It’s been a tough start to the month for the Gold Miners Index (GDX) as we’ve seen a sharp pullback in most gold names despite a relatively shallow pullback in the price of gold (GLD). However, while this pullback has been occurring, analysts have been busy ratcheting their earnings estimates higher for FY-2021, suggesting this could be a good opportunity to begin nibbling on miners before most realize that $1,550/oz gold prices are the new normal. Given that we’ve seen pullbacks in many miners at the same time as upward earnings revisions, we see quite a bit of value show up in the sector yet again, and three clear names stand out head and shoulders above the rest for earnings quality and margins. Assuming this correction in the miners continues, this is likely a low-risk area to begin adding exposure to these names.

(Source: Kirkland Lake Gold Company Presentation)

While Franco Nevada Gold (FNV), Wheaton Precious Metals (WPM), and Kirkland Lake Gold (KL) may not appear to have much in common at first glance, they do share one definite similarity. This similarity is that all of them have industry-leading margins, and it’s typically the highest-margin names that outperform their peers, even in a rising gold price environment. The fallacious argument going around is that investors should buy the low-margin producers as they’ll benefit the most from the higher gold price, and while this sounds good in practice, it’s total nonsense in most cases. This is because the higher-cost producers that have been unable to get their costs below $1,200/oz for years are poorly run in most cases. Meanwhile, the companies enjoying 50% margins at sub- $1,200/oz gold are incredibly well run, able to pump out cash-flow in gold bull or bear markets. This is why FNV, WPM, and KL have massively outperformed their peers the past several years, and will likely continue to do so, regardless of the gold price.

(Source: YCharts.com, Author’s Chart)

