It’s been a rough year thus far for investors in the Gold Miners Index (GDX), with the ETF sliding more than 5% year-to-date, massively underperforming the S&P-500 (SPY) and Nasdaq-100 (QQQ) indexes.

However, Q4 has been much better thus far for precious metals bulls, with the bulls staging a 14% rally thus far in the GDX, reversing nearly all the losses from Q3 when the gold price slid below $1,700/oz.

While the miners are up more than 10% off their recent lows, it’s worth noting that the sector remains the cheapest that it’s been in several years, and this suggests that further weakness should present a low risk buying opportunity. In this update, we’ll look at three miners trading at deep discounts to fair value, and their ideal buy points for the best reward/risk proposition:

(Source: TC2000.com)

With inflation readings continuing to remain elevated and negative real rates deeply in negative territory, one sector that doesn’t receive nearly enough love is the Gold Miners Index.

For those unfamiliar, the ETF is full of gold producers, silver producers, and royalty/streaming companies exposed to the gold and silver price. This disgust towards the sector is especially surprising given that the GDX is trading at its 2nd cheapest level in the past decade.

However, as the market goes, most investors and traders are interested in what’s hot now, not what’s offering the best value and may come back in favor next year.

The favored way to play the gold price to hedge against inflation is the Gold Miners Index, given that it’s quite liquid and a basket of stocks that provide exposure to gold.

However, with the average gold producer paying a dividend and the performance of the GDX often bogged down by the 10-15 poorly-run companies with razor-thin margins and inferior management teams, I believe the best way to play the gold price is through individual companies.

Typically, one must pay up for the best companies, which makes playing the industry leaders a less attractive proposition, given that the best way to lose money in the sector is by overpaying for quality.

However, after a 15-month cyclical bear market in the GDX, even some of the better names are dirt-cheap, which provides investors with an opportunity. Among the GDX, three names that stick out as high-quality business models at very reasonable valuations are Alamos Gold (AGI - Get Rating), Nomad Royalty (NSR), and Barrick Gold (GOLD - Get Rating).

I believe these three are worth keeping a close eye on, given that they trade at a discount to net asset value currently. Let’s look at Barrick first:

