We’ve seen a massive sea change in the Gold Miners Index (GDX) relative to last year, with the ETF up more than 20% year-to-date, a clear change of character from its lethargic price action in 2021. This sharp rally has been driven by a steady bid under the gold price (GLD), which sits above $1,900/oz, providing a meaningful boost to miners’ profits. This is a meaningful tailwind for the group, and despite these near-record gold prices, many miners continue to trade at their most attractive valuations in years. In this update, we’ll look at three names that look to be excellent buy-the-dip candidates.

(Source: TC2000.com)

Osisko Gold Royalties (OR), Nomad Royalty (NSR), and Alamos Gold (AGI) don’t have a ton in common, with the former being a mid-cap royalty company, the second one being a small-cap royalty company, and the latter being a diversified gold producer. However, these three companies do all share one key trait: growth. In fact, the average compound annual production/attributable production growth rate for these three companies is more than quadruple that of the industry average, and they’re led by strong management teams, suggesting a high probability of executing their plans successfully.

Beginning with Osisko Gold Royalties, the company has nearly 20 producing royalties, with its flagship royalty being a 3-5% net smelter return royalty on Canada’s 2nd largest gold mine: Canadian Malartic. For those unfamiliar, royalty/streaming companies pay developers and producers upfront to finance construction/development and expansions at specific assets. They receive a portion of metals over the asset’s mine life in exchange. This is a very attractive business model, given that royalty companies do not need to continue committing capital but in many cases can enjoy royalties for 20+ years at assets. Given that they are not operating the mines and are not required to fund sustaining capital at the operations, royalty companies enjoy some of the highest margins sector-wide at more than 90%.

