The software sector (IGV) has seen a massive resurgence after a substantial correction in Q3 2019 and is now back on top as the leading industry group by performance in 2020. The sector has benefited from increased spending in digital transformation, artificial intelligence, and enterprises moving to the cloud, with the industry up an incredible 200% since the 2016 cyclical bull market began. I believe it would be wise to start to take some profits in the sector after what’s been a historic run, as valuation is finally starting to catch up to quite a few of the names. This does not mean the group has topped out long-term. However, it does mean that reward to risk is waning at current levels.

(Source: TC2000.com)

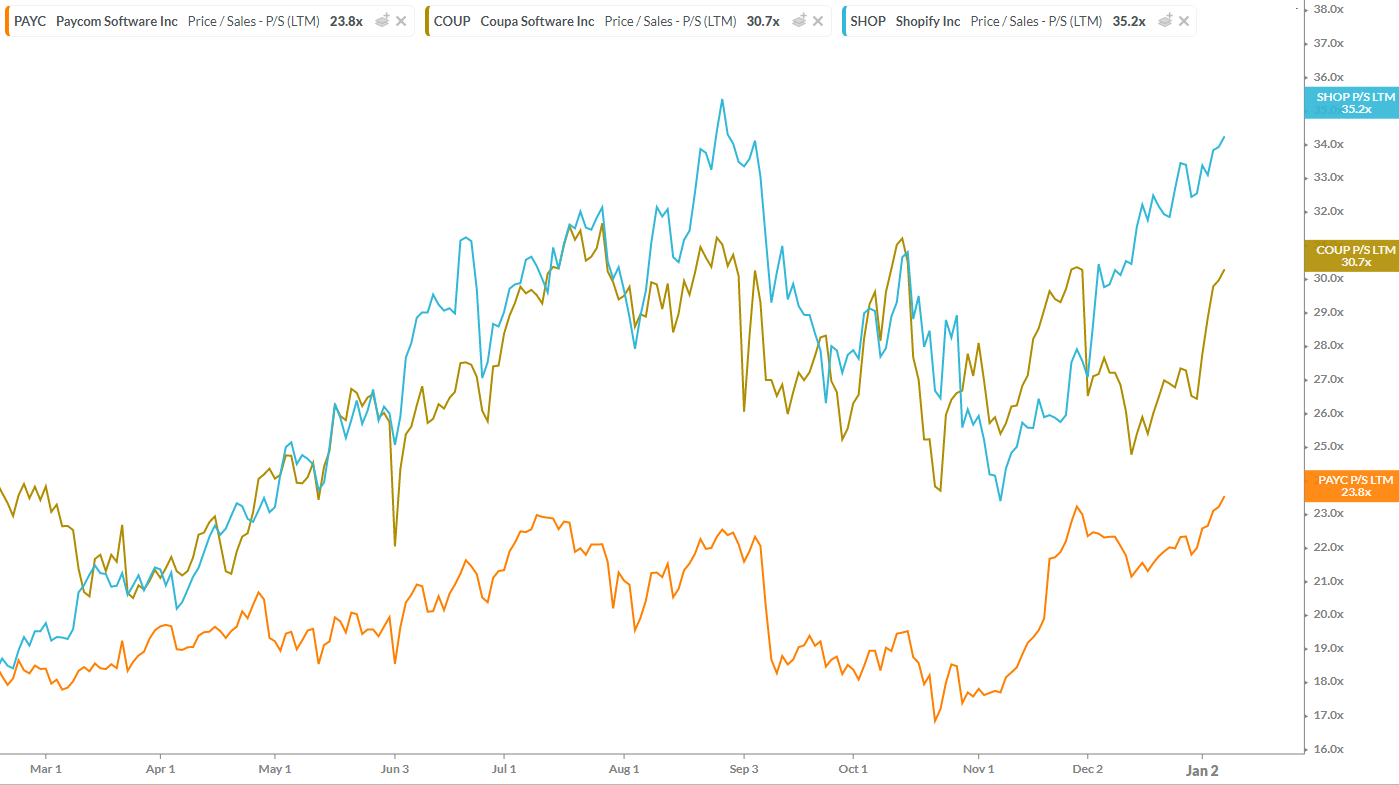

While several names in the sector have enjoyed incredible runs, three names continue to defy gravity and are also beginning to get expensive from a valuation standpoint. These three names are Paycom Software (PAYC), Coupa Software (COUP), and Shopify (SHOP), which are trading at revenue multiples of 24, 31, and 35, respectively. The last time we saw valuations like these among large-cap companies was in 1999 and 2000, and these stocks ended up sinking by over 50% over the next two years. I am not implying by any means that we need to see a repeat of this, but one could certainly argue that things are getting frothy here short-term.

