It’s been a volatile start to the year for the Nasdaq Composite (COMPQ), given that the index started the year up by more than 10% before briefly falling into negative territory for the year in early March. This volatility has taken an outsized toll on growth stocks and many software names, with multiple Nasdaq constituents staring down (-) 20% returns as we begin Q2. Fortunately, this pullback has allowed valuations to improve for some tech names, which looks to be creating a buying opportunity for hyper-growth names with strong business models. In this update, we’ll look at two stocks with a significant lead in their respective industries that are now trading at more reasonable valuations.

(Source: TC2000.com)

Amazon.com (AMZN) and Bill.com (BILL) have very little in common, with one being a mature online retailer & tech company and the other being a large-cap tech company in the software space. However, both companies do share two key traits: exceptional growth & improving earnings trends. In AMZN’s case, the company just came off a massive year with annual EPS growth of 81%, and in Bill.com’s case, the stock is not yet profitable but had a huge year with revenue growing by 45% despite a challenging year for small businesses due to COVID-19. In fact, both companies flourished in FY2020 while many other names were losing market share, and each company’s ability to adapt and maintain their lead on market share suggests that they have significant growth ahead in the coming years, and their respective growth stories are nowhere near over yet. Let’s take a closer look below:

(Source: Company Presentation)

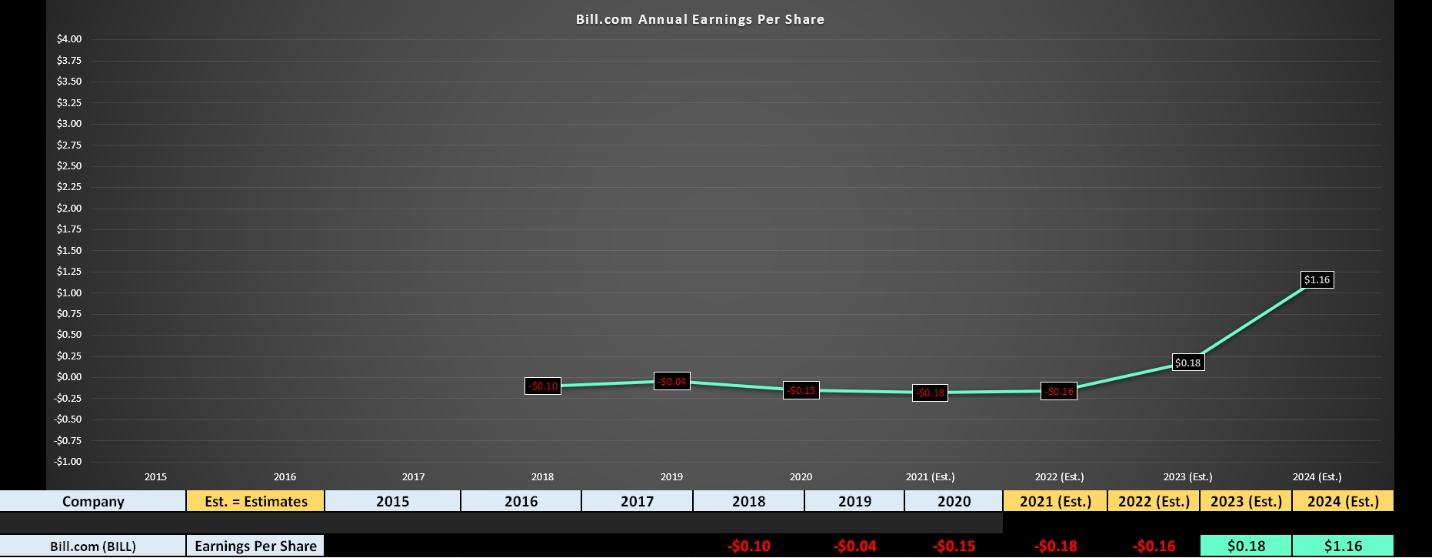

Beginning with Bill.com, the company had an impressive FY2020 with annual revenue growing to $158 million, and the company just coming off a quarter where it reported revenue of $54MM, up 38% year-over-year. This has placed the company in a position to generate revenue of more than $220MM in FY2021, translating to roughly 40% growth year-over-year after lapping a year of 45% growth. While this is a minor deceleration, it’s incredible when we consider that the company is maintaining its strong double-digit growth rates as it matures. So, while Bill.com might look expensive at nearly 40x trailing sales at a market cap above $12BB, it’s important to note that the growth story here is massive, as highlighted by Bill.com. In fact, the company’s ~109,000 customers represent only a fraction of what the company believes its TAM is.

(Source: YCharts.com, Author’s Chart)

This is because Bill.com has not even begun to scratch the surface internationally, has seen only minimal adoption among its existing customers, and estimates that there are 6BB small business employers in the US alone, with projected average revenue per user [ARPU] of $1,500 per year. Assuming the company even picked up a fraction of this market or 1MM customers, we could see Bill.com’s revenue soar to more than $1.5BB, or five times FY2022 estimates of $290MM. This doesn’t account for any international growth, with the global opportunity estimated at well over $30BB.

(Source: TC2000.com)

Even if we assume a revenue multiple of just 20, given that Bill.com would be much more mature by the time it reaches these goals domestically ($1.5BB in revenue), this would translate to a fair value for Bill.com of $30BB, or nearly triple the company’s current market cap. Obviously, a lot has to go right to achieve this growth. Still, with industry-leading customer satisfaction with a 121% net dollar retention rate and a huge tailwind with businesses constantly looking to find ways to save money & time, these projections aren’t unreasonable. As it stands currently, Bill.com is expected to post net losses per share in FY2021 and FY2022 before moving to positive annual EPS in FY2023, which is often a catalyst for new funds to enter the stock with earnings finally on the table. Technically, the stock has clear support near $132.00, and any dips below this level look like they would provide low-risk buying opportunities.