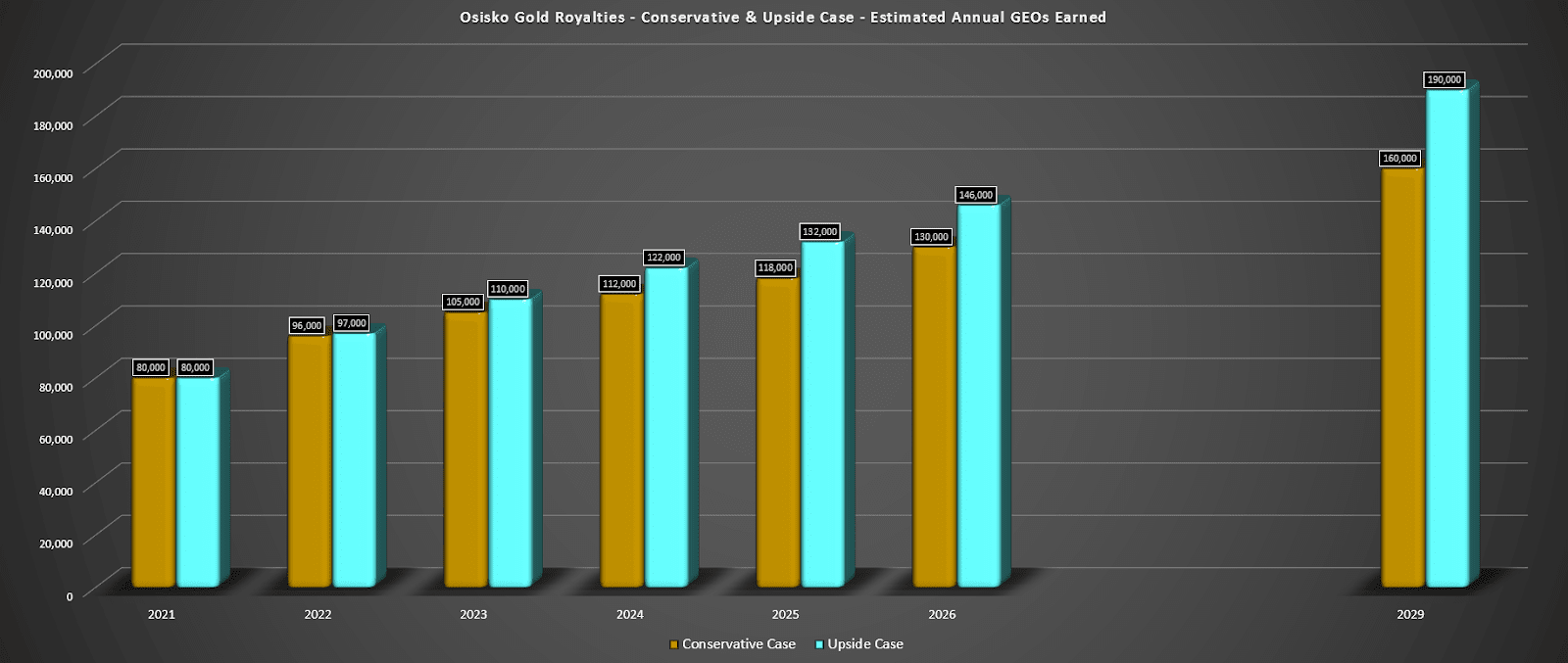

Given that there are more than ten royalty/streaming companies to choose from, it can be difficult for some investors to decide which ones are worth owning. In my view, Osisko Gold Royalties differentiates itself from nearly all of its peers, given that it has the potential to grow its attributable production from ~80,000 gold-equivalent ounces [GEOs] in FY2021 to more than 140,000 GEOs in FY2026. This represents a more than 70% growth rate, while the sector average is closer to 25%.

(Source: Company Filings, Author’s Chart & Estimates)

It’s important to note as well that Osisko Gold Royalties focuses on purchasing royalties/streams that are on assets in the best jurisdictions (Canada, Australia, United States), making it much less risky than its peers. It also has spread out its expected growth over more than ten assets, meaning that if there are delays at one or two assets, the company will still be able to deliver on its growth plans. Despite this very attractive business model and industry-leading growth profile, the stock trades at barely 1.0x P/NAV, which is a more than 50% discount to its peer group. Based on my view that it should trade at a fair multiple of 1.4x P/NAV, I see a fair value for the stock closer to US$18.00, and I see this pullback as a buying opportunity.

