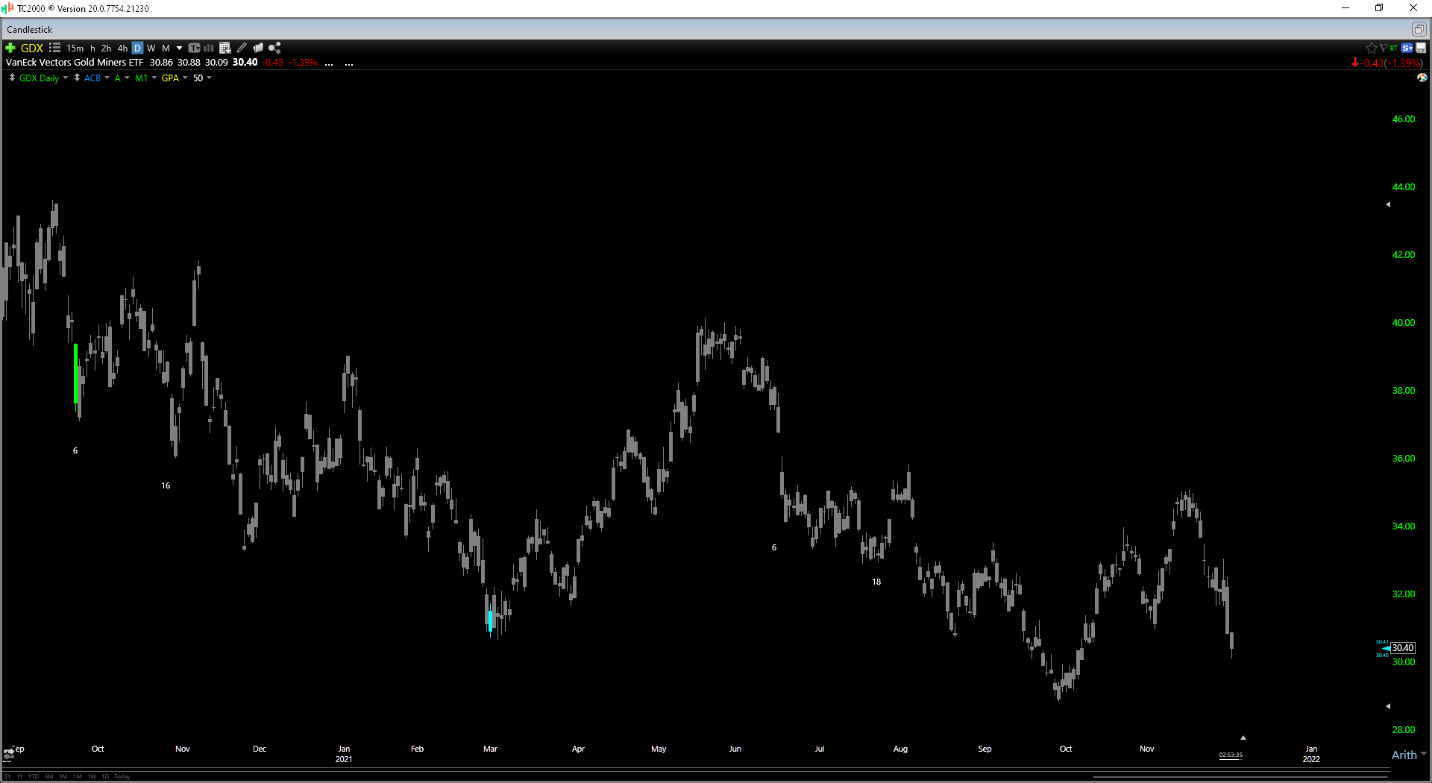

It’s been a rough year thus far for investors in the Gold Miners Index (GDX), with the ETF being one of the worst performers year-to-date. This is evidenced by its (-) 16% return vs. a 22% return for the S&P-500 (SPY), and understandably, sentiment is at its worst levels in years.

(Source: TC2000.com)

The good news is that the pervasive negative sentiment has contributed to some of the most attractive valuations we’ve seen in more than five years, with the majority of producers trading at a discount to net asset value. This update will look at three producers trading at massive discounts to fair value and why they should outperform over the coming year.

