It’s been a strong start to the month of May for the markets (SPY), and the tech stocks and high-growth names continue to see a relentless bid, with the Nasdaq 100 (QQQ) completely de-coupling from the major averages, up 10% year-to-date. While there is undoubtedly lots of long-term potential with many of these names, it’s beginning to look a little worrisome short-term, with the number of companies trading above 35x sales climbing back to double-digits this week. Also, we have several growth stocks quite extended from their bases, suggesting that the potential of 15-20% corrections in these names would not be surprising, especially some of the high-flyers that are up over 50% year-to-date. However, while a dip is possible, it isn’t the end of the world, and investors should be preparing a list of the market leaders, where they can look to add exposure on dips, while the uninitiated are panic selling after chasing this week. I believe that there are two market leaders who fit this bill: Docusign (DOCU) and Facebook (FB).

While Docusign and Facebook may not seem to have anything in common at first glance, they are both companies that have managed to roar to new all-time highs despite the turbulent market we’ve seen this year. Both offer massive earnings growth and a moat around their products. For Facebook, it’s one of the most popular social media websites with hundreds of millions of active members and massive brand recognition. When it comes to Docusign, it has a massive lead in the E-Signature space, with acquisitions focused on artificial intelligence to make their products more seamless and even more efficient, like the recent acquisition of Seal Software. Based on their strong forward earnings growth estimates, I believe both offer exceptional opportunities, assuming investors look to buy them on dips. Let’s take a look at Docusign below:

Beginning with Docusign, the company saw massive earnings growth last year, with FY-2020 annual earnings per share coming at $0.31, translating to earnings growth of 245% year-over-year. It’s important to note that this was obviously before the recent pandemic, and FY-2021 estimates are forecasting continued robust growth as we see more of a need for E-Signature products given the push towards social distancing. While customers of Docusign previously may have been predominantly those early to catch onto the trend, and those looking for efficiencies in their business, the social distancing requirements in place have made E-Signature products a necessity to operate effectively in a new COVID-19 dominated world. Therefore, I would expect the significant onboarding of new clients to accelerate, and it’s also possible that the company can up-sell current clients as their usage increases across the entire organization with less face to face contact than most companies are used to.

(Source: YCharts.com, Author’s Chart)

