We’ve seen a strong recovery off of the lows for the Nasdaq-100 Index (QQQ), with the ETF up nearly 10% since late September and many growth stocks more than doubling this performance. While we continue to see significant complacency across most sentiment indicators, which suggests some caution is warranted, further weakness or a re-test of the September lows could set up an exceptional buying opportunity. Therefore, investors would be wise to begin building their shopping lists. In this article, we’ll examine two tech names with explosive sales growth that look to be under significant accumulation by funds.

(Source: TC2000.com)

While LivePerson (LPSN) and Farfetch (FTCH) have little in common, with one being a software name and the other being in the online retail space, both do share one common trait: explosive sales growth. This trait, combined with relative strength, is often a great predictor for strong outperformance vs. peers, and it helps both companies are also leaders in their space. In LivePerson’s case, the company’s Conversational Cloud is one of the hottest products on the market for medium-sized businesses and enterprises navigating away from call centers. LivePerson’s net revenue retention rate of over 110% is proof that existing customers are more than satisfied with its effectiveness.

Meanwhile, FarFetch offers customers the broadest range of products and categories from luxury fashion brands online, selling products from companies like Burberry, Prada, Jimmy Choo, Fendi, and Versace. The company’s acquisition of New Guards Group last year has increased its customer count to a whopping 2.5 million, giving it a commanding lead in the online luxury market. Let’s see what makes both of these companies so unique below:

Beginning with Farfetch, the $9 billion-dollar online retailer has seen exponential growth since going public in late 2018, with quarterly sales soaring from $134.5 million in Q3 2018 to estimates of $371.1 million in Q3 2020.

This translates to a compound annual sales growth rate of over 66%, which makes Farfetch one of the top-100 growth companies trading on the US market currently. In Farfetch’s most recent quarter, the company reported near-record sales of $364.7 million, translating to 74% growth year-over-year. It’s worth noting that the company was lapping a year of 43% growth, which means that the company’s two-year stacked growth rate comes in at an unheard of 117%.

In terms of Gross Merchandise Value [GMV], the company reported GMV of $721 million, up 48% year-over-year. Some investors might be turned off because this massive growth still led to net losses per share of $0.20, but estimates show that the company could be profitable by as early as FY2023 as it benefits from economies of scale.

(Source: YCharts.com, Author’s Chart)

