We all know the stock market has been seen a steep increase in volatility over the past few months with the VIX hitting 32 — a nine month high.

But how does an increase in volatility, which is basically a measure of the price change magnitude within a given time frame, impact options’ values?

To understand this, we need to turn to one of the Greek’s; Vega.

Options traders sometimes use these terms interchangeably, and while they are related, they are two distinct concepts.

Volatility and the Black-Scholes Options Pricing Model

Volatility is one of the five inputs used in the basic Black-Scholes options pricing model.

Higher volatility means higher option prices. That’s because higher volatility means greater expected price swings.

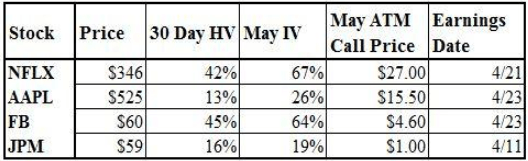

So it follows that stocks like Netflix (NFLX) and Facebook (FB) have higher volatility readings, and therefore are higher-priced options than more mature and stable companies like Apple (AAPL) and JP Morgan (JPM).

Take a look at this table:

Source:Options.com

Despite Apple having a higher underlying stock price than Netflix, its at-the-money May call is actually much lower in price than Netflix.

And note that both JP Morgan and Facebook are trading around $60. But the latter’s call is nearly five times the price.

This is almost entirely due to the differences in implied volatility. This is because Facebook is far more likely to make a huge move after earnings than JP Morgan.

Last quarter provided a perfect example of this. Facebook rose 14% in one day after reporting earnings. JP Morgan moved just 0.1%.

Vega and Implied Volatility Changes

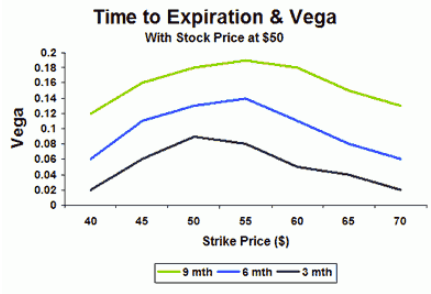

Vega isolates how a change in implied volatility will impact an option’s price by estimating how much its value changes when implied volatility moves 1%.

Source: Investopedia.com

Vega is highest for at-the-money strikes and increases as you go out in time. Notice also that peak vega also moves slightly out of the money as you go out in time. This is because the probability of a given price move occurring increases as the time frame is extended.

For example, if you’re speculating on a $10 price move, you have more of a chance of being right if you have a six-month time frame rather than one month.

A directional calendar spread, in which one buys a later-dated out-of-the-money option and sells a near-term out-of-the-money option is one strategy that tries to benefit from this concept.

When it comes to known events such as earnings reports, implied volatility will typically rise ahead of news and decline afterward.

Understanding the difference between historical (or realized) volatility and implied volatility is crucial in determining whether an option is relatively “cheap” or “expensive” and whether you want to be long or short vega.

In this case, one might want to be short vega through the sale of a straddle or iron condor, which would benefit from a decline in implied volatility even if the stock moves sharply following the news event.

Understanding what the options market is expecting, or “pricing in” as measured by implied volatility, will help you determine just how large a price move will be needed for a profit when you are long options. And vega will tell you how much a change in implied volatility following the report will impact the price of the options.

Often, a decline in IV (also known as vega risk) will offset the impact of price gains in the underlying stock. This is how you can be correct on a stock’s direction and still lose money on an options position.

Volatility helps define an option’s cost, and vega helps determine a position’s profit or loss. Therefore, it is critical to understand both concepts.

It’s a good idea to use a basic options calculator like this one from the Chicago Board of Options Exchange (CBOE) to play around with changes in implied volatility over different time frames and see what the impact on the option’s price will be.

The Greatest Trading Book

Ever Written

I have been working very hard to introduce you to the greatest trading book ever written. At my trading firm, the very first thing that any new trader had to do was read this book. They wouldn’t be allowed in my office if this book was not read. Now, I’ve taken this book and built an entire trading system around it. For anyone that has any interest in trading, this is a must-read. It’s about success, failure and then success again. This book is being offered today, Get Your Copy Now

About the Author: Steve Smith

Steve has more than 30 years of investment experience with an expertise in options trading. He’s written for TheStreet.com, Minyanville and currently for Option Sensei. Learn more about Steve’s background, along with links to his most recent articles. More...

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Best & Worst Performing Mega Cap Stocks for June 19, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for June 18, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for June 17, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for June 16, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.