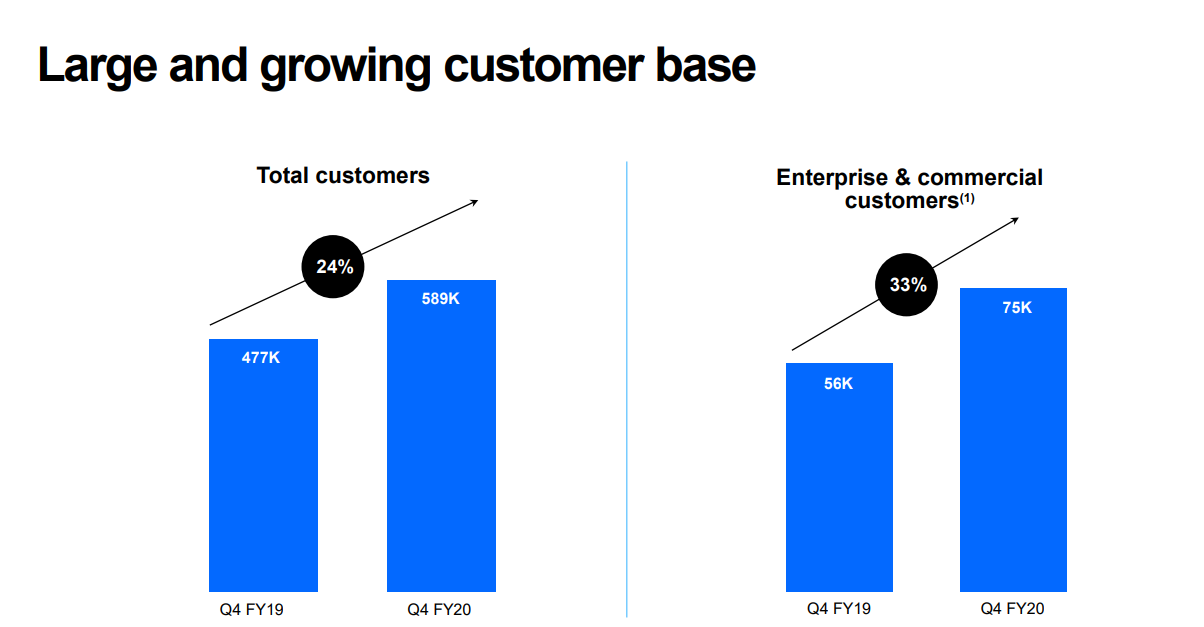

As shown in the image below, Docusign grew its total customer count by 24% year-over-year to 589,000 customers to finish FY-2020, with an annual growth rate of 33% in enterprise & commercial customers. The company has estimated that the 589,000 total customer count represents just over 1% of the overall addressable market. It’s certainly possible the company could capture at least 2-3% of this TAM given its market-leading position and significant lead on competitors. Similar to how Google became a household name, and this led to its mass adoption since, Docusign is now becoming somewhat of a household name, as the product has changed the way we sign mortgages, real estate transactions, and all types of legal documents.

(Source: Company Presentation)

Circling back to FY-2021 earnings estimates, they are positively reflecting this trend of continued growth in customer count and billings, with estimates for FY-2021 annual EPS of $0.52, translating to a growth rate of 68% year-over-year. It’s important to note that this robust growth rate is lapping a year of 245% growth in FY-2020, giving the company a two-year stacked growth rate of 313%. While Docusign certainly looks expensive to the average investor at over 100x forward earnings, I don’t believe P/E ratios are all that useful for companies growing earnings at near triple-digit growth rates. This is because names like Amazon (AMZN), and Shopify (SHOP) trading at well over 300 to 400x earnings in their infancy, but these premiums were clearly justified. Therefore, I believe Docusign is priced expensively for a reason, and I think any dips would provide buying opportunities. I remain long the stock for the time being, but I believe there would be an opportunity to add exposure if the stock can pull back to $105.00 or lower. Currently, the stock is a little extended from its multi-year base and getting a tad overbought. However, a drop towards the $105.00 level would relieve any overbought condition, and present an attractive buying opportunity, in my opinion.

(Source: TC2000.com)

Moving over to Facebook, we have a strong earnings trend here as well, though it might not look like it at first glance with FY-2019 annual EPS down 15% year-over-year. It’s worth noting that this was the only year of negative earnings growth for Facebook in the past decade, and this drop was an anomaly, as FY-2020 estimates are forecasting a return to prior highs. Current FY-2020 estimates are sitting at $7.55, with FY-2021 estimates at $9.32, and this would translate to a return to earnings highs this year, and a 22% growth rate next year. This is exceptional growth for a mega-cap like Facebook, and the company is trading at a more than reasonable forward P/E ratio near 26 based on these estimates.