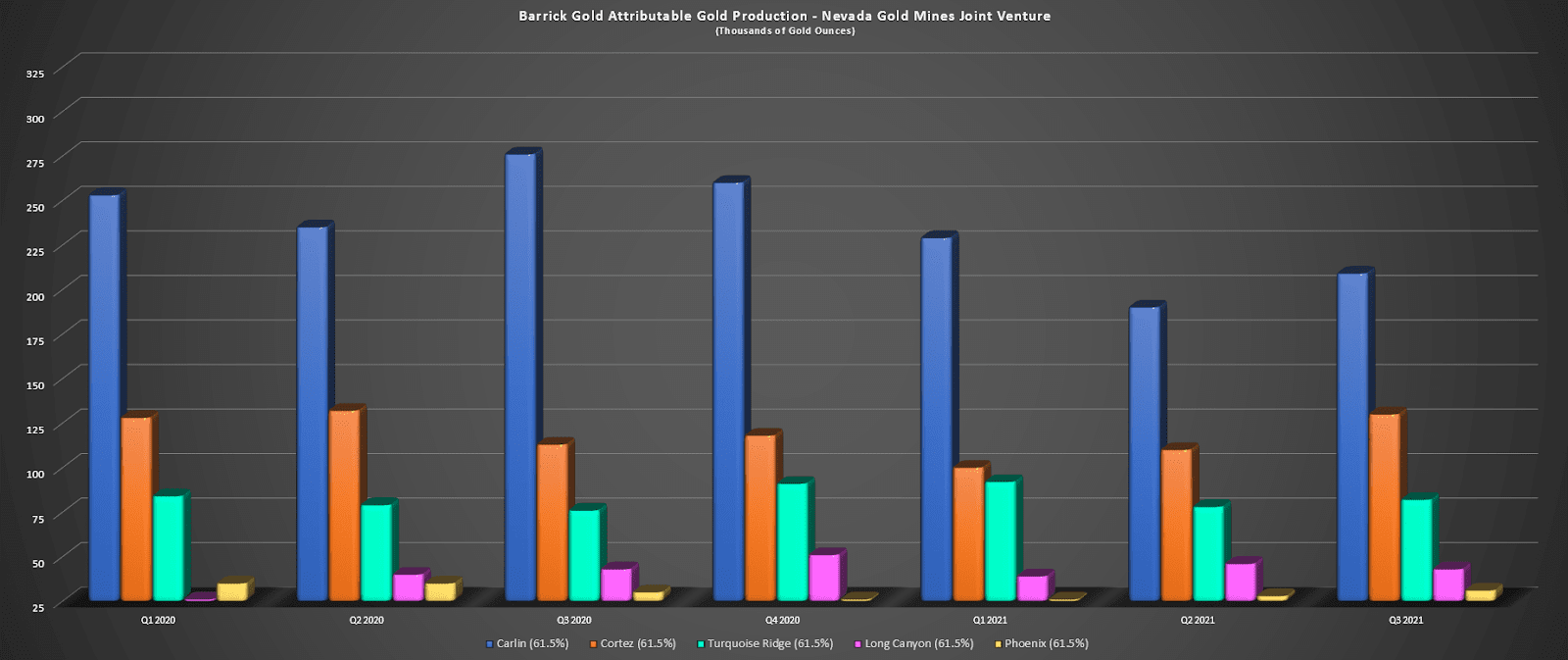

(Source: Company Filings, Author’s Chart)

As shown in the chart above, Barrick had a tough Q2 and Q3, with a mechanical mill failure at its Goldstrike Mine in Nevada weighing on production capacity.

This led to a sharp decline in production from this major production hub, which is 61.5% owned by Barrick and minority-owned by Newmont (NEM). This wasn’t helped by travel restrictions that weighed on productivity at its Hemlo Mine in Canada and much lower production from its Tongon Mine in Africa. However, repairs are complete at Goldstrike, which has Nevada up for a strong Q4.

Besides, Barrick continues to benefit from higher copper prices, which were able to offset some of the softness on the gold side of the business. So, while it’s easy to be disappointed about the weaker Q3 results, the operational weakness already looks priced into the stock:

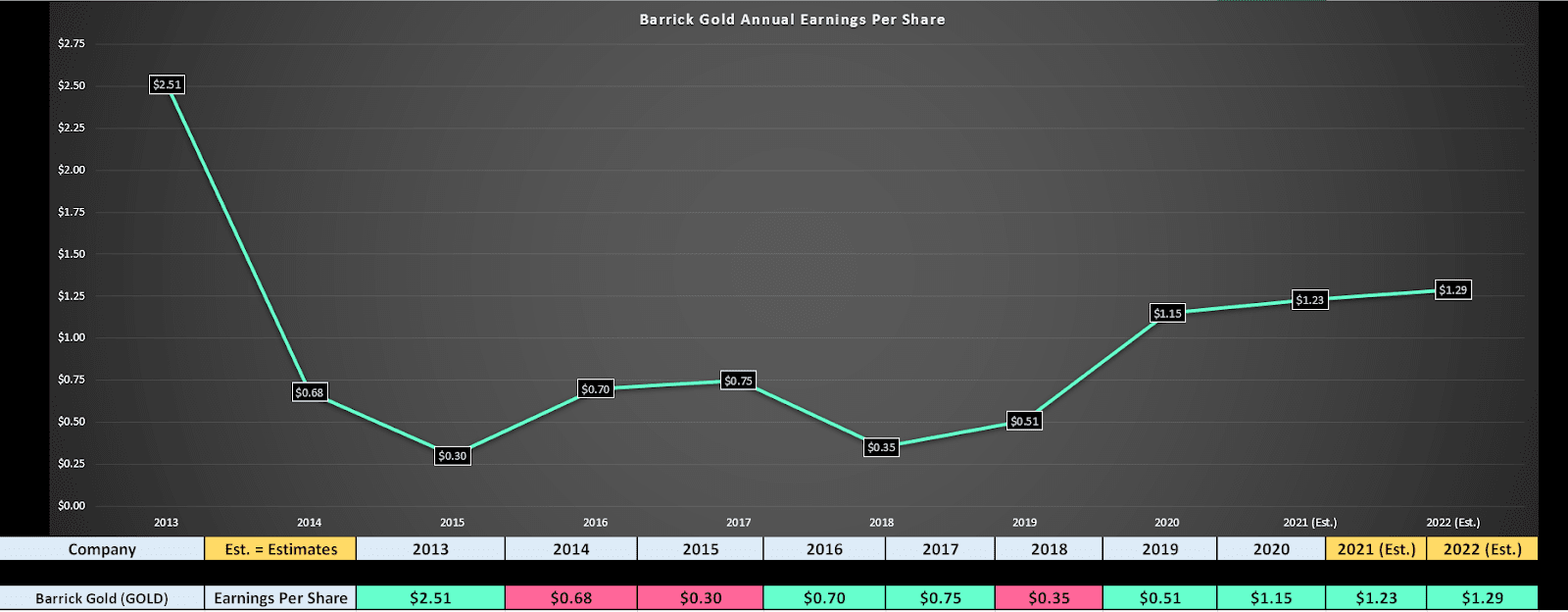

As shown below, Barrick Gold is on track to report $1.21 in annual EPS in FY2021 and $1.29 – $1.35 in annual EPS in FY2022. With the stock trading at a share price near $20.00, this leaves the stock sitting at a valuation of just 15x FY2022 earnings estimates, a significant discount to its historical earnings multiple of 18.

Meanwhile, on a price to net-asset-value [P/NAV] basis, Barrick Gold trades at roughly 0.99x P/NAV vs. a historical multiple of 1.25x P/NAV. This suggests that the stock is currently undervalued between 20% to 35%, with its fair value sitting above $26.50 per share.

(Source: YCharts.com, Author’s Chart)

