It’s been an exciting start to the year for the Nasdaq Composite (COMPQ) thus far, with the index on track for one of its strongest starts out of the gate in history. As we head into the back half of February, the Nasdaq Composite is already up 9% year-to-date, or an annualized return of nearly 70% if this pace continues.

This strong momentum has been driven by solid earnings reports out of names like Netflix (NFLX) and Tesla (TSLA), as well as continued outperformance from Semiconductors. However, in a market where it’s tough to find stocks that aren’t extended short-term, two tech stocks are looking attractive as they build new bases, with high-octane earnings growth and a commanding lead in their industry. For investors looking to add exposure in a market that doesn’t offer any dips, these two names look to be offering a low-risk opportunity.

(Source: TC2000.com)

Peloton (PTON) and Zoom Video (ZM) were two of last year’s largest leaders, enjoying triple-digit returns vs. the S&P-500’s 15% return, with both companies seeing massive demand for their products. This was because consumers looked to find ways to continue exercising at home and to converse with friends & family during the pandemic.

Of course, Zoom Video’s dominant tailwind came from the work-from-home movement, given that most travel and face-to-face meetings out of the picture. Despite these companies continuing to post incredible growth in their most recent quarter, they have not kept up with the market since Q4 and have spent the past quarter building new multi-month bases. Generally, when market leaders take a break and relieve their overbought conditions, this is an excellent opportunity to look at starting a new position. Of course, this view is emboldened by the fact that both companies just put up incredible earnings. Let’s take a closer look below:

(Source: Company Earnings Slides)

Beginning with Peloton, the company just came off a massive quarter, with Connected Fitness Subscriptions up 134% year-over-year to 1.67MM, and paid Digital Subscriptions up 472% to 625,000. For nay-sayers suggesting that there was no hope in consumers paying a $30~/month fee to exercise at home, this report certainly squashed any of these doubts. Based on strong growth in subscriptions and minimal churn, the company reported revenue of $1.06~BB in fiscal Q2 2021 alone and has guided for $4.1BB in revenue in FY2021.

This exceptional growth despite vaccine roll-outs suggests that many fitness enthusiasts are sticking with their Pelotons, and many are looking to join the workout-from-home movement with no interest in going back to crowded gyms. Therefore, while the global pandemic was clearly a massive tailwind for Peloton in FY2020, it’s looking like the pandemic’s length relative to expectations will create more long-term Peloton users than initially anticipated.

However, the most bullish takeaway from the report was that Peloton could not keep up with demand, which is great news for long-term investors. While this difficulty meeting demand could undoubtedly weigh on fiscal Q3 2021 results with a guide for only single-digit sequential revenue growth, it’s clear that the demand should be fulfilled long-term, with Peloton being the leader in interactive fitness products & services. So, for investors with a long-term time horizon, this negativity about supply chains could be creating a buying opportunity.

(Source: YCharts.com, Author’s Chart)

As shown above, Peloton is set to be profitable for its first year in FY2021, with annual earnings per share [EPS] estimates sitting at $0.42. While this looks outrageously expensive for a stock trading near $140.00, it’s important to note that PTON has a top-50 growth rate in the market currently out of 7000 US-listed stocks, with expected compound annual EPS growth of 91% looking out to FY2024 ($0.42 vs. $2.96). So, while Peloton might look expensive relative to traditional metrics like trailing P/E, it’s actually reasonably priced at less than 50x FY2024 annual EPS estimates in a market where triple-digit earnings growth often receives a multiple of closer to 150. Don’t believe me? Look at names like Chewy (CHWY) with subscription businesses and lower margins than PTON.

(Source: TC2000.com)

If we look at the technical picture, this is the first real pullback we’ve seen for PTON since its massive breakout, and the first base after a massive run for a stock is typically a buying opportunity. As we can see, PTON has sold off for two months in a row but has barely given up any of its December gains and is coming into its monthly moving average, which has been strong support in the past. While there’s no guarantee that this level holds, buying near this monthly moving average for top-50 growth stocks is generally a solid entry point.

Therefore, I would view any pullbacks below $145.00 on PTON as low-risk buying opportunities. The key to this setup working is defending this monthly moving average, so we want to see $130.00 defended at all costs going forward.

(Source: Company Presentation)

Moving over to Zoom Video, the company also had a strong report, with fiscal Q3 2021 revenue up 367% year-over-year to $777MM. Meanwhile, customer growth increased 485% year-over-year for customers with ten or more employees, and enterprise growth came in at triple-digit levels as well. However, the most important figure was trailing-twelve-month net expansion rates, which spent a tenth consecutive quarter above 130%. This figure suggests that ZM is clearly the market leader and that we’re seeing customer satisfaction, with clients not moving to cheaper alternatives in the video communications space.

Critics of ZM have noted that the company is barely profitable despite its incredible growth and that demand is set to drop off as soon as life returns to normal in an ex-COVID-19 world. While there’s no question that we will see a surge in demand for dining out, traveling, shopping, and many other things, I am not sure that businesses will go back to their previous ways. This is because businesses traditionally have spent like crazy on travel and real estate, which has compressed margins, simply due to the fact that they didn’t know better, they didn’t have time to change their ways, or it wasn’t a priority.