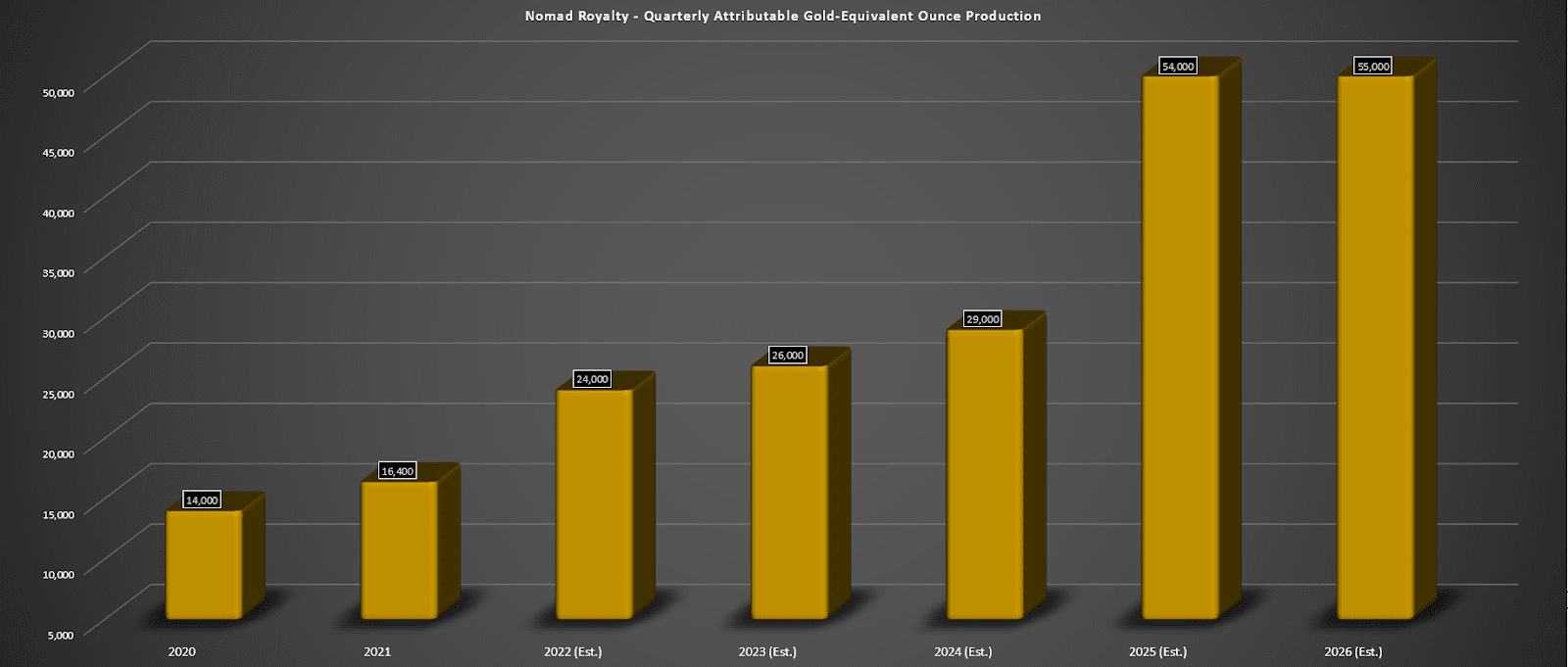

The second name worth keeping a close eye on is Nomad Royalty, which has a very similar model to Osisko Gold Royalties but is less mature, with just seven producing assets. Based on FY2022 guidance, the company expects to earn 24,000 gold-equivalent ounces [GEOs], translating to more than 40% growth year-over-year. Assuming an average gold price of $1,820/oz, this will translate to revenue of more than $43MM.

Based on Nomad Royalty’s current market cap of $480MM, this may seem like a steep valuation. However, it’s important to note that FY2022 is just inning #1 of the company’s growth story, and companies with 80% plus margins command premium multiples. This is because Nomad expects to grow annual attributable GEO production to more than 50,000 GEOs in FY2025, giving the company a compound annual attributable production growth rate of 30%. This dwarfs the peer average compound annual production growth rate of less than 5%.

Similar to Osisko Gold Royalties, this growth will come from multiple different assets, with these including the Greenstone Gold Mine in Canada, the Robertson Mine in Nevada, the Platreef Mine in South Africa, and the Blackwater Project in Canada. Assuming the company can deliver on its goals, it should see revenue grow to more than $100MM in FY2025, leaving Nomad trading at less than 5x sales. Several of the company’s peers currently trade at more than 10x sales, suggesting more than 100% upside for Nomad from current levels over the next few years.

(Source: Company Filings, Author’s Chart & Estimates)

The other attractive part about Nomad is that its management is regularly buying back shares in the open market, and the company has one of the most attractive dividend yields sector-wide at 2.2%. Based on the growth in cash flow expected over the next several years, I would expect the annualized dividend to grow to US$0.30 by 2025, which would translate to a nearly 4% yield on cost for investors entering the stock at current levels. So, given the steady insider buying, industry-leading growth profile, and attractive dividend yield, I see Nomad as a must-own name in the precious metals space.

The final name worthy of one’s consideration is Alamos Gold, a mid-tier gold producer that operates three mines in Canada and Mexico. Unfortunately, the company had a tough year in FY2021, with lower production than expected at its Mulatos Mine in Mexico. However, while some investors may have exited the stock after its poor performance in 2021, I believe this is a mistake. This is because the company continues to have exploration success at its Island Gold Mine and has a growth profile most producers would salivate over.