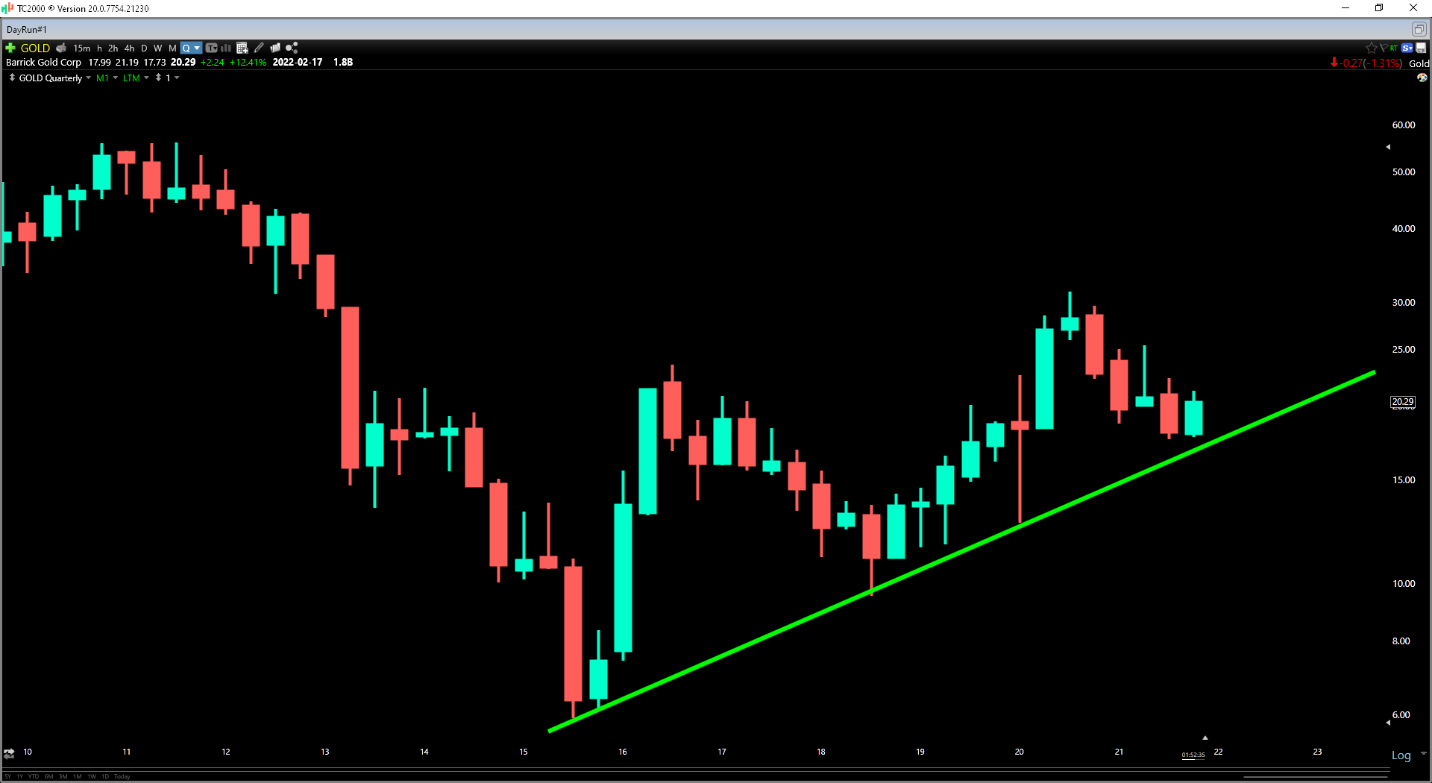

If we look at the technical chart below, Barrick is sitting just above a major support zone dating back to 2015, which is a long-term uptrend that comes in near $17.50 – $18.25.

If Barrick were to drop back to oversold levels near $18.25, this would represent a very low-risk buying opportunity, with tests of multi-year trend lines quite rare in the gold space, especially during gold bull markets.

Notably, a pullback to $18.25 would push Barrick back below 0.95x P/NAV, setting investors up for a nearly 50% upside to fair value, an even larger margin of safety, as well as a 2.0% dividend yield.

So, while I am not in a rush to buy Barrick at this moment, I continue to watch the stock closely for a re-test of the $18.25 – $18.30 level, where the stock would be a steal.

(Source: TC2000.com)

The second name worth keeping a close eye on is Nomad Royalties (NSR), a newly-listed small-cap royalty producer that’s led by a team with significant previous experience in the royalty sector.