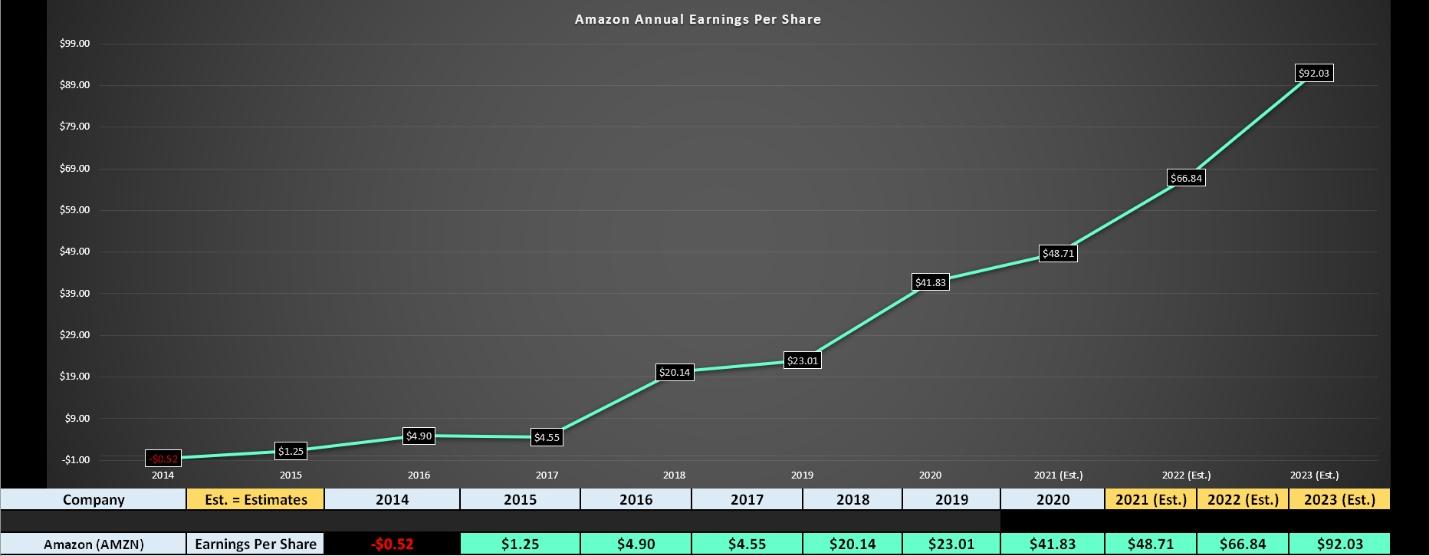

Moving over to Amazon, the stock needs no introduction and just came off an incredible year, as noted earlier. In Amazon’s case, the company managed to dominate given that many consumers were not interested in entering stores to do their shopping, and the company enjoyed 44% revenue growth in Q4 and more than 35% growth in FY2020. This exceptional growth combined with strong gross margins of nearly 40% translated to a significant boost in annual EPS, with FY2020 annual EPS coming at $41.83.

For investors not in the stock looking in, it’s understandable to think AMZN is expensive at current levels, trading at more than 75x trailing earnings. However, with FY2023 estimates sitting at above $90.00 per share, FY2020 and FY2021 annual EPS figures are already stale. Even if we assume a more contracted earnings multiple of 65 for Amazon vs. where it’s previously traded consistently above 80, this would translate to a fair value of $5,982 based on FY2023 estimates of $92.03. In addition, as the company matures, we could see AMZN begin to pay a small dividend, which would make it an intriguing dividend growth story as well.

(Source: YCharts.com, Author’s Chart)

AMZN has clearly had a massive run over the past decade, and it’s easy to assume that there’s no upside left. However, on closer inspection of the monthly chart, I would argue that this isn’t the case at all. As we can see, AMZN has typically gone on multi-year bull runs after breaking out of massive bases, and we are just 13 months into this recent breakout and up less than 100% from the breakout level at $1,800. If this were to play out like the previous breakout, Amazon would enjoy a 4-year run with a return of nearly 400% ($1,800 vs. $400).

However, with the stock more mature, expectations have to be reeled in. Having said that, even if we saw two-thirds of the return over a similar multi-year run (266%), this would translate to AMZN heading to $5,850 per share, in line with fair value for FY2023 EPS estimates. Therefore, I would not rule out another double in AMZN, and I would view any pullbacks below $3,000 as an opportunity to add to positions.

(Source: TC2000.com)

While the overall market remains expensive, AMZN and BILL are solid stories with lots of growth left in their tank, trading at reasonable valuations given their potential. So, if we do see weakness in Q2 in either name and AMZN dips below $3,000 or Bill.com below $132.00, I would view these corrections as low-risk buying opportunities. For now, I remain long AMZN from $1,600 per share and may look to add to my position in the coming weeks.

Disclosure: I am long AMZN

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

AMZN shares were trading at $3,316.39 per share on Thursday afternoon, up $37.00 (+1.13%). Year-to-date, AMZN has gained 1.83%, versus a 9.53% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| AMZN | Get Rating | Get Rating | Get Rating |

| BILL | Get Rating | Get Rating | Get Rating |