Agnico Eagle (AEM), Barrick Gold (GOLD), and Alamos Gold (AGI) all have very different production profiles, producing 3.4 million, 5 million, and 500,000 ounces per annum respectively. However, all three have high-quality management teams, strong track records, and very bright futures if they can deliver on their plans.

For Agnico Eagle, this includes a major merger with Kirkland Lake Gold which will combine two of the best companies sector-wide into a massive Canadian gold producer with industry-leading for costs. In Barrick’s case, the company continues to have tremendous exploration success and production growth at Goldrush/Fourmile in Nevada and a large tailings/throughput expansion on deck at Pueblo Viejo. Finally, for Alamos Gold, the company is looking to grow production by 50% over the next four years, with the main pillar of this growth being Island Phase III, a ~240,000-ounce producer with sub $650/oz all-in sustaining costs. Let’s look at the three companies below:

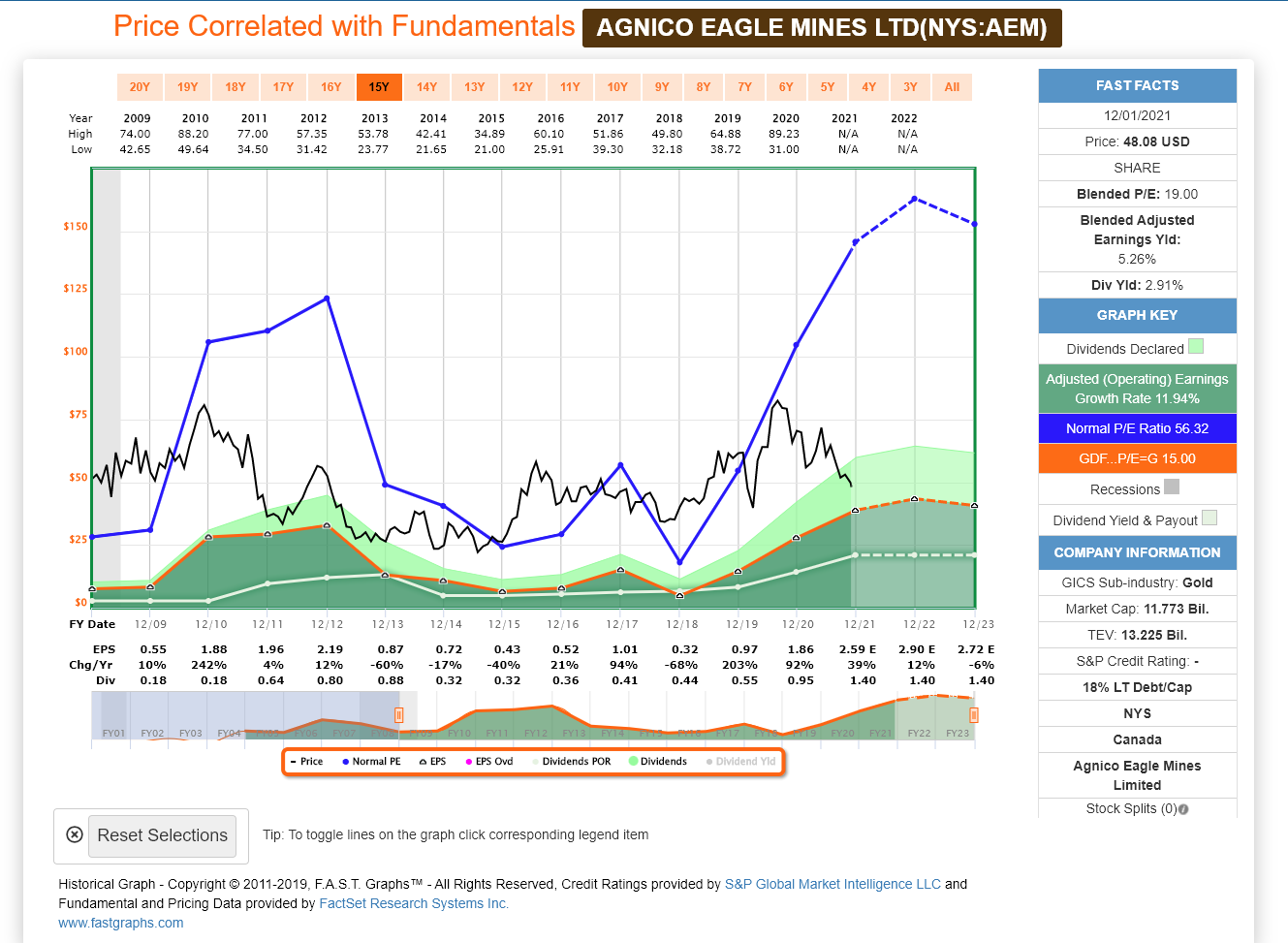

Beginning with Agnico Eagle, the company has found itself down 30% year-to-date following the merger with Kirkland Lake Gold and near one of the most significant oversold conditions it’s seen in years. This has left the stock trading below 1.0x P/NAV, which is a dirt-cheap valuation for a producer of its size, with more than 95% of gold production coming from Tier-1 jurisdictions.

(Source: FASTGraphs.com)

Based on estimated annual EPS of more than $3.50 in FY2022, the stock now trades at less than 14x next year’s earnings estimates vs. a historical earnings multiple of more than 30x earnings. Even in a more conservative scenario, with the ceiling I typically use of 22x earnings for miners, fair value comes in above $70.00 per share. This points to more than 40% upside from current levels to fair value, while investors collect a ~3.0% dividend yield.

Given Agnico’s industry-leading margin profile, enviable development pipeline (Upper Beaver, Hammond Reef, Santa Gertrudis), and excess mill capacity in the Kirkland Lake Mining camp, which will contribute to synergies, I see the stock as a staple for investors interested in gaining precious metals exposure. In summary, I see this pullback below $50.00 as a low-risk buying opportunity.