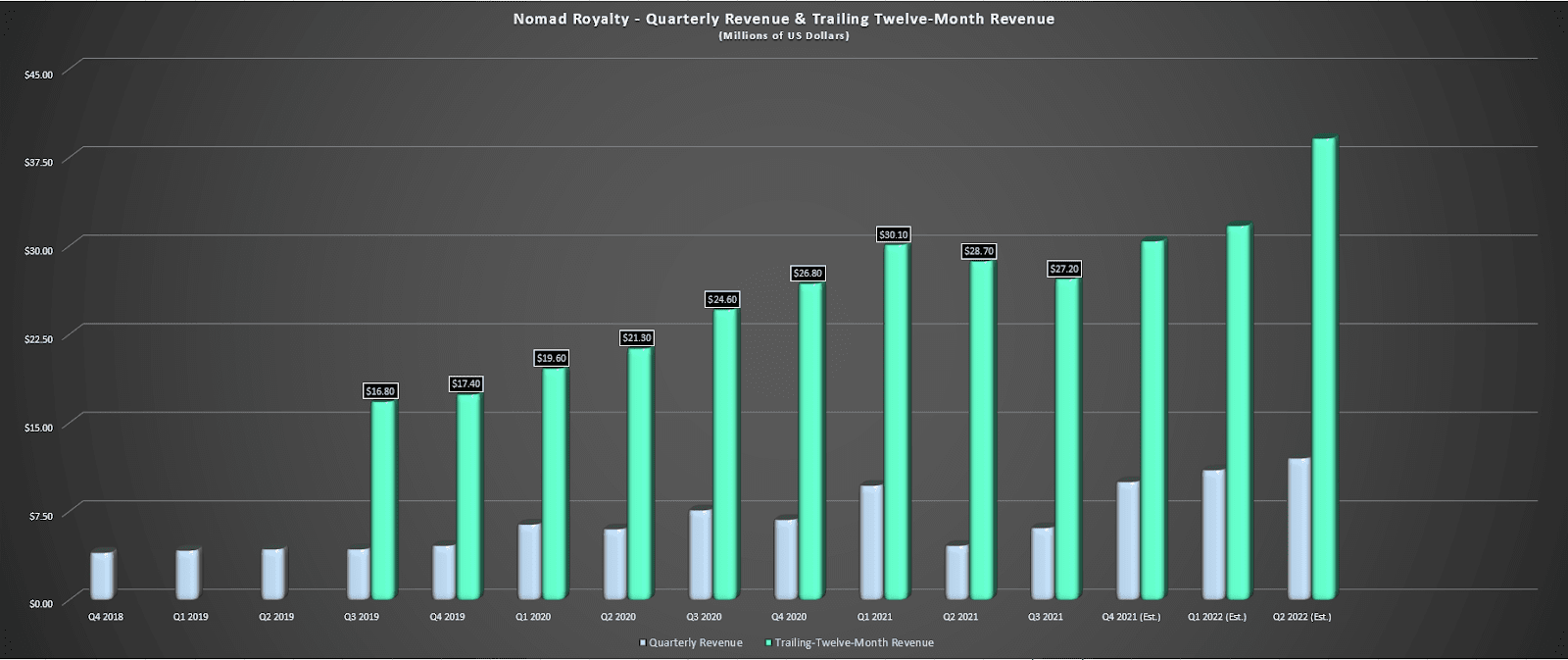

The company has had a very busy year thus far, adding a name royalty on the massive Greenstone Gold Project that’s in production, a significant royalty at the Caserones Copper Mine in Chile, and a royalty on the large Blackwater Gold Project in British Columbia. Meanwhile, the company’s largest royalty asset, the Blyvoor Mine, has continued to ramp up over the past few months after a slow start to production.

This is expected to translate to a significant increase in revenue in FY2022 for Nomad, with revenue set to hit a new all-time high in Q1 2022 and increase to more than $47MM next year.

(Source: Company Filings, Author’s Chart)

(Source: Nomad Royalty Company Presentation)

