We’ve seen a violent correction in the Gold Miners Index (GDX) over the past six months, and few names have managed to evade 25% plus corrections, except for a couple of names that were snapped up in M&A by peers. This significant pullback has led to despondence in the sector, with many investors throwing in the towel, others out of ammo to keep buying, and some leaving the sector for good in search of greener pastures.

This shift from extremely bullish sentiment to a complete dearth of bulls could be providing an opportunity for long-term investors to get in at dirt-cheap valuations, with some miners like Newmont (NEM) offering a dividend yield that’s 150% higher than the S&P-500. In this article, we’ll look at three names that stand out among their peers, which not only pay dividends but also trade at very reasonable earnings multiples currently:

(Source: TC2000.com)

The Gold Miners Index has long been known as a sector where capital goes to die, and it’s been an accurate assessment given the amount of shareholder value that was destroyed in the prior bull cycle. Fortunately, the survivors from the prior bull cycle have learned from the mistakes of other companies and have adopted a much more conservative and shareholder-friendly approach this time around by avoiding over-priced M&A and abnormally capital-intensive projects, focusing on free cash flow and letting go of higher-cost non-core assets.

This pivot in strategy has already begun to pay off for several miners, with names like Newmont and Barrick extinguishing their net debt and already returning value to shareholders through dividends and buyback. The three names we’ll focus on today are Newmont, SSR Mining (SSRM), and Royal Gold (RGLD), which offer investors a mix of high yield, high growth, and high margins.

Beginning with Royal Gold, the company had a strong year in FY2020 with record revenue of ~$499MM, from sales of ~320,000 attributable gold-equivalent ounces [GEOs]. While FY2020 production was down slightly year-over-year, this was solely due to disruptions at some of its partner’s sites due to COVID-19. These issues have since been resolved, and RGLD is getting ready for its next phase of growth, with the massive Khoemacau Mine in Botswana set to come online later this year.

RGLD holds an 80% silver stream on the project, and this translates to more than 1.5MM ounces of silver per year delivered to RGLD, or more than ~$30 million in revenue at current metals prices. This bump in RGLD’s annual attributable GEO sales combined with higher metals prices is what’s driving the strong earnings trend we can see below, with annual EPS set to grow more than 60% from FY2020 levels ($3.86 vs. $2.38).

(Source: YCharts.com, Author’s Chart)

At a share price of $103.00, it’s understandable that some investors might think RGLD is expensive, given that it’s trading at more than 26x FY2022 annual EPS estimates. However, RGLD is not a traditional miner; it’s a royalty/streaming company that does not have a capital-intensive business as most miners do, and it enjoys extremely high margins. This is evidenced by RGLD’s 75% plus margins on a trailing-twelve-month basis, which were more than 3500 basis points above the average miner.

With higher metals prices in FY2021 on average expected in FY2021, RGLD’s margins should improve closer to 80%, and 80% margin businesses can easily justify an earnings multiple of 40. In fact, RGLD has typically traded at an earnings multiple above 40, which makes the current earnings multiple of 26 look very cheap. Therefore, for investors looking for a low-risk way to play the sector, RGLD is a solid choice if it dips back below $100.00 per share.