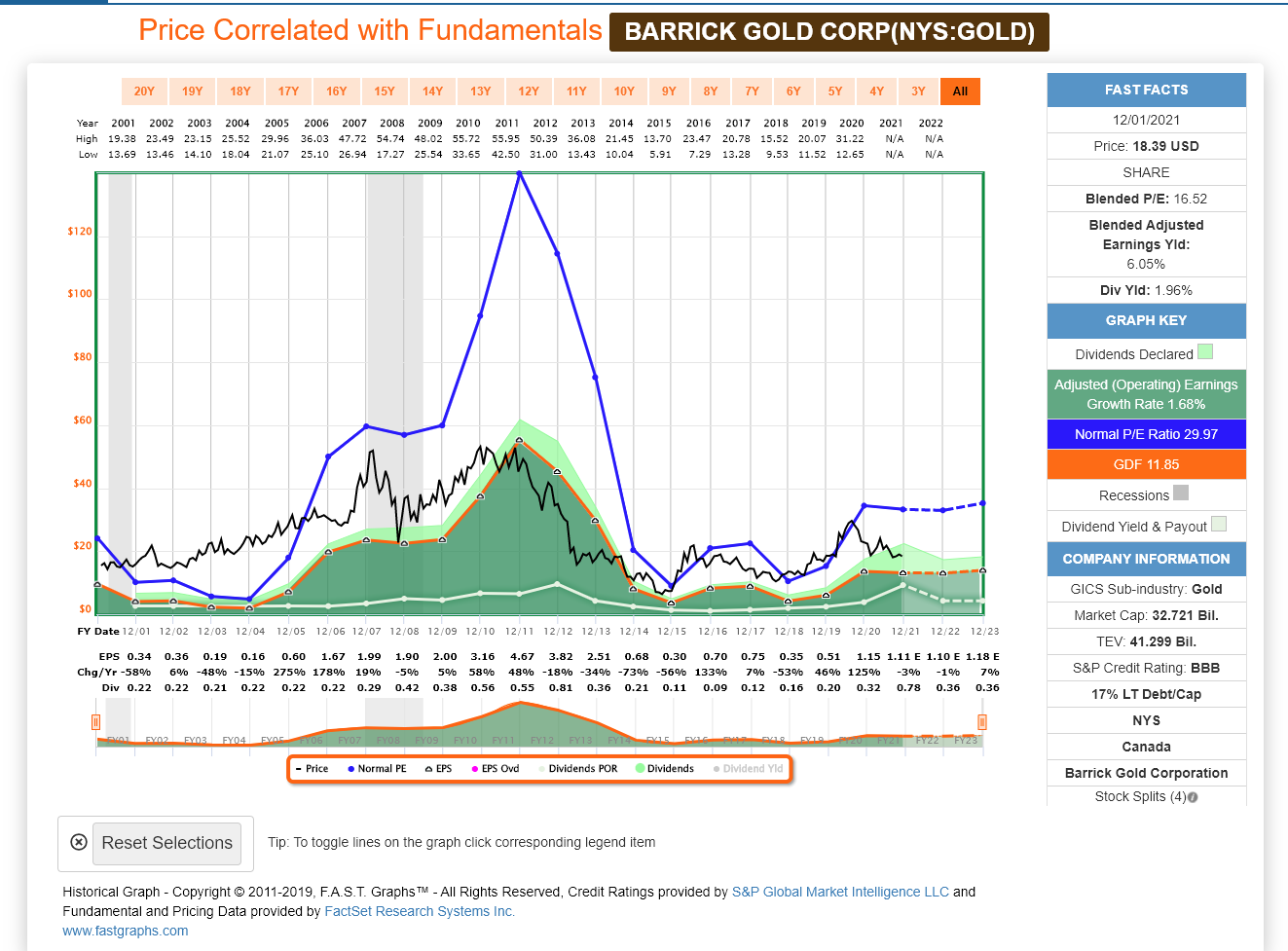

Moving over to Barrick Gold, the company is the 2nd largest producer globally and just came off a tough quarter, which explains the recent weakness in the stock. This was evidenced by the company’s 20% decline in revenue year-over-year. However, the decline in revenue was related to a one-time issue (mechanical mill failure at its Goldstrike roaster) and a major gold price headwind, with Barrick coming up against a record gold price in the year-ago period.

(Source: FASTGraphs.com)

While this was undoubtedly disappointing, the underwhelming results look to be priced into the stock, with Barrick trading near $18.00 per share and at just 16x trailing earnings. Looking ahead to FY2023 estimates, Barrick is expected to earn between $1.18 -$1.38 depending on the gold and copper price, leaving the stock trading at closer to 14x FY2023 earnings estimates. If we compare this to the stock’s historical earnings multiple of 22, this points to significant upside for the stock. So, while it’s easy to be negative on Barrick after what’s been a tough year, I believe the correction has nearly run its course, with Barrick approaching a major bottom.

It’s worth noting that in addition to being cheap, Barrick continues to advance its Goldrush and Fourmile projects, which make up a major growth pillar for the company in Nevada. Meanwhile, the company continues to see impressive exploration success at other sites in Nevada, with the shared Nevada Gold Mines Joint Venture being the largest mining complex globally. With the barriers torn down around the properties following the joint-venture, I would expect meaningful reserve growth over the next few years from this mining complex, which makes Barrick an exciting exploration story and a relatively safe way to gain exposure to the gold price.

The final name on the list is Alamos Gold, a much smaller name with a production profile of ~500,000 ounces per annum. Alamos Gold recently cut its FY2021 production guidance slightly due to a weaker than expected H2 at its Mexican Mulatos Mine. This has caused many investors to throw in the towel on the stock after what’s been a tough year from a share-price performance standpoint. However, for those familiar with the Alamos story, the company is going to look much different in 3-4 years, so there’s no reason to get hung up on its disappointing quarterly results.

