It’s been an incredible year thus far for tech & growth stocks, and this impressive performance since the March lows has helped to push the Nasdaq-100 (QQQ) to one of its best years on record, with a 44% return year-to-date. Unfortunately, this massive rally has left a good chunk of the index’s constituents quite expensive as investors continue to hunt down anything with value left in the index to bolster their Q4 returns. The other issue is that investor sentiment is now sitting at its most dangerous levels since January 2018, with complacency hitting a new 2-year high this week.

Obviously, this doesn’t mean that the market has to fall apart in the next few weeks, but it does suggest that a Santa Rally might end up running into selling pressure. The good news is that there are still a couple of names in the index that rank well for growth and are trading at reasonable valuations. Let’s take a closer look at them below:

(Source: TC2000.com)

The companies we’ll discuss today are Facebook (FB) and DocuSign (DOCU): two companies that have little in common fundamentally, other than the fact that they’re both QQQ constituents. The former company is a social media giant and the proud owner of arguably the most addictive App in the world: Instagram.

The latter is a disruptive tech company that’s gained considerable traction since the global pandemic hit as fewer companies are meeting face to face. This is because DocuSign’s E-Signature offering allows businesses to go on as usual without physical signatures. Other than Zoom Video (ZM), this is one of the most essential products to businesses, so it’s no surprise that the stock has more than doubled this year.

While the two companies don’t share much fundamentally, they do have one common trait: strong earnings trends. While Facebook’s growth pales compared to DocuSign, the company is on track to post a new high in annual EPS this year, and earnings growth is expected to continue to increase by more than 10% per year out to FY2023. Let’s take a closer look below:

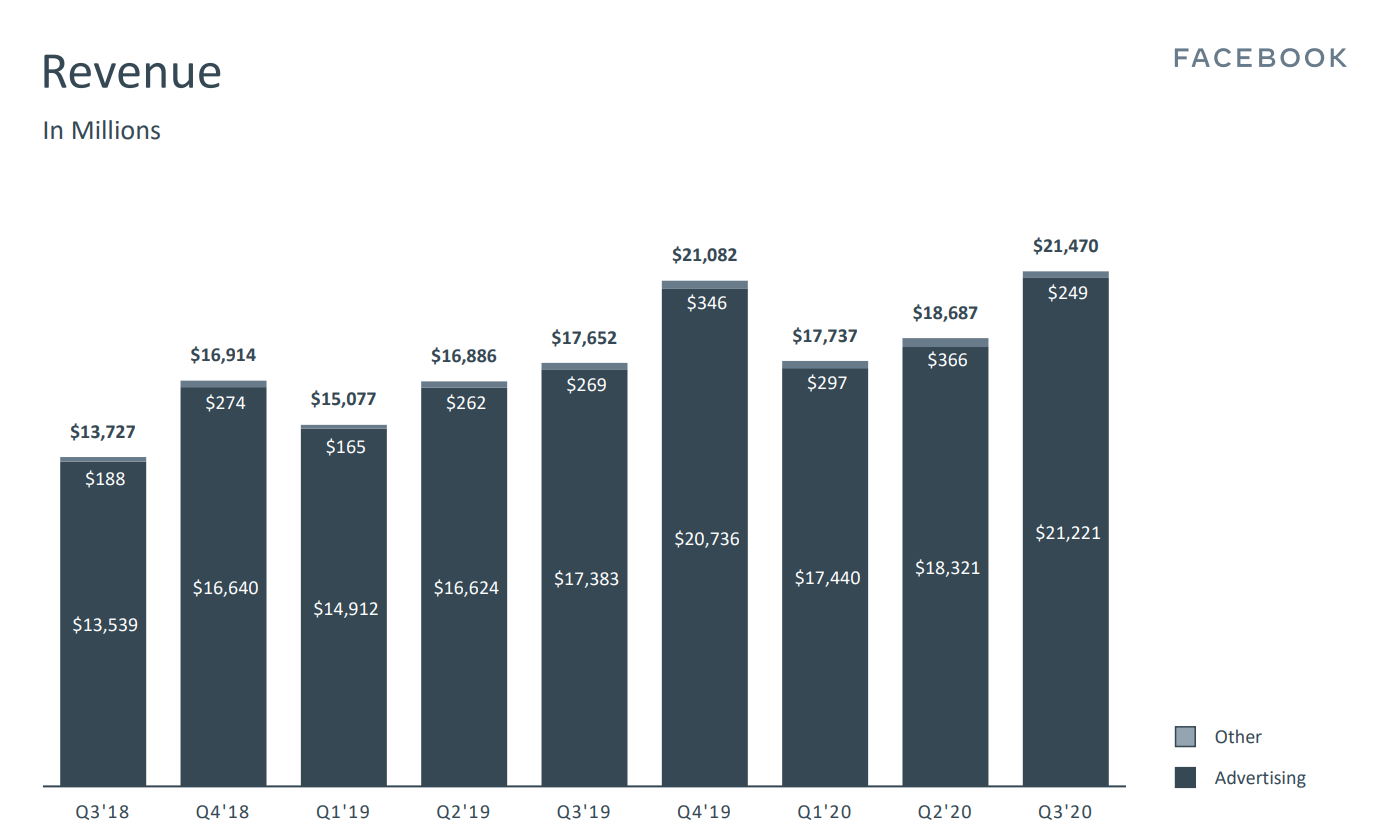

(Source: Facebook Corporate Presentation)

Facebook just came off a strong quarter in Q3 with record revenue of $21.47 billion, and diluted EPS hit a new high of $2.71 as well. Despite critics suggesting that FB’s best days are over as people continue to migrate away from its platforms, this couldn’t be further from the truth, with monthly active users up to 2.74 billion, up 12% year-over-year.

Meanwhile, the company’s average revenue per user [ARPU] came in just shy of all-time highs of $8.52, with an ARPU of $7.89 in Q3. This translated to 9% growth year-over-year, with the biggest gains coming from APAC where Q3 ARPU hit a new high.

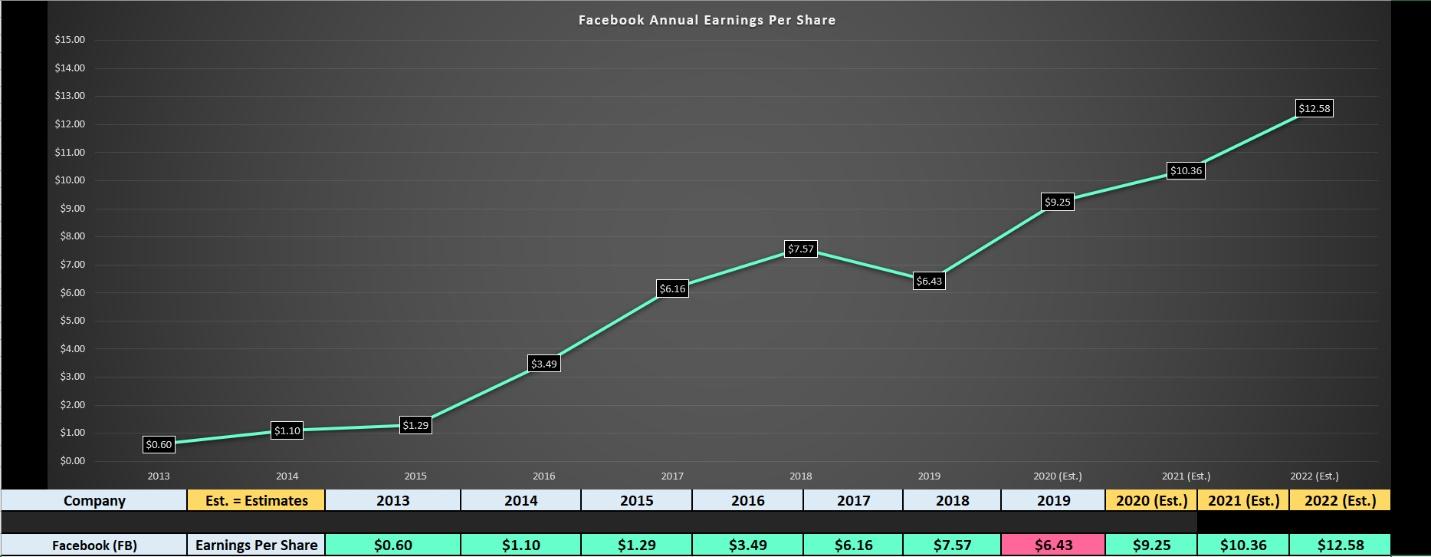

(Source: YCharts.com, Author’s Chart)