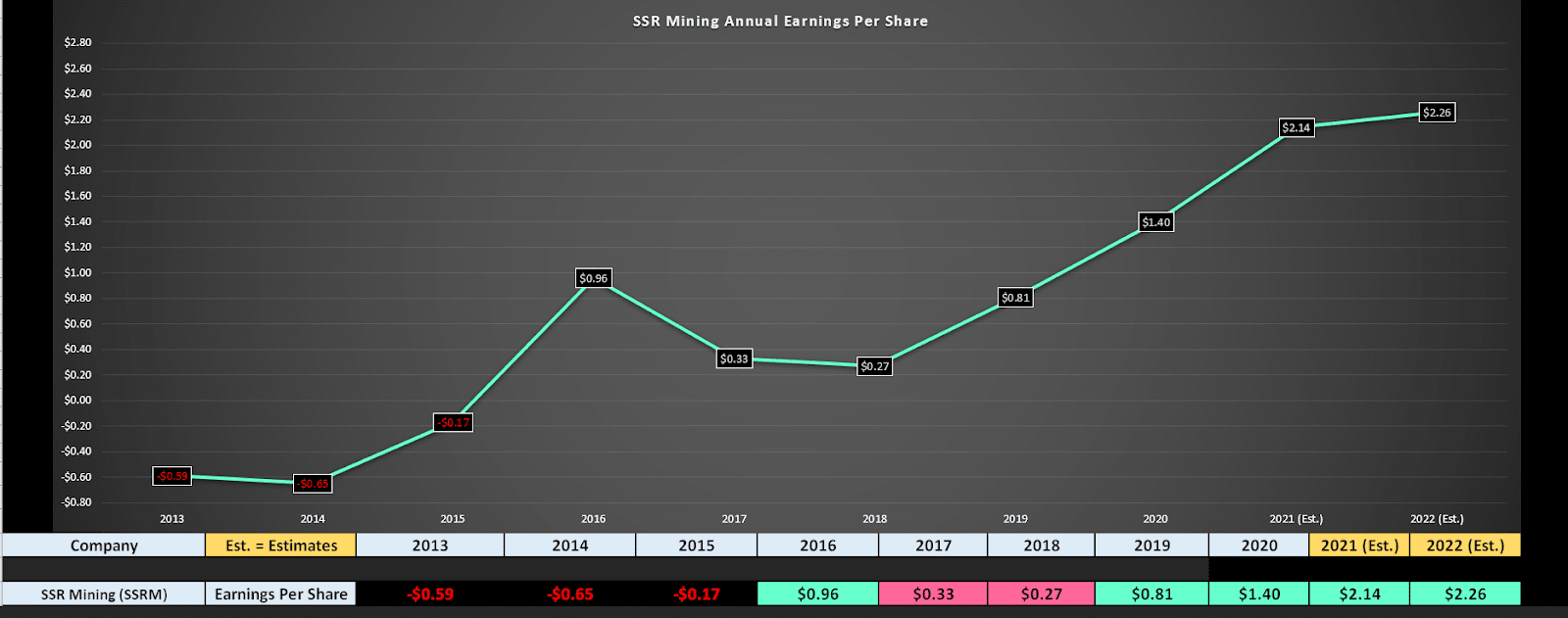

The next name on the list is small-cap miner SSR Mining (SSRM), a company that transformed itself with a major acquisition of a Turkish gold mine last year. This deal helped SSR Mining to nearly double its annual GEO production from FY2019 levels (422,000 GEOs), with Alacer’s Copler Mine in Turkey expected to produce over ~260,000 ounces of gold per year. While the mine isn’t massive and is only a Tier-2 operation, Copler has an enviable reserve base of nearly 4MM gold ounces, translating to a more than 13+ year mine life. In a sector where it’s difficult to find miners with 10+ year mine lifes lies due to declining grades, Copler is an exceptional asset that’s made SSRM much more attractive.

(Source: Author’s Chart)

If we look at SSRM’s earnings trend below, we can see that the company expects to report annual EPS of $2.14 in FY2021 and $2.26 in FY2022. This would translate to more than 60% annual EPS growth between FY2020 and FY2022, and there is considerable upside in these estimates if the gold price heads back above $1,850/oz. However, even assuming the company only meets these estimates, SSRM Mining is trading at barely 6x FY2022 EPS projections at a share price of $14.20.

This is an extremely low multiple for a company with multiple operations, even if SSRM is a slightly higher cost producer, with all-in sustaining costs above $1,000/oz. I see a fair earnings multiple for SSR Mining of 9 to account for its higher costs and riskier jurisdiction in Turkey, which translates to a fair value of $20.34. Therefore, the stock offers solid upside from current levels.

(Source: YCharts.com, Author’s Chart)