(Source: Company Filings, Author’s Chart)

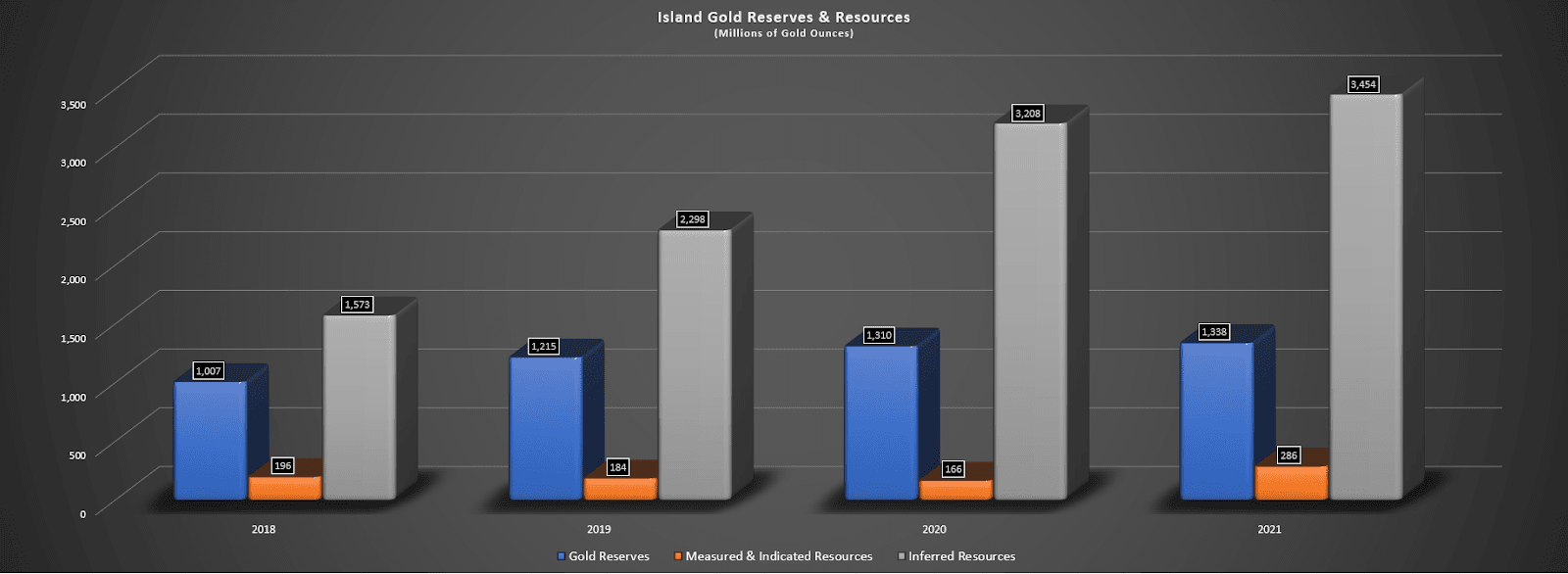

Looking at the reserves above, we can see that the company continues to grow resources and reserves despite mining depletion, and its total resource base at its high-grade Island Mine is now sitting at ~3.74MM ounces. This is in addition to another ~1.34MM ounces of higher-confidence reserves, translating to a total resource base of ~5.1MM ounces. The steady resource growth is great news for the company and certainly provides support for its planned Phase 3 Expansion to grow to more than 230,000 ounces of production per annum.

As it stands, the Island Gold Mine is one of the top-10 highest-grade gold mines globally, and given the continued exploration success, I see the possibility of the resource base growing to more than 6MM ounces and 2.0 million ounces of reserves by 2025. This would give Island one of the longest mine lives globally among high-grade underground mines, and it gives investors strong visibility into free cash flow generation looking out to 2035 based on reserves alone from this asset.

