Earnings season officially kicks off next week with some of the big banks such as JP Morgan (JPM) and Bank America (BAC) set to report on Tuesday and the first of FAANG, Netflix (NFLX) reports on Thursday.

Earnings can be very tricky to trade as there are many moving and unknown parts; will the company miss or beat expectations, what will be the guidance, will traders ‘sell the news’ in profit-taking and will the recent overall market volatility override the results?

But there is one predictable pricing behavior that savvy options traders use to produce steady profits.

The biggest mistake novices make is purchasing puts or calls outright as a means of a directional “bet.” They are usually disappointed with the results, even if the stock moves in the predicted direction the value of the option can actually decline, and result in the loss despite being “right.”

Don’t Get Post Earnings Premium Crushed

The problem is that they failed to account for the Post Earnings Premium Crush (PEPC) which is my label for how the implied volatility contracts immediately follow the report no matter what the stock does.

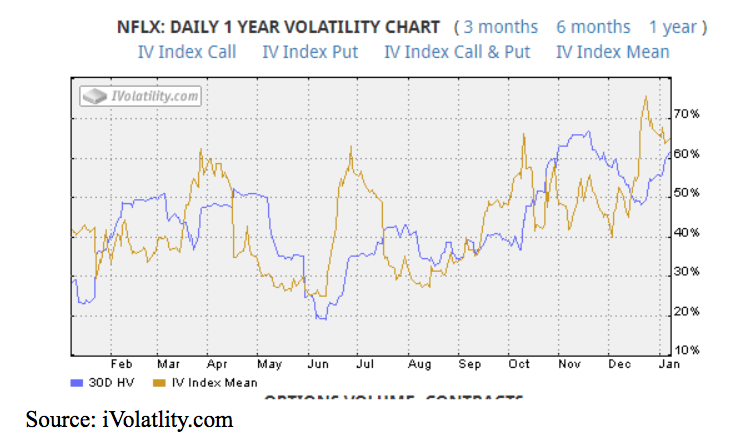

You can see the repeating pattern of implied volatility of Netflix’s options spiking and retreating on the quarterly reports.

You’ll often hear traders cite what percentage move options are “pricing in” or the earnings. The quick back of the envelope calculation for gauging the magnitude of the expected move is to add up the at-the-money straddle.

This article does a great job of explaining how to use the straddle to both assess expectations and potentially profit.

Once option traders are armed with this bit of knowledge they could advance to use spreads to mitigate the impact of PEPC when looking to make a directional bet. Some will graduate to getting this predictable pricing behavior in their favor by selling premium via strangles or the more sensible limited-risk iron condors. But these strategies still carry the risk of trying to predict if not the direction, then the magnitude of the move.

Here’s a lead-in to a list of the most historically-volatile stocks following earnings reports., meaning they are likely to see both the largest increase in implied volatility leading up to earnings and the largest PEPC.

The Pre-Earnings Trade

The true professionals pursue a safer and more reliable path of positioning in anticipation of the increase in implied volatility that precedes earnings and avoids the actual event altogether. Just as PEPC is predictable, so is the pumping up of premium leading into the event; it’s just more subtle in that it occurs incrementally over the course of many days.

One strategy for taking advantage of rising IV leading into earnings is calendar spread in which you sell an option that expires prior to the earnings while simultaneously purchasing one that expires after the event. Like any calendar spread it will benefit from the accelerated decay of the nearer-dated options sold short. But this has the added tailwind of earnings approaching an option which includes seeing it rise, causing the value of the spread to increase. To keep the position delta neutral, both put and call calendars should be established.

These positions must be established in advance and closed before the actual earnings. The profits might not be as dramatic as catching a huge post-earnings move, but they can be substantial. More importantly, they can be consistent and have a high probability.

With weekly options, there should be plenty of situations in the coming weeks to take advantage of the rise in IV leading into earnings. This site provides a good starting point of names and their options-specific pricing tendencies. With most offering weekly options, there should be plenty of opportunities for double calendars. As always, do your own research and confirm the reporting dates. But, this offers a great starting point.

About the Author: Steve Smith

Steve has more than 30 years of investment experience with an expertise in options trading. He’s written for TheStreet.com, Minyanville and currently for Option Sensei. Learn more about Steve’s background, along with links to his most recent articles. More...

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Best & Worst Performing Stock Industries for July 26, 2024

Led by ticker KGJI, "Fashion & Luxury" was our best performing stock industry of the day, with a 1,299.75% gain.

Best & Worst Performing Mid Cap Stocks for July 26, 2024

GSHD leads the way today as the best performing mid cap stock, closing up 29.21%.

Best & Worst Performing Small Cap Stocks for July 26, 2024

KGJI leads the way today as the best performing small cap stock, closing up 100,000.00%.

Best & Worst Performing Large Cap Stocks for July 26, 2024

NOW leads the way today as the best performing large cap stock, closing up 13.40%.