In Part 1 of this series, I explained the research behind the scary idea that the tech-laden Nasdaq could fall as much as 30% off its highs due to rapidly rising interest rates.

(Source: MarketWatch)

I also explained why, according to a study from Lipper Financial, the reality of inflation expectations means that such a severe 30% tech bear market is highly unlikely.

That’s not to say that unlikely things can’t happen. The 2020 pandemic was unlikely in any given year, and look at how dramatic last year was for stocks.

However, the fact is that the relationship between interest rates and stocks, including fast-growing tech names, is far more complex than many in the financial media might have you believe.

Interest Rates Don’t Matter: Fundamentals Do

During the four rising-rate periods that saw the least yield curve steepening, as measured by the difference between 10-year and 3-month Treasury yields, S&P 500 Index returns were weaker than for a typical period, averaging an annualized 3.5%. In the four periods when the yield curve steepened the most, the S&P 500 averaged an annualized 14.5%.” – Lipper Financial (emphasis added)

According to LPL’s research, from the 1960s through 2020 when the yield curve was steepening the most stocks did almost 5X better than when it steepened the least.

(Source: Ben Carlson)

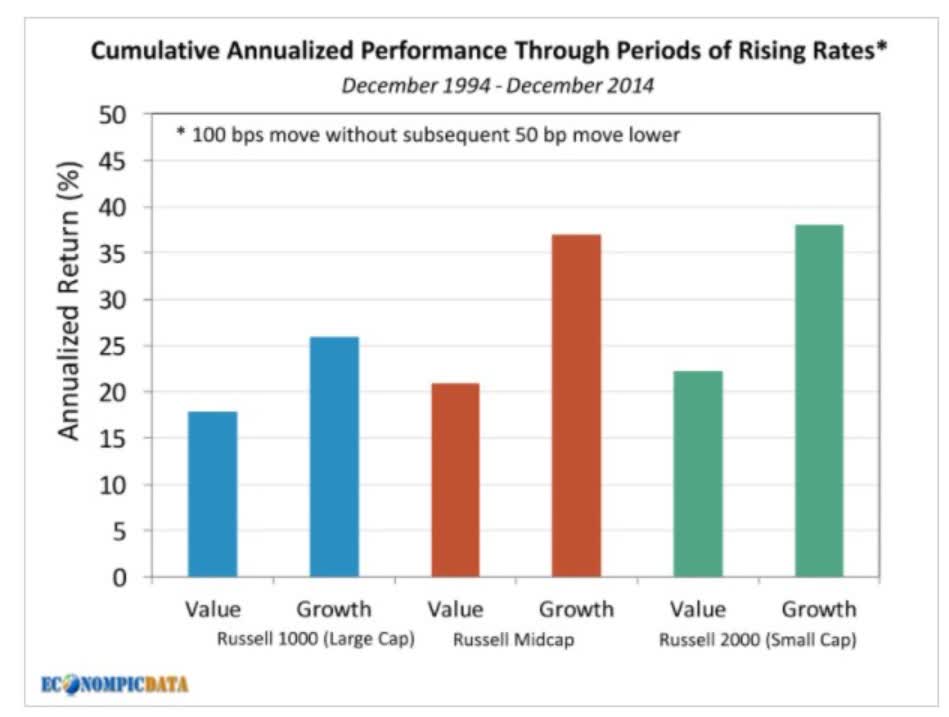

Data from Ritholtz Wealth Management also found that from 1004 through 2014, rising rates proved good for all stocks, even large-cap growth.

Why is that?

- a steepening yield curve = economic optimism

- because long-term rates are rising faster than short-term rates

The Fed, via the Fed Funds Rate, has strong control over short-term rates. But long-term rates? Those are primarily a function of economic forecasts and inflation expectations.

Today the Fed has repeatedly said that it will never again raise rates simply because unemployment is low.

- it will wait to see actual inflation rather than try to head off inflation just because its models say it should be coming

- the Fed’s new approach is based on data, not merely risks of what MIGHT happen

The bond market has become somewhat skeptical of the Fed’s repeated claims that it isn’t worried about an overheating economy. But guess what? That skepticism is what’s creating incredible long-term investment opportunities right now.

That’s because rising rates are, without statistically GOOD for stocks, because it means a strong economy and strong earnings growth.

- from 2020 through 2023 the FactSet bottom-up consensus is for about 60% earnings growth

- the strongest growth in a decade

We also can’t forget, that rates are up big, but off the lowest levels in history.

An increase from 0.5% to 2% is a lot different on the economy than an increase from 3% to 4.5%.

Rates have been rising but they are still historically low, with the 10-year Treasury yield at the end of February falling into the bottom 2% of all values dating back to 1962.

While it’s true that rates become a bigger burden for businesses, consumers, and governments as they rise, even at current and higher levels rates are still attractive and can continue to support a robust economic rebound.

Looking back again at the different rising rate periods, during the four periods with the highest initial 10-year Treasury yield, the S&P 500 averaged a 2.5% annualized return, while those with the four lowest initial yields averaged 15.4%.

A lower initial yield likely reflects manageable inflation and a Fed that isn’t tightening, but it also represents the added economic support of a still low cost of borrowing even as rates rise.” – Lipper Financial, emphasis added

Lipper finds that if rates are TOO high, then stock returns can indeed suffer. JPMorgan’s research also concludes that 10-year yields above 5%, if combined with rising interest rates, usually mean falling markets.

- though the tech bubble occurred when rates were as high as 7%

- because boom economic growth overcomes even high-interest rates as far as stocks are concerned

But note that Lipper’s study looked at rates as high as 16% back in 1981. If you honestly expect 10-year yields to soar from 1.6% to 5.6% in a matter of months, then yes you might want to worry about short-term corrections.