However, it’s clear that some companies can work from home and save time and money with Zoom, and the pandemic has been a perfect test case to show that travel is not necessary in many cases, nor is crowding several people in a room multiple times a week for team meetings. Therefore, for businesses looking to win long-term by saving time and expanding their margins, I don’t see any reason why they wouldn’t stick with Zoom.

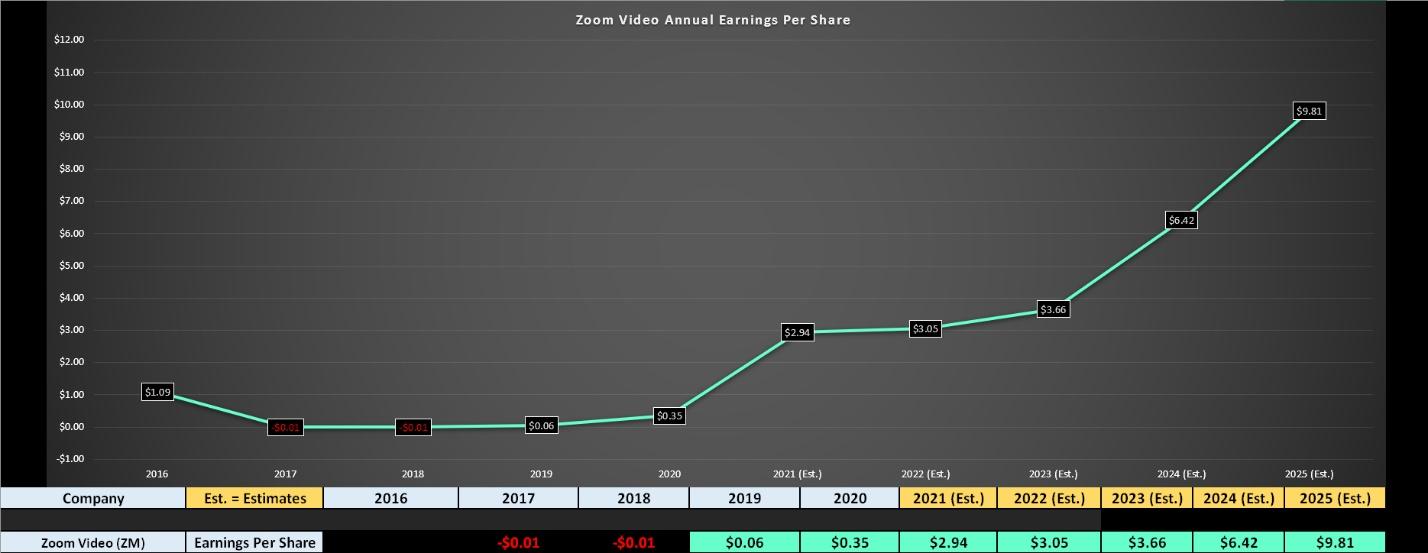

(Source: YCharts.com, Author’s Chart)

Addressing the profitability issue, ZM indeed earned less than $1.00 in annual EPS last year despite unprecedented demand. Still, a look at FY2021 and future earnings estimates suggests this is a very stale number. In fact, FY2021 annual EPS is expected to increase by nearly 1000% year-over-year, with estimates of $2.94 vs. $0.35. This represents one of the top-10 growth rates in the market currently, and top-10 growth stocks typically do not simply fade away.

If we look ahead to FY2024 estimates, earnings are projected to more than double again after nearly 800% growth in FY2021, translating to a compound annual EPS growth rate of 95% between FY2020 and FY2025 ($9.81 vs. $0.35). This is incredible growth that’s unrivaled in the large-cap space currently.

So, while ZM is arguably expensive at nearly 150x FY2021 sales, I would argue it’s actually cheap based on the fact that I think they can earn over $4.50 in FY2023, and estimates are conservative. Assuming Zoom Video earns $4.50 in annual EPS in FY2023, the stock is trading at less than 100x earnings in a market that typically pays up to 150x earnings for triple-digit growth. This would translate to a Q1 2023 price target of closer to $675.00.

(Source: TC2000.com)

If we look at the chart below, we can see that Zoom Video is building out a new cup base, with this also being its first base (like PTON) since its massive stage-1 breakout. While I don’t see the stock as a buy at current levels, I would expect any dips to the lower edge of this base near $350.00 to be a low-risk buying opportunity. If we do see some weakness in the coming weeks below $360.00, I believe this would provide a decent entry point for investors.

In a market where it’s tough to find stocks that haven’t gone parabolic, ZM and PTON are two market leaders with incredible growth that are building out new bases. While PTON is the only one I see as a low-risk buying opportunity, I believe both names should be near the top of one’s watchlist going forward. For now, I remain long PTON and NFLX and may look to start a position in ZM if we see further weakness.

Disclosure: I am long NFLX, PTON

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

7 Best ETFs for the NEXT Bull Market

5 WINNING Stocks Chart Patterns

ZM shares were trading at $435.20 per share on Thursday afternoon, up $4.20 (+0.97%). Year-to-date, ZM has gained 29.02%, versus a 4.02% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| ZM | Get Rating | Get Rating | Get Rating |

| PTON | Get Rating | Get Rating | Get Rating |

| TSLA | Get Rating | Get Rating | Get Rating |

| NFLX | Get Rating | Get Rating | Get Rating |