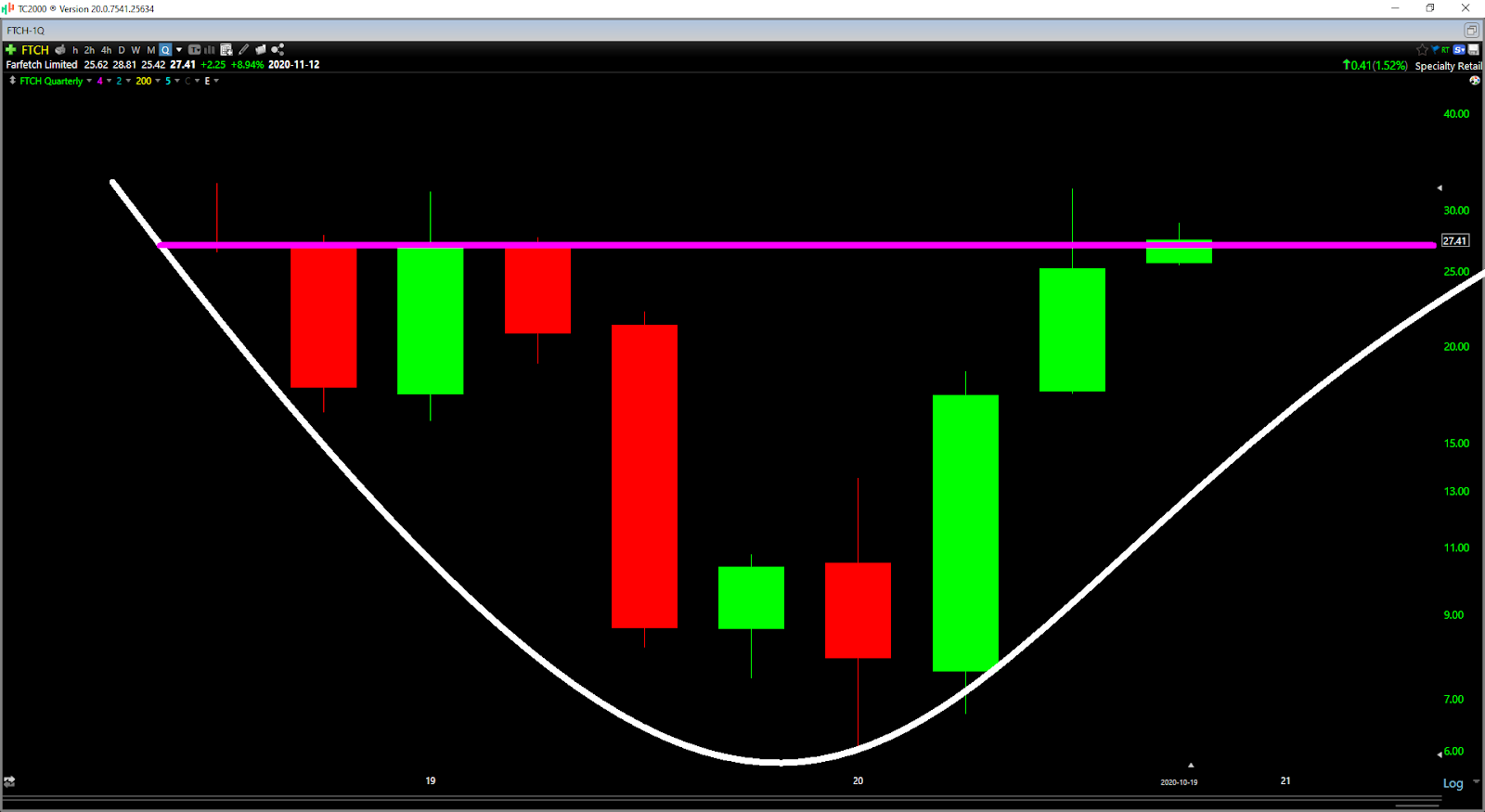

When it comes to the technical picture, it’s hard to find many companies that hold a candle to Farfetch, with the stock building out a multi-year cup base since its IPO debut. Generally, these primary IPO bases can lead to explosive uptrends if they do breakout successfully, and Farfetch clearly has a catalyst for this breakout.

This catalyst comes in the form of market-leading sales growth and a push towards profitability in FY2023. The good news for Farfetch is that it’s in an area of the market that is less affected by the ongoing recession, with most of the customers buying luxury goods being in the higher-income categories. This is similar to what we’ve seen with Restoration Hardware (RH), as the company has continued to grow sales year-over-year despite softness in the economy. Based on Farfetch’s improving fundamentals and the strong technical picture, I would view any pullbacks below $26.25 as low-risk buying opportunities.

(Source: TC2000.com)

