It’s been a volatile couple of weeks for the Nasdaq Composite (QQQ), with the index starting the year up 10% but giving back a significant chunk of its gains the past two weeks. This sharp correction in the index has unnerved several growth stocks, with many sliding as much as 40% in less than a month after worries about rising yields.

Fortunately, this carnage has provided the first real buying opportunity for the highest-octane growth names, allowing some valuations to cool off after briefly hitting frothy levels. In this article, we’ll take a look at two names with industry-leading growth trading at reasonable valuations considering their growth prospects.

(Source: TC2000.com)

Peloton (PTON) and Silicon Motion Technology (SIMO) have minimal in common, with one being in the Semiconductor industry group and the other being in the Leisure group. Still, both share one key trait: exponential earnings growth. Looking ahead to FY2022, SIMO is expected to grow annual EPS by more than 26% year-over-year, while PTON is expected to grow annual EPS by over 110%. For SIMO, this growth should translate to follow-through from an earnings breakout, which is a very bullish development, while PTON is expected to move to profitability next year and enjoy triple-digit earnings growth for two years in a row. Generally, the best place to go fishing for top performers is among those growing annual EPS by more than 25% year-over-year, and both PTON and SIMO meet these requirements. Let’s take a closer look at the two companies below:

For those unfamiliar, Silicon Motion Technologies is a global leader in developing NAND flash controls for SSDs and other solid state storage devices. These high-performance storage solutions are used in PCs, smartphones, and commercial/industrial applications, and SIMO is currently the leading merchant supplier of SSD controllers used in PCs globally. The company’s sales mix is split between SSD solutions, SSD controllers, and eMMC+UFS controllers, with the bulk of its revenue coming from SSD controllers.

Over the past three years, the company has seen minimal growth in revenue, with gross margins flat and ranging from 48% to 49.5%. However, the company’s new 3-year plan is to deliver $1BB in sales in FY2023, which translates to a compound annual growth rate of above 20% from trailing-twelve-month sales of $540MM. Most impressively, SIMO expects to maintain 50% gross margins with these sales and enjoy higher operating margins closer to 30%. This confident guide is due to backlogs and significant purchase orders from customers, and it’s worth noting that the company has a history of delivering on its guidance.

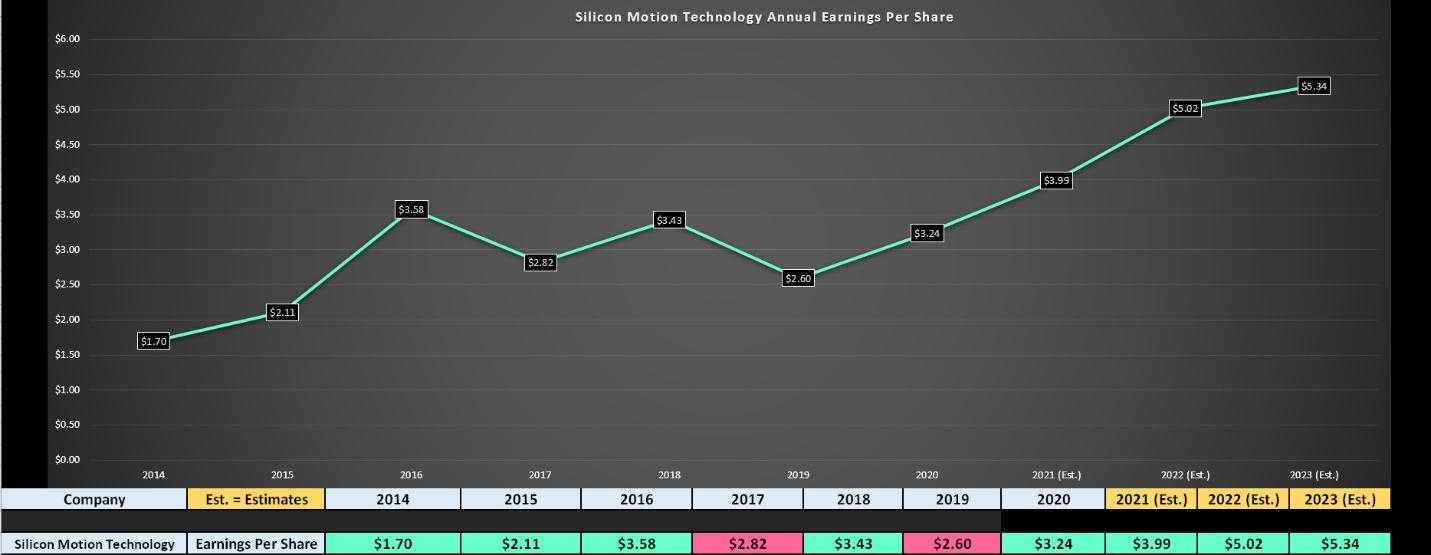

(Source: YCharts.com, Author’s Chart)

As shown above, SIMO’s annual EPS has been in a range since FY2016, which explains why the stock hasn’t made a ton of progress. However, FY2021 annual EPS estimates are sitting at $3.99, and this would translate to a new multi-year high in annual EPS for the stock and 23% growth year-over-year.