(Source: Koyfin.com)

Paycom Software

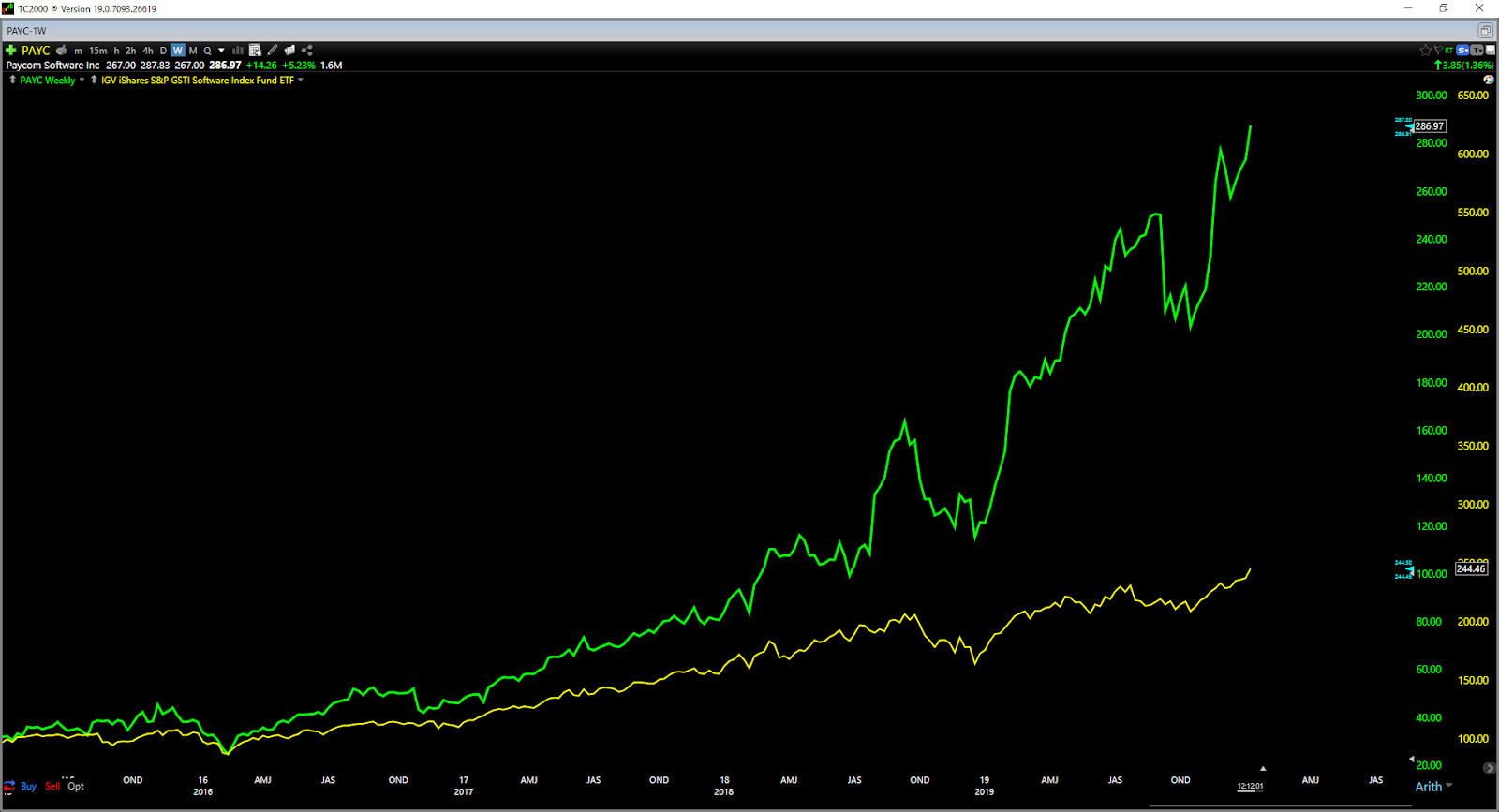

Beginning with Paycom Software, the company is a cloud-based human capital software companies that manages the employment life cycle for employers. The stock has seen one of the most impressive returns among the group, more than quadrupling the return of the Software group since 2016, with a 1080% performance. In this period, the company has managed to grow annual EPS from $0.87 in FY-2016 to estimates for $4.27 in FY-2020, but revenue growth rates are finally beginning to slow a little based on FY-2020 estimates.

While revenue growth has been hovering in the low 30% range for the past two years, we are likely to see it slip to the mid 20% level as we head into FY-2020. This is not a material deceleration or enough to derail the company’s growth, but it will make it harder for the company to beat earnings estimates going forward. Based on a revenue multiple of nearly 24 and potential deceleration in revenue growth rates, the company is getting quite expensive here near $290.00 a share. Therefore, I believe this is an opportune spot to book some profits.

(Source: YCharts.com, Author’s Chart)

(Source: TC2000.com)

Coupa Software