(Source: Company Filings, Author’s Chart)

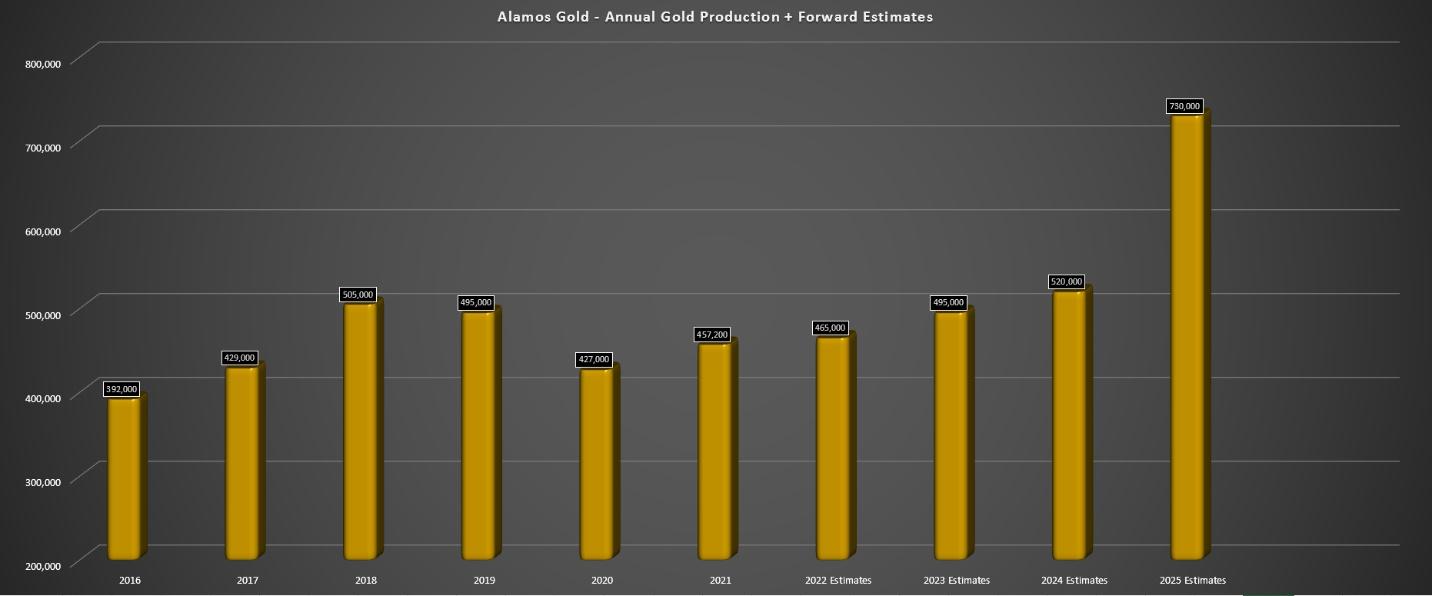

At the same time, the company is looking to advance its Lynn Lake Project in Manitoba, with a goal of producing up ~170,000 ounces per annum from this asset in 2025 through 2030 and 140,000 ounces thereafter. Combined with the ~100,000-ounce per annum increase in production at Island Gold, Alamos could see production grow to 730,000 to 750,000 ounces in FY2025. Most importantly, its costs at Island are expected to plummet from ~$800/oz to less than $600/oz, making this one of the highest-margin assets globally.

To summarize, not only does Alamos have 50% production growth in the tank, but it will also see a more than 20% decline in costs and an improved jurisdictional profile with 80% of production coming from Canada. Given this very favorable outlook, I see Alamos as a top-5 gold producer and a must-own name for investors looking to own producers in the gold sector.

A pullback would not be surprising with the GDX up sharply year-to-date, but I believe it should present a buying opportunity. I would argue that Nomad Royalty, Osisko Gold Royalties, and Alamos Gold are three of the best names to keep near the top of one’s shopping list for any pullbacks, given their industry-leading growth and strong management teams. To summarize, I remain long all three names currently, and I would strongly consider adding to my positions on any weakness.

Disclosure: I am long GLD, OR, AGI, NSR

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one’s portfolio.

Want More Great Investing Ideas?

AGI shares were unchanged in after-hours trading Thursday. Year-to-date, AGI has gained 9.04%, versus a -4.86% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| AGI | Get Rating | Get Rating | Get Rating |

| GDX | Get Rating | Get Rating | Get Rating |

| GLD | Get Rating | Get Rating | Get Rating |

| OR | Get Rating | Get Rating | Get Rating |

| NSR | Get Rating | Get Rating | Get Rating |