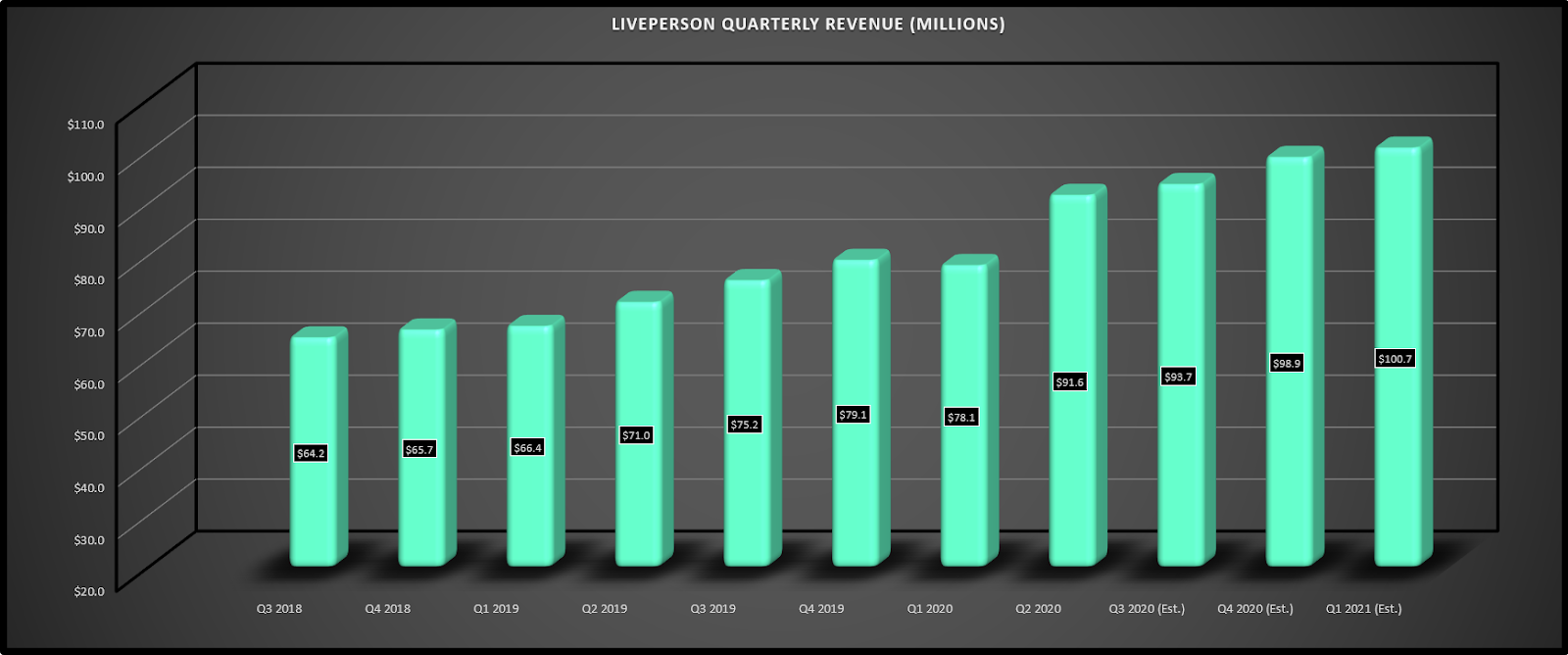

Moving over to LivePerson, the company has robust sales growth as well, with a significant acceleration in the most recent quarter. As we can see below, the company reported $91.6 million in revenue for Q2, up 29% year-over-year, and this translated to an 1100 basis point acceleration sequentially from the 18% growth rate in Q1 2020.

The catalyst for this improved growth rate is the rapid adoption of LivePerson’s cloud communication services, with enterprise and mid-market average revenue per user growing 25% year-over-year. It’s also worth noting that revenue retention rates exceeding the guidance of 110%. The company also closed seven 7-figure deals in Q2 alone, and at the same time, as it sees accelerating revenue, LivePerson is reducing its cash burn to below $50 million.

This is helped by the fact that the company’s AI is continuing to learn from the tens of millions of interactions on LivePerson’s Conversation Cloud and the fact that LivePerson has moved from office to a work-from-home setting, which should drive long-term cost savings.

(Source: YCharts.com, Author’s Chart)

While LivePerson has already broken out of its primary IPO base years ago, the stock has just recently broken out of a new 1-year base in Q3 on massive volume. The stock looks to be building a new base atop its previous resistance near $45.00, and it’s worth noting that we’ve seen minimal selling volume during the recent correction.

This suggests that the funds accumulating after the blow-out Q2 report are not selling their shares and maybe adding to their positions. I would not be inclined to start a new position at current levels near $60.00, but I believe that any pullbacks to $52.50 or lower would provide low-risk buying opportunities. Assuming we do see a pullback this deep, LivePerson would drop a revenue multiple of just 11x, a more than the reasonable valuation for a software name with accelerating sales growth.

With the major market averages up massively since their March lows, some investors are understandably discouraged that they’ve missed the boat. However, while many names are quite overvalued and high-risk heading into the Q3 Earnings Season, I believe any weakness in Farfetch below $26.25 and LivePerson below $52.50 would provide low-risk buying opportunities. Therefore, for investors looking for stocks that still have a significant runway for growth, these are two names worth keeping at the top of one’s shopping list if we see some more turbulence in Q4.

Disclosure: I am long LPSN, RH

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

Top 11 Picks for Today’s Market

7 Best ETFs for the NEXT Bull Market

5 WINNING Stocks Chart Patterns

LPSN shares were trading at $59.82 per share on Tuesday afternoon, up $0.75 (+1.27%). Year-to-date, LPSN has gained 61.68%, versus a 8.52% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| LPSN | Get Rating | Get Rating | Get Rating |

| QQQ | Get Rating | Get Rating | Get Rating |

| FTCH | Get Rating | Get Rating | Get Rating |