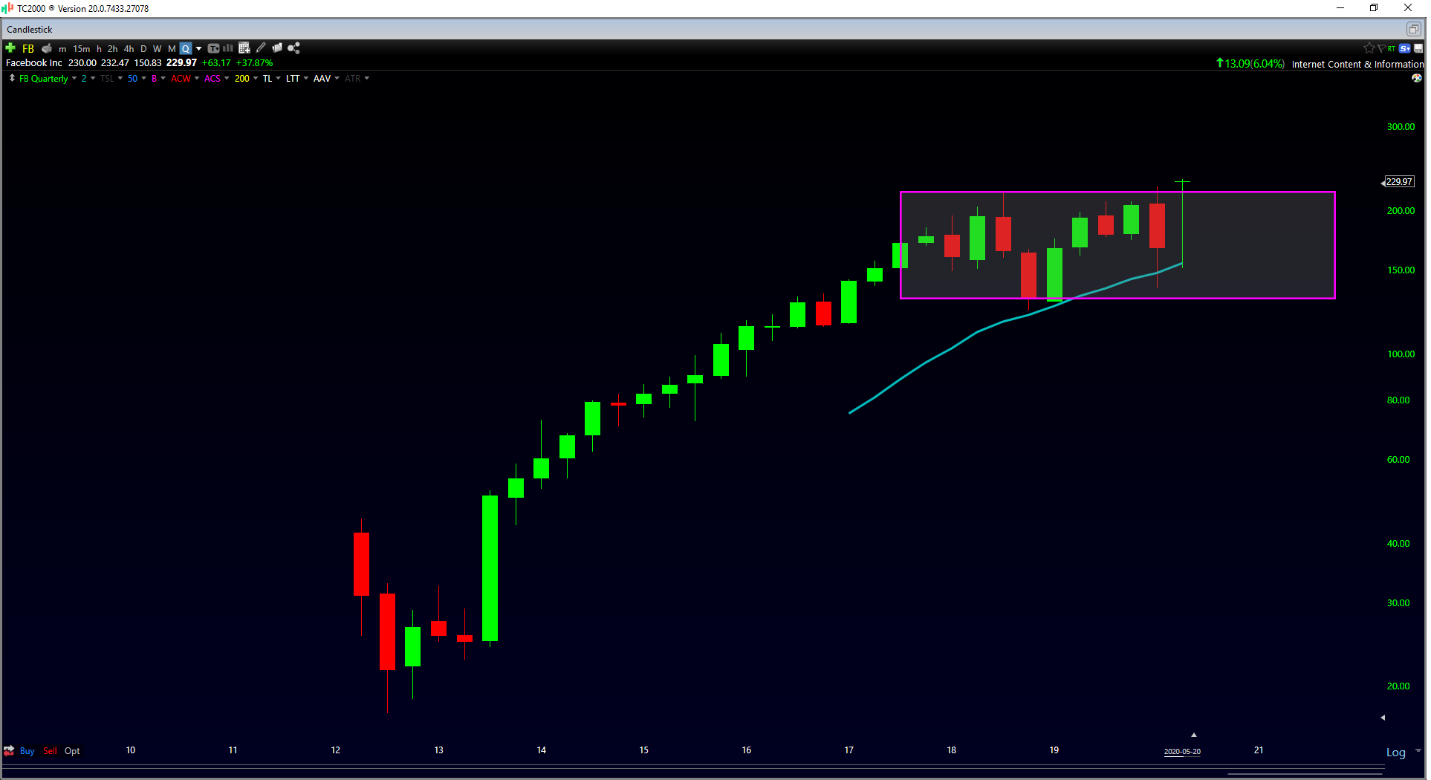

(Source: YCharts.com, Author’s Chart)

If we take a look at Facebook’s technical picture, there’s a lot to like here, with the company building a multi-year base while it digested the earnings drop, but now emerging through the top of this base. Typically, multi-year bases in the tech juggernauts provide solid buying opportunities, as we saw with Netflix (NFLX) and Amazon earlier this year, and I would expect this breakout to be no different for Facebook. While I would not be in a rush to chase the stock above $230.00 per share, I believe any pullbacks below $206.00 would provide lower-risk buying opportunities. Assuming the stock could pull back to this level, it would be trading at below 25x forward earnings and would move from more oversold, from a current slightly overbought condition.

(Source: TC2000.com)

While it’s undoubtedly been a stock-picker’s market year-to-date, with several landmines that have blown up on investors, I believe the key is to stick to the proven names that are the least disrupted by this pandemic. When it comes to FB and DOCU, both companies boast exceptional earnings growth and strong technical charts, and the latter has seen an accelerated trend towards its product’s adoption due to its social distancing initiative. Therefore, for investors looking to add exposure to this market, I believe DOCU and FB provide exceptional opportunities, as long as investors are mindful and take advantage of dips, vs. chasing these names up here. As noted above, the $206.00 level on Facebook, and the $105.00 level on Docusign, would represent what I believe to be lower-risk buy-points.

Disclosure: I am long Docusign (DOCU)

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “BUY THE DIP” Growth Stocks for 2020

7 “Safe-Haven” Dividend Stocks for Turbulent Times

FB shares were trading at $234.69 per share on Thursday afternoon, up $4.72 (+2.05%). Year-to-date, FB has gained 14.34%, versus a -7.64% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| FB | Get Rating | Get Rating | Get Rating |

| DOCU | Get Rating | Get Rating | Get Rating |