This would translate to an earnings breakout for the stock, and smart money seems to be sniffing out this breakout ahead of time, given that the stock just launched to new all-time highs. If we look ahead to FY2022, annual EPS is expected to accelerate further to $5.02, translating to 26% growth year-over-year ($5.02 vs. $3.99). Generally, earnings breakouts are one of the best setups for getting involved in stocks, and this looks like the early innings of a new multi-quarter uptrend for SIMO if this breakout is successful.

(Source: TC2000.com)

Looking at the above chart, we can see that SIMO has broken out of a nearly 4-year base on significant volume, suggesting that larger buyers are looking to get into the stock above $60.00. If this earnings breakout were coupled with lethargic price action and poor volume, I would be more skeptical of the upbeat guidance. However, the technical picture could not be brighter, and this base breakout targets a move to $80.00 if the breakout is successful. Therefore, if we were to see any dips to the $61.00 level, I would view this as a low-risk buying opportunity.

(Source: TC2000.com)

Moving over to Peloton, the stock has gotten beaten up lately, and sentiment for the stock is in the dumps for the first time in months. This is quite surprising given that Peloton was one of the top performers with a 430% return last year, and every stock is entitled to a sharp pullback to reset its chart. As the monthly chart above shows, PTON looks like it might be building out a new cup-shaped base here, and the volume on this pullback has not been that meaningful at all. In fact, it’s been relatively light compared to the volume we saw on the upside that took the stock from $80.00 to $165.00. While there’s no guarantee that volume doesn’t start coming into the stock heavily over the next few weeks, I would argue that this looks like weak hands being shaken out of the stock thus far.

So, how do the fundamentals look?

For investors looking for growth, there aren’t many stocks with more impressive annual EPS growth and revenue growth than Peloton. The company just came off a quarter where it reported 128% sales growth, and PTON currently has a 2-year average revenue growth rate of 103%, a figure that dwarfs 95% of other growth stocks. Some investors will argue that the best days for the stock are over, with bike sales likely to slow as gyms re-open, but PTON doesn’t need massive bike or treadmill sales to remain a growth story; it just needs a good chunk of existing members to stick with their current memberships and moderate growth in new members. T

his is because when you have 3MM members paying more than $30/month, you have a very enviable recurring revenue profile. Based on lower than expected churn in Q2, higher apparel sales than expected, and strong demand for the high-ticket Bike+ and Tread, I think earnings estimates could be on the conservative side.

(Source: YCharts.com, Author’s Chart)

If we look at the chart above, PTON is not currently reporting positive annual earnings per share, but this is expected to change in a big way in FY2021. This is because the company is set to transition from net losses per share to positive annual EPS, and this transition is typically one of the best times to get involved in growth stocks. This is because some growth funds require positive annual EPS before starting or building larger positions, and PTON is set to make this leap to having earnings on the table this year. While PTON might look expensive at more than 250x FY2021 annual EPS estimates, it’s worth noting that the market is forward-looking, and the $0.43 in annual EPS is hardly relevant. Instead, investors should be looking at FY2022 and FY2023 estimates, which are sitting at $0.94 and $2.01, respectively. Assuming PTON hits these estimates, it’s trading at just over 55x FY2023 annual EPS estimates, which is a dirt-cheap valuation for a company with a compound annual EPS growth rate of over 115%.

So, where to buy the stock?

While I would not chase PTON on its recent bounce off the lows to $115.00, I would expect any pullbacks closer to the $100.00 level to provide a low-risk buying opportunity. This is because it would place PTON at less than 50x FY2023 projected annual EPS and allow any weak hands that bought this dip to be shaken out. There’s no guarantee that the stock will re-test its recent in the $94.00 – $100.00 range, but this looks like a solid setup if we do get a pullback over the coming weeks.

While many investors are chasing the hot stock du jour and the leaders of 2021, SIMO and PTON offer industry-leading earnings growth at a reasonable price and are pulling back on low volume, which looks to be shaking out weak hands. This makes these two names solid bets if we do see some weakness in the market, with SIMO being the most compelling opportunity, given that it just broke out to a new all-time high. In summary, I see PTON and SIMO as two intriguing ideas to buy on dips, and I would view any pullbacks near PTON’s recent lows as low-risk buying opportunities.

Disclosure: I am long SIMO

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

PTON shares were trading at $114.95 per share on Thursday afternoon, up $3.63 (+3.26%). Year-to-date, PTON has declined -24.24%, versus a 5.62% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| PTON | Get Rating | Get Rating | Get Rating |

| SIMO | Get Rating | Get Rating | Get Rating |