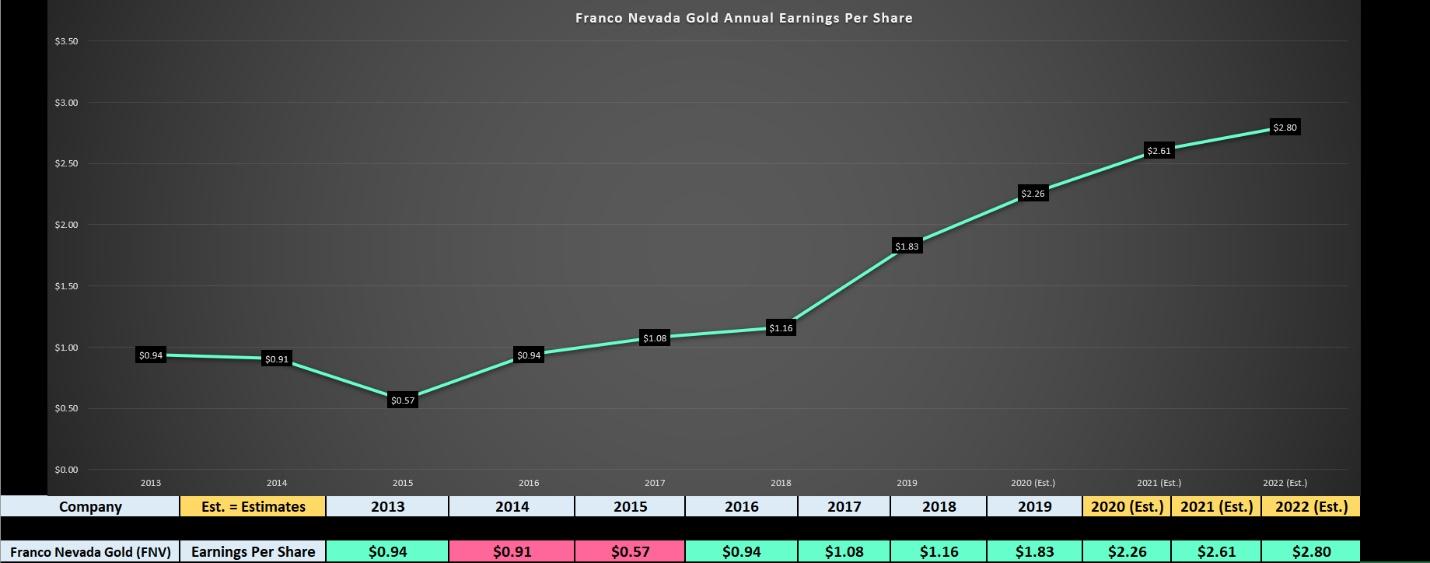

Beginning with Franco Nevada Gold, the company is a staple for any precious metals portfolio with 80% plus margins, a massively diversified royalty portfolio, and one of the best earnings trends in the sector. As the chart above shows, the company has managed to grow its annual EPS from $0.94 in FY-2016 to $1.83 last year, achieving a nearly 100% growth rate in earnings with only a 25% rise in the price of gold. If we look ahead to FY-2020 earnings estimates, this growth is expected to continue at a brisk pace, with estimates currently sitting at $2.26. This would translate to a 24% growth rate year-over-year, a level of growth that only the best growth companies in the market are able to achieve consistently. Most importantly, these earnings estimates are trending higher, and this growth is occurring despite the company lapping a year of 57% growth last year. On a two-year stacked basis, this is over 80% growth, which remains one of the most robust earnings growth profiles in the sector.

(Source: TC2000.com)

If we take a look at the chart above, we can see that Franco Nevada Gold was one of the first names to vault to new highs following the mid-March correction, up nine weeks in a row, which shows significant accumulation by funds. Since that time, the stock has pulled back for a few weeks now but is resting just a couple of percent above its key weekly moving average. For investors looking to begin to add exposure to the name, a test of this moving average would be the ideal spot to do so. Currently, this moving average sits at the $123.00 level and would be what I would consider a relatively low-risk buying opportunity.

(Source: Kirkland Lake Gold Company Presentation)

Moving over to Kirkland Lake Gold, we’ve got the previous leader in the sector, but the name remains well off its highs following the acquisition of one of the largest mines in Canada last year, Detour Lake. This deal is likely to lead to margin compression and was also an earnings headwind given the higher share count following the merger. However, Kirkland Lake Gold has been snapping up shares on the open market to bring its share count back to closer to pre-acquisition levels. Thus far, the company has repurchased over 3% of its float, with plans to buy back up to 10% in the next 12 months. Generally, I’m not particularly eager to buy turnaround stories with compressed margins, but it’s important to note that the company had industry-leading margins before the drop in margins due to the Detour Lake acquisition. Therefore, Kirkland Lake will still have industry-leading margins of over 50% after the merger. Besides, the higher gold price has more than offset any margin headwind with the price of gold hovering above $1,600/oz.

(Source: YCharts.com, Author’s Chart)

As we can see from the above chart of annual earnings per share, the company managed to grow annual EPS by over 100% in FY-2019 but is now set for a significant deceleration in earnings growth in FY-2020. However, following a two-year stacked growth rate of 180%, this is entirely normal. Currently, FY-2020 earnings estimates are sitting at $2.99, projecting 11% growth year-over-year, and earnings are forecasted to continue their strong trajectory in FY-2021 with estimates sitting at $3.72, reflecting over 20% growth year-over-year. While this 11% growth rate for FY-2020 is below that of the sector for FY-2020, which currently sits closer to 24%, the most attractive thing about Kirkland Lake is that the valuation crept down to the lowest levels in years for the stock. After factoring in $2.50 per share in cash, the company is trading for less than 12x forward earnings, while the remainder of Tier-1 producers are trading closer to 20x forward earnings. Therefore, there is significant potential for margin expansion here, and my price target for the stock remains at $53.00. It’s quite rare that investors get the opportunity to buy the industry-leading with 60% plus margins at fire-sale prices, but the stock is finally trading at an exceptional valuation after years selling at a premium to its peers.

(Source: TC2000.com)