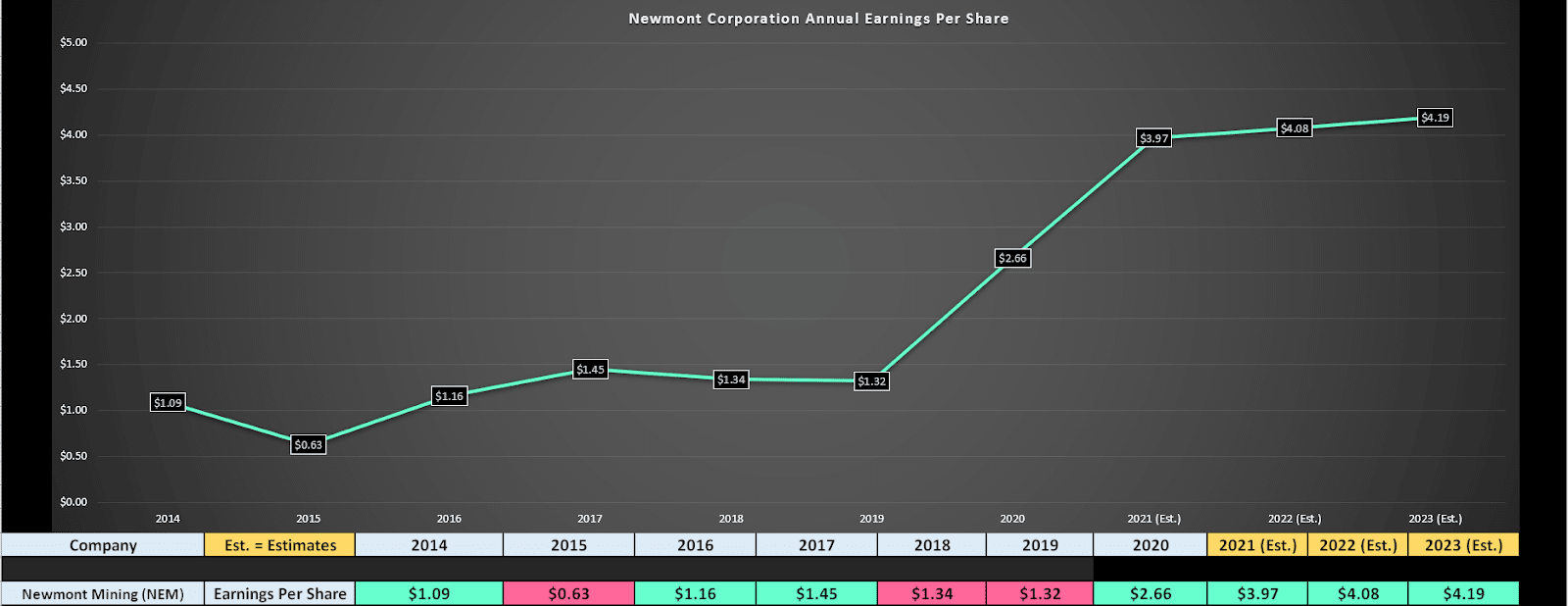

The final name on the list is Newmont (NEM), a more well-known name given that it’s the only gold producer in the S&P-500. Newmont is also the world’s largest gold producer, and the company just came off an exceptional year, generating more than $3.5BB in free cash flow. This gave the company the confidence to more than double its dividend to $2.20 per share, which translates to a 3.70% yield at current levels.

The major distinction for NEM is its investments in technology and safety track record, with NEM being the first miner to invest heavily in automation, with its Boddington Mine in Australia set to become the world’s 1st million-ounce autonomous gold mine. This should pay off massively for NEM over the long run, especially as it fits more operations with this technology, with margins likely to increase substantially after the initial high capital investment in new equipment. During FY2020, NEM’s all-in sustaining costs came in at just above $1,000/oz, translating to 40% plus all-in sustaining cost margins.

(Source: YCharts.com, Author’s Chart)

Looking ahead to FY2021, Newmont is expecting a much stronger year with margin expansion due to higher gold prices and increased production after lapping disruptions at some operations last year. Based on FY2021 annual EPS estimates, NEM is expecting to increase annual EPS by over 48% year-over-year to $3.97. This is an incredible earnings growth rate relative to the average S&P-500 company, yet NEM trades at a huge discount to the market, sitting at an earnings multiple of less than 15 currently. It’s important to note that these estimates look quite conservative if the gold price can get back above $1,850/oz. A fair earnings multiple for the stock given its 50% plus margins is closer to 20, which would leave the stock valued closer to $80.00 per share. Therefore, at a current level of $59.00, the stock looks like a great combination of growth and value.

While miners typically trade at a deep discount to other stocks due to their cyclical business, the whole sector looks far too cheap, even accounting for this discount. Therefore, for investors looking to diversify, now looks like an opportune time to begin buying. Currently, I see the safest and best bet as NEM, given its low earnings multiple, nearly 4.0% yield, and potential to increase its yield to more than 7% from current levels at a $2,200/oz gold price. While a gold price this high might not seem likely and is certainly not the base case, it offers incredible upside for investors getting in after a 25% correction at current levels.

Disclosure: I am long NEM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

How to Ride the NEW Stock Bubble?

NEM shares were trading at $59.62 per share on Thursday morning, down $0.75 (-1.24%). Year-to-date, NEM has declined -0.45%, versus a 3.53% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| NEM | Get Rating | Get Rating | Get Rating |

| SSRM | Get Rating | Get Rating | Get Rating |

| RGLD | Get Rating | Get Rating | Get Rating |