When athletic shoe retailer, Foot Locker (FL) reported earnings last week, the stock tumbled some 15% and has continued to slide over the following days. I think it is now approaching a great buying opportunity from both a technical and fundamental standpoint.

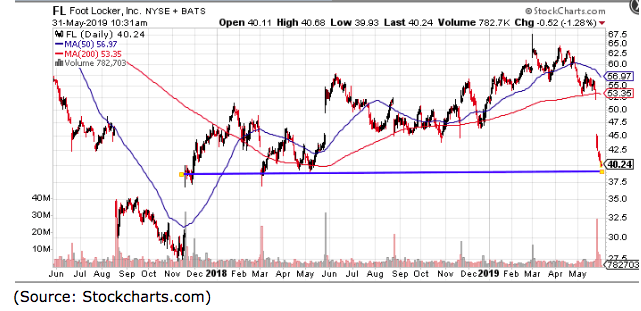

The technical picture is fairly simple; FL is now back to its lowest levels in 18 months and approaching major support near the $40 level.

Of course, a decline in price to new lows doesn’t make the shares a bargain if companies fundamentals are deteriorating.

Foot Locker did post slightly worse-than-anticipated Q1 sales and earnings results. But, almost all metrics were still positive, and I think the market grossly overreacted to what was perceived as a ‘miss’ and some overriding concern that are plaguing retailers in general.

While many mall or outlet-based retailers are struggling, Foot Locker is outperforming competitors and still growing against a tough backdrop.

Overall, revenue grew 8% and eps were up 7.5% year-over-year.

Particularly impressive was the direct-to-consumer (DTC) online sales increased 14.8% y/y, driving online penetration to 15.4% of sales from 13.9% in the comparable quarter a year ago. The growth in this channel demonstrates Foot Locker’s ability to adapt to the digital world, which is crucial to any retailer hoping to remain competitive.

But, probably the most interesting number was the comp of physical stores, which was up 3.9% year-over-year demonstrating the underlying value of the Foot Locker model.

Investors seem to have a difficult time believing Foot Locker can thrive as an outlet/mall-based chain. But, as a company that serves younger customers often in areas with lower rates of online sales penetration, the physical store is an attractive asset.

Additionally, Foot Locker’s ability to display the product and partner with key vendors like Nike (NKE) creates a selling environment that induces purchases.

While online sales are still growing at 50% in-person sales still represent over 80% of all retail sales, meaning physical assets retain value. The nature of the footwear industry, with its market-specific allocations, high turns on premium product, and extensive product displays, allows Foot Locker to capture real value from its physical locations.

That said, Foot Locker still owns an excess of stores in the U.S. and Europe. As a result, the company closed 25 stores during the quarter, and it expects to continue shrinking its footprint by 6% over the next year — with underperforming units such as Lady Foot Locker, comprising the bulk of the closings.

Also, while China and tariffs were not mentioned on the earnings call, it’s clear that investors are worried about the impact of tariffs on Foot Locker’s earnings. The impact remains to be seen and at this point, it seems a worst-case scenario is priced in any resolution, which would be a positive catalyst.

All told the company’s numbers all stack up positively to reports over the prior eight quarters, which helped drive shares from $40 to a high of $70, just this past March, making this return to $40 unwarranted and great a buying opportunity.

About the Author: Steve Smith

Steve has more than 30 years of investment experience with an expertise in options trading. He’s written for TheStreet.com, Minyanville and currently for Option Sensei. Learn more about Steve’s background, along with links to his most recent articles. More...

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Best & Worst Performing Mega Cap Stocks for July 11, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 34.37%.

Best & Worst Performing Mega Cap Stocks for July 10, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 9, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 8, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.