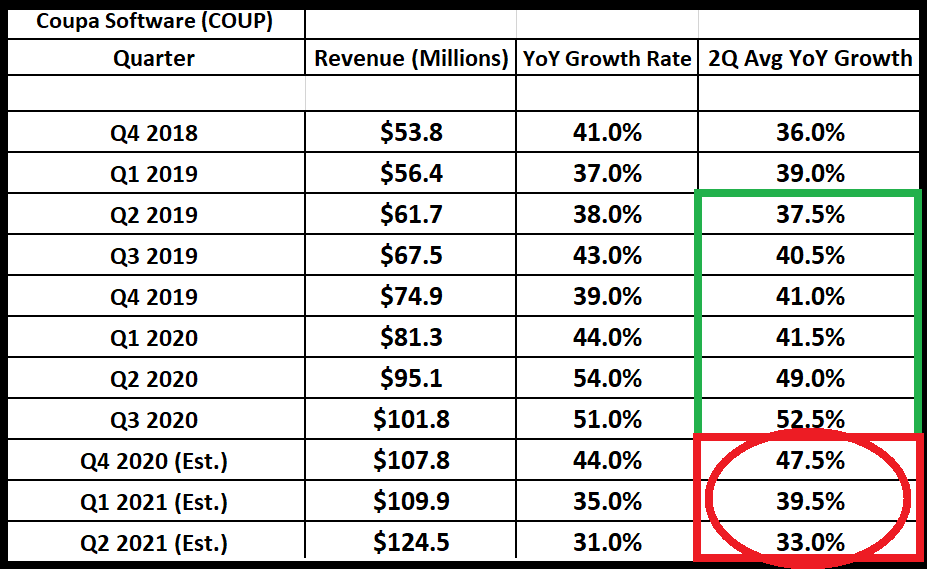

When it comes to Coupa Software, the stock has put up the weakest performance of the three names, but only because it only debuted in late 2016. The stock is up over 500% since its IPO debut in Q4 2016 and was one of the top performers in 2019 among the software names. Coupa Software operates in the cloud-base business spend management area and is a market leader with incredible revenue growth rates of 54% and 51% in the most recent two quarters, respectively.

The problem with Coupa Software, however, is that the valuation is getting quite stretched at a revenue multiple near 31. This valuation headwind is made worse for Coupa Software, given the fact that revenue growth rates are also decelerating materially here, similar to Paycom Software. Revenue growth rates expected to slide to 44% for fiscal Q4 2020 and 35% in fiscal Q1 2021. This would represent a sequential deceleration in revenue growth rates of 700 basis points unless the company can manage to put up a massive beat. Based on a revenue multiple of 30.7 and a revenue growth rate that’s set to decelerate, I believe investors would be wise to nail down some profits on Coupa Software above the $171.00 level.