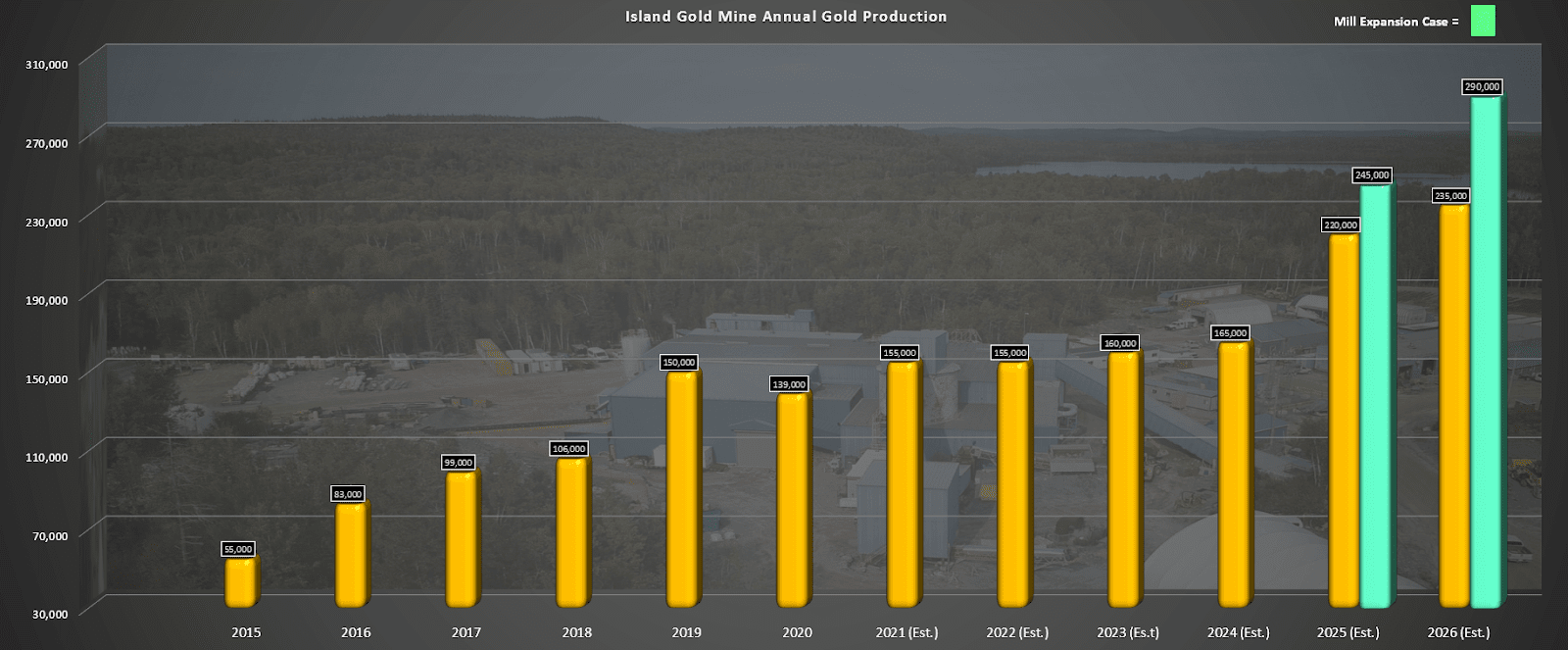

(Source: Company Filings, Author’s Chart & Estimates)

As discussed earlier, Alamos has a very impressive organic growth profile and is planning to grow production to ~750,000 – ~775,000 ounces in 2025/2026. This is based on a significant expansion at its Island Gold Mine and plans to bring its Lynn Lake Project online in Manitoba. Most importantly, this growth comes at better margins than its current cost profile ($750/oz vs. $1,050/oz), and it boosts Alamos production in Canada, a much more attractive jurisdiction than Mexico. So not only is Alamos set to grow production by ~50% in the next four years, but its costs will drop dramatically, and its jurisdictional profile will improve immensely.

At a current share price of $7.25, Alamos Gold trades at barely 14x FY2023 earnings estimates and below 0.80x P/NAV. This is despite the fact that the company continues to make new discoveries at its Island Gold Mine, is transitioning to a much lower-cost mine in Mexico next year (La Yaqui Grande), and has one of the best growth profiles sector-wide. So, with the stock sitting at its cheapest levels in years, I see the stock as a steal at current levels.

After years of capital destruction in the past bull market cycle, it’s understandable that gold miners are not at the top of investors’ shopping lists. However, we are seeing much more capital discipline in this cycle, significant free cash flow generation, and the valuations are the best they’ve been since the end of the 2015 bear market. Therefore, for investors looking for value in a market where it’s difficult to find it, I see AEM, AGI, and GOLD as three top picks in the gold mining space.

Disclosure: I am long AEM, AGI

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

AGI shares were trading at $7.30 per share on Thursday afternoon, down $0.15 (-2.01%). Year-to-date, AGI has declined -16.06%, versus a 23.72% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| AGI | Get Rating | Get Rating | Get Rating |

| AEM | Get Rating | Get Rating | Get Rating |

| GOLD | Get Rating | Get Rating | Get Rating |

| AGI | Get Rating | Get Rating | Get Rating |