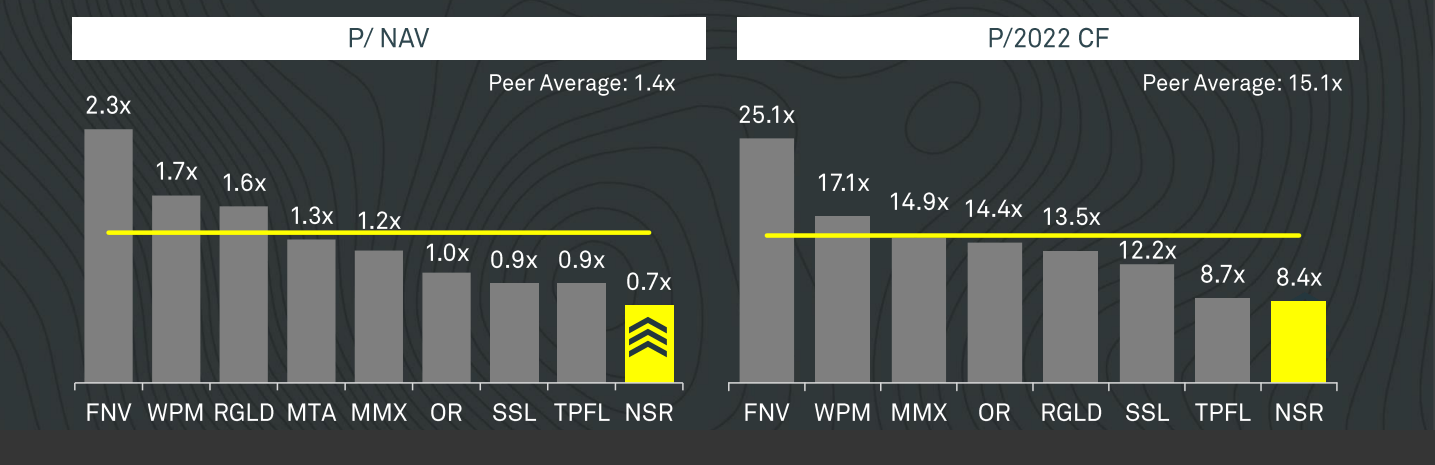

With Nomad currently trading at a market cap of $450MM, this leaves the stock sitting at less than 10x sales, which is a dirt-cheap valuation for a company with 70% plus margins. Some investors would argue that Nomad should not trade at this high a valuation or anywhere near the price to cash flow ratios of its peers, given that it’s a much smaller company.

While I would agree that NSR should not command a valuation like Franco Nevada or Wheaton Precious Metals, it could easily command a valuation of 13x sales and 1.1x P/NAV, translating to more than 30% upside from current levels from a share price of $7.60.

Besides, FY2022 revenue estimates do not include any cash flow from major royalties that are set to come online, including Greenstone, Robertson, Woodlawn, Blackwater, and a doubling of annual production at Blyvoor.

So, while NSR trades at less than 10x FY2022 sales, it appears to trade at closer to 5x FY2025 sales, assuming these assets stick to their current schedules. This points to long-term upside well above $11.00 per share, with investors collecting a 2.3% dividend yield while they wait for this growth.

In summary, I see Nomad as the most attractive play in the royalty/streaming space, and I would view any pullbacks below $7.30 as low-risk buying opportunities or opportunities to add to positions.

The final name on the list is a mid-cap producer, Alamos Gold, currently operating three mines, two in Ontario and one in Mexico.

Like Barrick, Alamos had a tough quarter in Q3, with its Mulatos Mine underperforming expectations and expected to have a few soft quarters ahead while the company completes construction at its higher-grade La Yaqui Grande Project in Mexico.

However, the company’s other two mines that make up 70% of consolidated production continue to perform quite well, and Island Gold continues to impress from an exploration standpoint. This year alone, the company has seen multiple high-grade intercepts down-plunge from the existing mineral resource base, suggesting significant upside from both a tonnage and grade standpoint at this ~140,000-ounce operation.

Even before this year’s drill results, Alamos was well aware that this was a world-class operation, and it decided to look into an expansion study to increase production at this mine.