(Source: TC2000.com)

(Source: YCharts.com, Author’s Chart)

Shopify

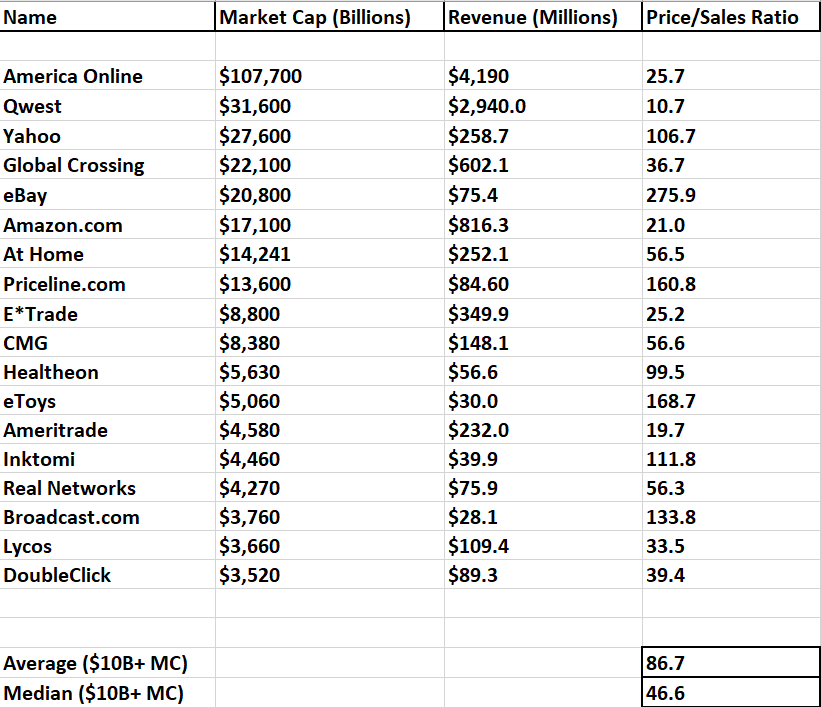

Finally, when it comes to Shopify, the stock is trading at near bubble-like valuations, at an exorbitant 35.2x price to sales. This valuation is above the valuation of America Online (AOL) in Q3 1999, which traded at over 25x sales. While much of this valuation is justified, given the stock’s massive annual EPS growth from $0.15 in FY-2017 to estimates of $0.89 for FY-2020, the revenue growth rate remains a problem here also.

(Source: The Internet Bubble, Author’s Table)

As the chart below shows, revenue growth rates have been trending down for several quarters in a row now, but these growth rates are expected to fall beneath 50% in FY-2020. This is not ideal, as it will revoke Shopify’s title as a high-growth stock, and give it a new title as a medium growth stock (20 – 50% revenue growth rates). Q2 2020 revenue is estimated to come in at $499.5 million, representing only 38% growth year-over-year.

(Source: YCharts.com, Author’s Chart)

Unless Shopify can beat these estimates materially by $30.0 million or better and avoid material deceleration, I believe it’s going to get more difficult for Shopify to continue beating earnings estimates. Revenue growth is the lifeblood of any growth company, and Shopify’s growth rates are finally getting to a point where they’re going to become a headwind for future growth. This happens to every growth stock as you cannot grow infinitely at 50%+ sales, but valuation and deceleration in growth are a deadly combination. Based on this, I believe the $425.00 plus level is a good spot for investors to book some profits.

In summary, the software group as a whole continues to remain expensive except for a few names, but Shopify, Paycom Software, and Coupa Software are the three priciest names in the group. I believe this is an excellent spot for investors to ring the register on 1/3 of their positions as the reward to risk remains poor at valuations resembling 1999 levels for these names. This does not mean they cannot go higher; it merely means that a lot of the juice has been squeezed out of these names at current levels.

SHOP shares were trading at $429.72 per share on Thursday afternoon, up $11.62 (+2.78%). Year-to-date, SHOP has gained 8.08%, versus a 1.35% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| SHOP | Get Rating | Get Rating | Get Rating |

| COUP | Get Rating | Get Rating | Get Rating |

| PAYC | Get Rating | Get Rating | Get Rating |