As shown above, these improving metrics have set FB up for another year of record annual EPS, with FY2020 annual EPS estimates sitting at $9.25 currently. While this 44% growth rate in annual EPS ($9.25 vs. $6.43) should be discounted as FY2019 was a down year for earnings, it’s encouraging to see annual EPS immediately returning to new highs. Meanwhile, annual EPS is expected to hit $12.58 in FY2022, continuing its trend of double-digit earnings growth that Facebook has enjoyed for nearly a decade now.

Some investors might argue that FB is expensive at $280.00 per share with earnings of just $6.43 last year, but these are stale numbers, and the market is looking forward to the FY2022 numbers now that we’re about to enter 2021. Based on the FY2022 annual EPS estimates, FB is actually trading at a very reasonable 22x earnings given that it’s a liquid market leader with consistent annual EPS growth. Therefore, if we were to see the stock pullback below $265.00, where it would trade at roughly 21x FY2022 earnings, I would view this as a low-risk buying opportunity.

(Source: DocuSign Earnings Slides)

Moving over to DocuSign, the company also came off a huge quarter, with billings up 61% year-over-year to $406 million, and revenue soaring by 45% to $342 million. This translated to the strongest quarter for the company’s sales growth in over two years, and the company is getting set to report its fiscal Q3 2021 earnings this week.

While many critics believe that the growth story is over with vaccines getting ready to roll out, I would argue this isn’t the case at all. This is because DocuSign saves businesses both time and money by avoiding travel and appointments, and there’s no reason that this is going to change just because people can meet face-to-face again. Meanwhile, the 55% growth in enterprise & commercial customers is not likely to suddenly erode just because of promises of a vaccine. Enterprises tend to make decisions with years of planning in mind, not weeks, and DOCU is firmly positioned as the leader in the E-Signature space.

(Source: YCharts.com, Author’s Chart)

As shown in the DOCU’s earnings trend, the company has had explosive growth, with FY2020 annual EPS up over 200% and FY2021 annual EPS expected to grow by 85% ($0.58 vs. $0.31). These are incredible metrics given that the company is lapping a year of triple-digit growth. If the company can meet FY2023 forecasts of $1.72, it will boast one of the highest compound annual earnings growth rates in the market of over 109% ($1.72 vs. $0.09).

While some investors might be writing the company off as it looks extremely expensive at over 700x FY2020 annual EPS, it’s important to note that the market is already looking ahead to FY2023 given that DOCU is getting ready to report its fiscal Q3 2021 earnings this week.

Based on annual EPS of $1.72, the stock is trading at only 130x earnings, which is actually quite reasonable for companies with a compound annual growth rate of over 100%. However, to bake in a margin of safety, I see the low-risk buying opportunity for the stock on any dips below $205.00.

This is where the stock should find support near its 200-day moving average and the bottom of its current base. As we can see in the chart below, DOCU broke out of a massive base last year, ran up over 200%, and is now building its first real base since its blow-off top in Q3. The best-case scenario would be another couple of months building a base here, and then a breakout in Q1 of next year as the stock would have digested its recent parabolic advance

(Source: TC2000.com)

While it’s tough to find much value out there in the market currently, DOCU and FB are two names that should be at the top of one’s shopping list if we do see a correction. This is because both names are leaders in their respective industry groups and have a significant lead on their competitors, making it likely that they’ll remain the leaders for years to come. Currently, I don’t see a low-risk buying opportunity for either stock.

Still, any dips below $265 on FB and $205 on DOCU would translate to attractive valuations and solid entries for either name. Therefore, for investors looking for names to put on their shopping list if we do see a correction in the coming weeks, I believe these two names are worthy of keeping a close eye on.

Disclosure: I am long FB

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

FB shares were trading at $283.01 per share on Thursday afternoon, down $4.51 (-1.57%). Year-to-date, FB has gained 37.89%, versus a 15.71% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| FB | Get Rating | Get Rating | Get Rating |

| DOCU | Get Rating | Get Rating | Get Rating |

| QQQ | Get Rating | Get Rating | Get Rating |