But ask yourself, why would interest rates rise that quickly when

- the bond market sets long-term rates based on inflation expectations

- the bond market’s medium-term inflation expectations are still within the Fed’s long-term target range

- they have been changing at a very slow rate, over nearly a year

In other words, the catalysts for triggering a 30% Nasdaq bear market, are not actually threatening us right now.

But what if tech stocks just roll over, because enough people believe they will. Or to put it another way, what if millions become convinced a tech bear market is inevitable, creating the exact plunge in growth stocks they feared?

How To Get Rich If Tech Stocks Crash 25%

In 2000 some stocks rose 800%, like Tesla (TSLA). Others fell 50%, like Carnival (CCL). At any given moment it’s always a market of stocks, not a stock market.

However, here’s a highly effective and easy trick to avoid losing a fortune in a future Nasdaq bear market.

- even if one doesn’t happen in 2021 it’s inevitable at some point

That trick is this. Always buy safe companies at safe prices.

- safe companies = above-average quality or better, with strong fundamentals and sound balance sheets

- safe prices, historically fair value, or better

If you never knowingly overpay for a company, you avoid the obvious stupid mistake.

Charlie Munger, Buffett’s right hand at Berkshire for over 30 years, says that the key to their success is consistently being not stupid.

That literally boils down to what Joel Greenblatt calls “buying above-average quality companies at below-average prices.”

Of course, in real life, it’s not quite that simple, but it’s not far off either.

Take the example of Amazon (AMZN - Get Rating), my personal biggest holding.

- I’ve invested over $200,000 into Amazon over the years across all my portfolios

Let’s consider two periods of time when Amazon an obviously stupid mistake and a brilliant low-risk/high-probability Buffett-style fat pitch.

Amazon As An Obviously Stupid Mistake

(Source: FAST Graphs, FactSet Research)

Over 20 years Amazon has grown at hyper-rates as strongly as 70% per year. Yet the market keeps paying 24 to 26X operating cash flow for this company outside of bear markets and bubbles.

- there is a 91% probability that Amazon’s intrinsic value is about 25X cash flow

- since billions of investors, “weighing the substance of this company” to quote Ben Graham, keep paying 25X cash flow

Back in August 2018, right before the big late 2018 recession fear correction began, Amazon was 38X cash flow.

- 52% historically overvalued

Does this mean that everyone buying in August 2018 was an idiot? Actually no.

Back in August 2018, the analyst consensus for Amazon’s long-term growth rate was close to 50%.

- According to Peter Lynch, paying 50X cash flow for a company growing at 50% is still reasonable and prudent

- Peter Lynch is the 3rd greatest investor of all time

- 29% CAGR returns for 13 years

However, this is where market historians gain an edge over the momentum crowd.

- Amazon has never sustained PEGs of 1.0 or higher

- on a cash flow basis AMZN’s fair value PEG is 0.9

- still within Lynch’s reasonable PEG range

But here’s what protects the prudent Amazon investor in August 2018 when Amazonis 52% historically overvalued.

- Amazon growing up to 70% annually still is valued by investors over time, at 24 to 26X cash flow

- so paying 38X cash flow is pure speculation that the multiple will keep climbing

- when it has never done so in the history of the company

John Templeton and Howard Marks are two of the greatest investors in history. And they point out that 80% of the time, mean reversion means that “this time isn’t different”.

20% of the time it is, which explains why the greatest investors in history are right 60% to 80% of the time. 20% of the time the past can’t help you understand the future, but 80% of the time it can.

(Source: FAST Graphs, FactSet Research)

- In early 2016 Amazon was trading at the same valuation it is now, 23.6X blended cash flow

- A wonderful hyper-growth company at a good price

- investors have earned 37% CAGR total returns since then

(Source: FAST Graphs, FactSet Research)

AMZN is expected to see a few years of slower growth, resulting in JUST 18% annual consensus return potential through 2023.

(Source: F.A.S.T Graphs, FactSet Research)

Which is about 45X more than that of the 36% overvalued S&P 500.

The bottom line is this.

- if the economy grows fast enough to cause interest rates to rise above the 2% to 3% long-term range economists expect, it means Amazon is likely thriving like never before

- those fundamentals will put a floor under the stocks

- AMZN is extremely unlikely to fall to a blended P/OCF of under 18 in a roaring economy

- which is what a 25% decline in Amazon from here would represent

Amazon hasn’t traded at sub 18X cash flow since August 2010

(Source: F.A.S.T Graphs, FactSet Research)

That’s not to say that the market can’t potentially send Amazon down to P/cash flow multiples that are outrageously low. But the last time Amazon traded under 18X cash flow investors who bought and held, made almost 25X of their money over the next 10.5 years.

Basically, Amazon is exactly the kind of fat pitch-safe blue-chip you can buy today.

Safe doesn’t mean “can’t fall a lot if the Nasdaq crashes”. But it does mean that 5+ years from now you’re very likely to be sitting on very impressive returns that make you seem like a genius.

When in reality all you did was make “consistently not stupid” decisions.

Want More Great Investing Ideas?

How to Ride the NEW Stock Bubble?

9 “MUST OWN” Growth Stocks for 2021

5 WINNING Stocks Chart Patterns

SPY shares were trading at $388.02 per share on Friday morning, down $3.46 (-0.88%). Year-to-date, SPY has gained 3.78%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Adam Galas

Adam has spent years as a writer for The Motley Fool, Simply Safe Dividends, Seeking Alpha, and Dividend Sensei. His goal is to help people learn how to harness the power of dividend growth investing. Learn more about Adam’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| SPY | Get Rating | Get Rating | Get Rating |

| AMZN | Get Rating | Get Rating | Get Rating |