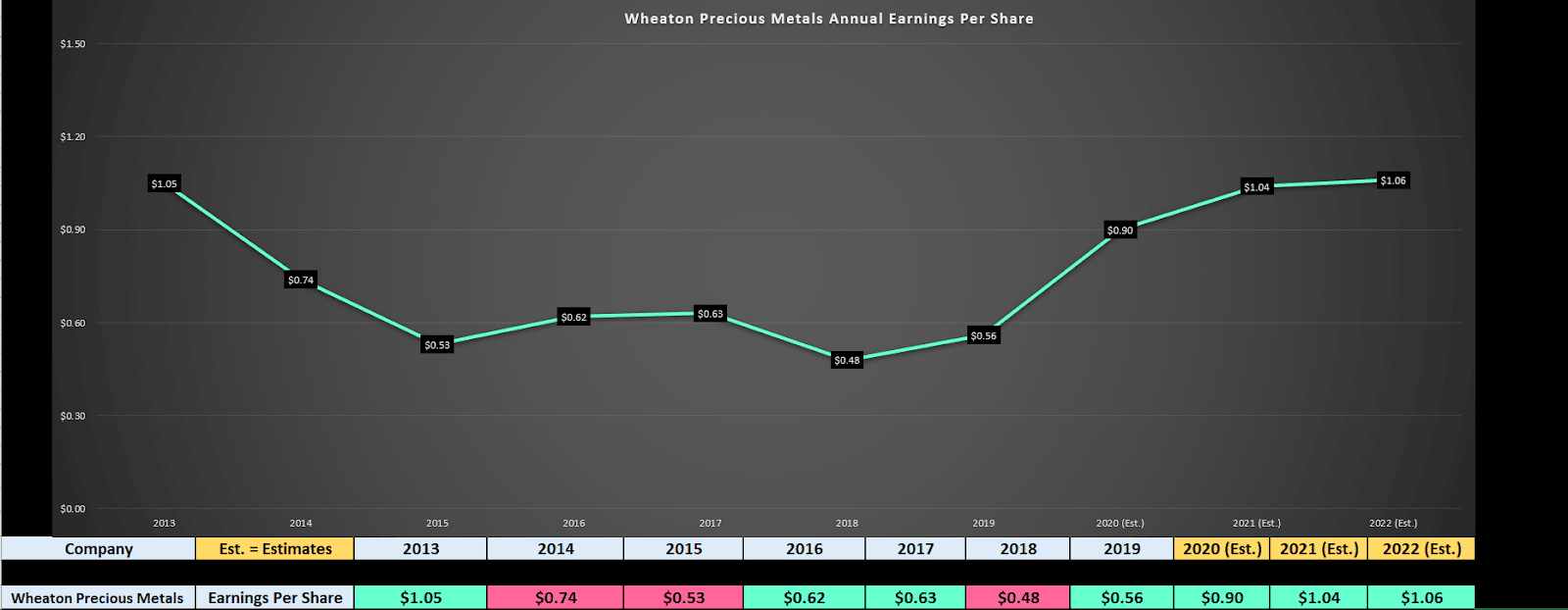

Last but not least, we have Wheaton Precious Metals, another royalty play in the precious metals sector. As the chart below shows of annual EPS, the company saw minimal earnings growth over the past several years but is finally expected to see an earnings breakout in FY-2020. Typically, earnings breakouts are very bullish, and especially when they’re coupled with a breakout in price. This is what we see with Wheaton as earnings estimates continue to climb higher, with FY-2020 annual EPS sitting at $0.90. This would translate to a 60% growth in earnings year-over-year and is one of the highest growth rates among the royalty names currently. Therefore, while the stock may look expensive at over 60x FY-2019 earnings, it only looks pricey as investors are not factoring in the massive growth this year.

(Source: YCharts.com, Author’s Chart)

(Source: TC2000.com)

Similar to FNV, Wheaton Precious Metals is pulling back to its key weekly moving average, and any test of this moving average near $35.50 would likely provide a low-risk opportunity to add some exposure. Based on the fact that WPM is trading for just 45x FY-2020 earnings despite an industry-leading growth rate, the stock is finally beginning to get attractive again, assuming this pullback continues.

The massive rally in the precious metals sector has left many names over-extended, and many laggard names expensive. Fortunately, this relentless bid under the laggards has allowed a few reliable sector leaders to head towards attractive levels with money drifting to lower-quality and lower-cap stocks. Given the exceptional earnings quality of FNV, WPM, and KL, and their industry-leading margins, I believe these three names are excellent choices for investors looking for value in the sector. Currently, I remain long Kirkland Lake Gold, but I would consider scooping up shares of WPM and FNV if they were to continue to pull back. Ultimately, I see all three names higher in the next 12 months regardless of the gold price and believe all three are staples for a precious metals portfolio.

(Disclosure: I am long KL)

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

Do NOT Buy This Dip! Are you prepared for the bear market’s return?

7 “Safe-Haven” Dividend Stocks for Turbulent Times

9 “BUY THE DIP” Growth Stocks for 2020

FNV shares were trading at $128.55 per share on Thursday afternoon, down $1.41 (-1.08%). Year-to-date, FNV has gained 24.98%, versus a -2.81% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| FNV | Get Rating | Get Rating | Get Rating |

| GLD | Get Rating | Get Rating | Get Rating |

| GDX | Get Rating | Get Rating | Get Rating |

| WPM | Get Rating | Get Rating | Get Rating |

| KL | Get Rating | Get Rating | Get Rating |