Smith & Nephew PLC ADR (SNN): Price and Financial Metrics

SNN Price/Volume Stats

| Current price | $30.06 | 52-week high | $31.72 |

| Prev. close | $30.28 | 52-week low | $23.69 |

| Day low | $29.86 | Volume | 238,490 |

| Day high | $30.15 | Avg. volume | 875,029 |

| 50-day MA | $29.33 | Dividend yield | 2.88% |

| 200-day MA | $27.38 | Market Cap | 13.17B |

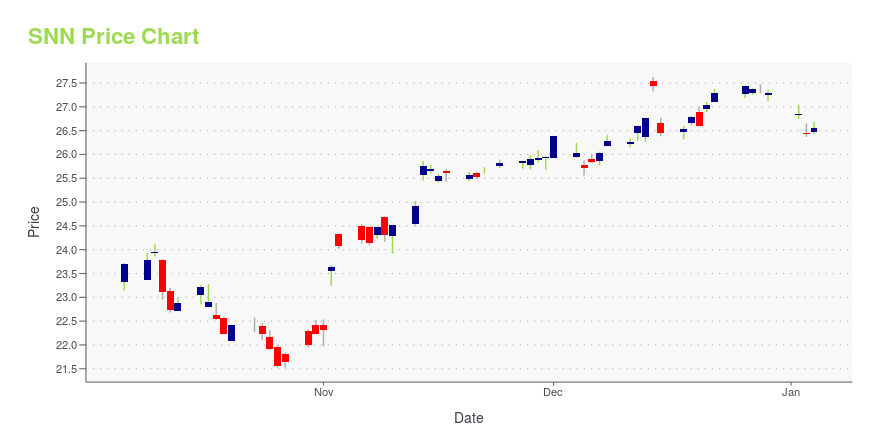

SNN Stock Price Chart Interactive Chart >

Smith & Nephew PLC ADR (SNN) Company Bio

Smith & Nephew plc, also known as Smith+Nephew, is a British multinational medical equipment manufacturing company headquartered in Watford, England. It is an international producer of advanced wound management products, arthroscopy products, trauma and clinical therapy products, and orthopaedic reconstruction products. Its products are sold in over 100 countries. It is listed on the London Stock Exchange and is a constituent of the FTSE 100 Index. (Source:Wikipedia)

SNN Price Returns

| 1-mo | 2.28% |

| 3-mo | 15.48% |

| 6-mo | 22.85% |

| 1-year | 8.52% |

| 3-year | 19.05% |

| 5-year | -18.54% |

| YTD | 24.25% |

| 2024 | -7.42% |

| 2023 | 4.35% |

| 2022 | -20.26% |

| 2021 | -16.26% |

| 2020 | -10.45% |

SNN Dividends

| Ex-Dividend Date | Type | Payout Amount | Change | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Loading, please wait... | |||||||||

Continue Researching SNN

Here are a few links from around the web to help you further your research on Smith & Nephew Plc's stock as an investment opportunity:Smith & Nephew Plc (SNN) Stock Price | Nasdaq

Smith & Nephew Plc (SNN) Stock Quote, History and News - Yahoo Finance

Smith & Nephew Plc (SNN) Stock Price and Basic Information | MarketWatch

Loading social stream, please wait...