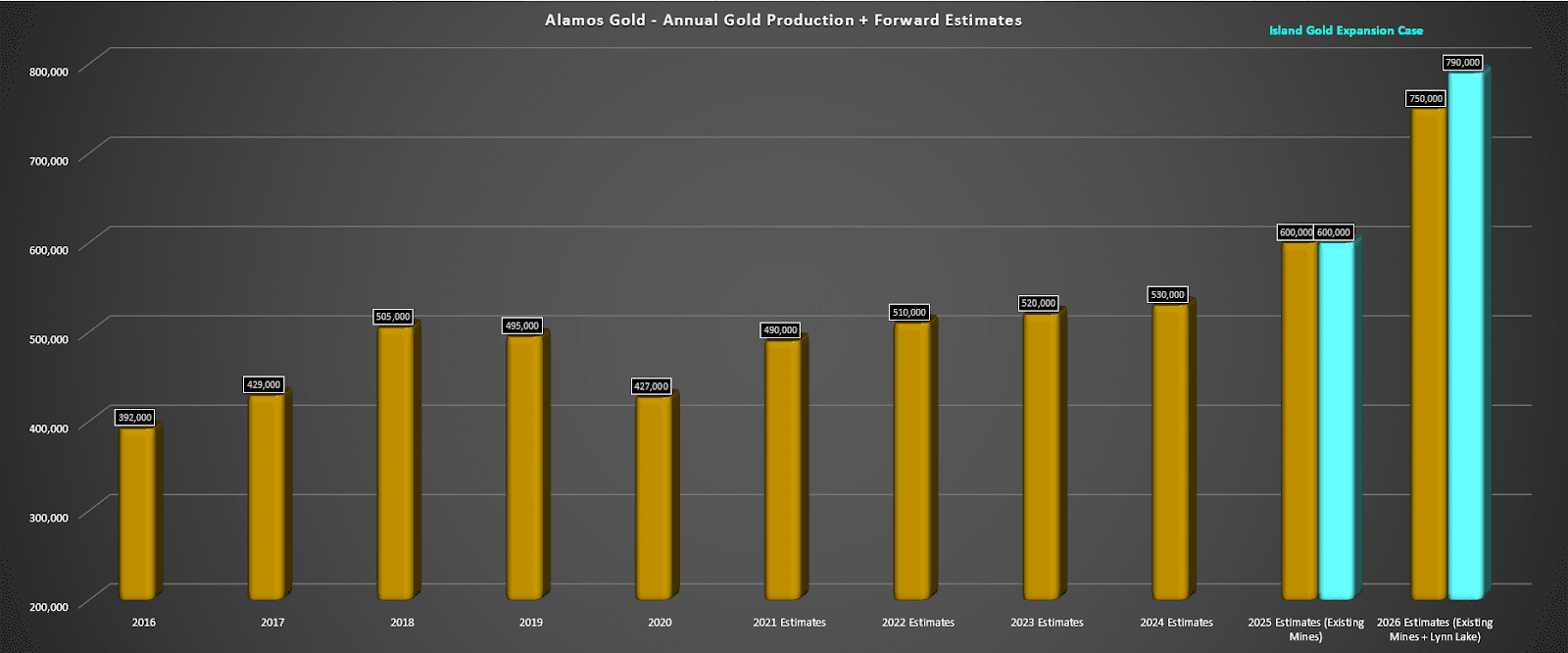

The Phase III study, which contemplates a higher throughput rate and the construction of a shaft, is expected to be completed in 2025. Once complete, annual production should increase by more than 75% to ~240,000 ounces per annum, with costs at Island Gold set to drop from $800/oz to below $625/oz.

This would make Island one of the lowest-cost gold mines globally. At the same time, the company is awaiting permits for its Lynn Lake Project in Manitoba, which is set to add another 150,000 ounces of production to its consolidated production profile. As the chart below shows, this has Alamos set up to grow production ~50% over the next four years, with a goal of becoming a 750,000-ounce producer by 2025.

(Source: Author’s Estimates, Company Filings, Author’s Chart)

In a sector where it’s hard to find stories with high double-digit organic growth, Alamos is one of a kind, yet the stock trades at less than 1.0x P/NAV and less than 10x FY2023 earnings estimates. This is a dirt-cheap valuation, and I continue to see a fair value for the stock closer to $11.00 per share.

So, with the stock down and out after a weak quarter, I would expect that any weakness going forward should present a low-risk entry point into the stock. It’s important to note that my fair value of $11.00 assumes no further discoveries at Island Gold, which looks highly unlikely given the record intercepts we’ve seen reported this year.

It’s easy to ignore the Gold Miners Index after a year of underperformance, but my favorite time to invest in the index is when everyone else has given up on it and most have moved on to greener pastures.

This seems to be the case currently, with the GDX 30% off its highs and most producers in the sector trading at their cheapest valuations in years. In summary, if this pullback in the GDX continues, I would keep a close eye on GOLD, AGI, and NSR. As noted, their respective low-risk buy zones are at $18.30, $7.30, and $8.00, respectively.

Disclosure: I am long GLD, NEM, AGI

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

GLD shares fell $0.06 (-0.03%) in after-hours trading Friday. Year-to-date, GLD has declined -3.22%, versus a 26.64% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| GLD | Get Rating | Get Rating | Get Rating |

| NEM | Get Rating | Get Rating | Get Rating |

| AGI | Get Rating | Get Rating | Get Rating |

| Get Rating | Get Rating | Get Rating | |

| NEM | Get Rating | Get Rating | Get Rating |

| GOLD | Get Rating | Get Rating | Get Rating |