I think we can all agree that becoming wealthy is a dream shared by most, if not all people. As Woody Allen once said, “money is better than poverty, if only for financial reasons.”

But whether you dream of living it up in a Miami Beach penthouse, or merely being able to enjoy a comfortable retirement, here’s the biggest mistake that a lot of investors make in their quest to become financially independent.

Getting Rich Quickly is Often a Curse, Not a Blessing

I’m a huge fan of the TV show “Shark Tank” where self-made millionaires and billionaires (the Sharks) get pitched investing ideas by entrepreneurs from all over the country.

Recently in one episode Charles Barkley, the famous NBA star (now retired) and a legendary venture capitalist, said something that shocked me. He said that 80% of NBA players end up going broke.

After looking into it, I found that Mr. Barkley was wrong, but not off by much. According to CNBC

- 60% of NBA players go broke within five years of retiring

- 78% of NFL players go broke within TWO YEARS of retiring

And it’s hardly just professional athletes that end up squandering incredible income and winding up in the poor house. Here’s 16 year NBA veteran Chris Dudley (who played for five different teams) to explain

“During my 16-year NBA career, I saw newly retired teammates lose everything to financial schemes and scams, dishonest or unqualified advisors, and reckless spending only a few years after leaving the league. Since starting a second career as a financial advisor more than a decade ago, I’ve seen this storyline repeat itself again and again — with high-net-worth individual investors, as well. Not a month goes by without seeing a headline describing the latest riches-to-rags story in professional sport.”

But sadly, the curse of “riches to rags” isn’t just the realm of the celebrity or professional athlete. A recent survey by the investing app STASH found that 59% of Millenials thought that playing the lottery was a good retirement plan. Ironically enough, 31% of all Americans don’t invest in the stock market, in any way, shape or form, because they consider it “too risky”.

The sad thing is that these same people, who see a Powerball or Mega Millions ticket as their best hope of reaching their financial dreams, don’t realize that, even if they “got lucky” and did win, chances are they could soon come to regret “hitting it big”.

Getting Rich Isn’t Enough, STAYING Rich Is the Real Goal

According to a study of 3,200 ultra-high net worth families by the Williams Group Wealth Consultancy, 70% of family fortunes are wiped out by the second generation, and 90% by the third. In other words, the millions or even billions that the first generation spent a lifetime amassing, are typically totally squandered by those who didn’t have to earn it, and thus have little respect for the rules of money.

And remember all those Millenials who were hoping that a lottery jackpot might put an end to their retirement fears? Well while it’s not true that most lottery winners go bankrupt within five years, according to The National Endowment for Financial Education lottery winners do go bankrupt more often than most Americans. And according to the Consumer Financial Protection Bureau, 33% of lottery winners eventually declare bankruptcy.

To understand why we need only realize the link between lottery winners, professional athletes, celebrities, and the ultra-wealthy, most of who end up losing their family fortunes. It’s a lack of respect for the important habits that allowed for the accumulation AND preservation of lots of money in the first place.

Money can be thought of as a working battery and thus a source of power. Let’s say I start a business making a product that meets a previously untapped but important consumer need. I sell millions of these devices, to people all over the world, who had to work hard for that money and value the convenience and life-improving nature of my product.

These people trading their money for my product is how I ultimately amass millions or even billions of dollars, which is nothing more than the combined work of all these people (plus myself in growing my business to bring it to market). The energy a battery stores can be used to power many things, and in the same way money is a form of power because it can be used to purchase the labor or services of lots of other people.

But, as Spider Man’s uncle Ben famously said: “with great power comes great responsibility.”

That’s the thing that people don’t realize about money, that’s it’s a tool that must be used wisely. Great self-made business people have to learn the hard way the true value of money and learn from the inevitable mistakes they make growing their businesses and overcoming various challenges.

Similarly, self-made investing millionaires, whose only business is their portfolios (a holding company that owns income-producing assets like stocks/bonds) will typically make plenty of mistakes along the way to amassing a large nest egg. It’s learning from these painful experiences that not just allows these investors to get rich, but to stay rich.

And let’s not forget that just as with any powerful tool, there are plenty of downsides to money too, which also explains why it’s so easy to lose a fortune far quicker than earn one.

As Shark Tank’s Daymond John says “money can’t solve your problems, just drive you up to them in a Bentley”.

According to Michael Cole, the president of Ascent Private Capital Management at U.S. Bank, “Wealth often breaks down family trust and relationships”. That’s not surprising given that, according to a study by Ramsey Solutions, 21% of all divorces (the second biggest cause) are over money issues (infidelity is the #1 cause).

Cole estimates that poor communication and lack of trust is why 60% of family fortunes get wiped out. 25% is from lack of financial preparation (ie financial illiteracy) and 10% from a lack of shared vision (ie everyone wants to overspend on their own desires). Mr. Cole gave one example that fits perfectly with our theme today.

He had one client who amassed $100 million over his lifetime, by living frugally, working hard at the business he started, and his family had no idea they were actually rich. When he died this client left $100 million to his three daughters, who he had never told would become some of the richest people in the world one day. What followed was a “feeding frenzy” where the entire family fought like rabid dogs to get a cut of the booty, and within a few years, the money was all gone.

As one frequent guest Shark (Alex Rodriguez) likes to say, to be successful it helps to have a Ph.D. from the school of hard knocks, with Ph.D. standing for “poor, hungry and desperate.”

By which he means that starting out from nothing and having to earn every dime (and avoid losing it or at least learning from when you mess up and do) is how you’ll learn how to respect the power and value of money, and thus become most likely to amass a lot of it.

I’m no stranger to financial mistakes and poverty. I picked the wrong spouse and made plenty of mistakes that left me poverty stricken for several years. We had our utilities shut off (all of them) several times and once things got so tight I went a month without food (I lived off only mustard, water, and pickle juice).

But it was precisely those experiences that taught me incredibly valuable lessons about money including

- Money is a powerful tool that must always be respected

- Money = financial flexibility and security

- Money doesn’t solve all problems (indeed it causes ones all its own) BUT is essential to keeping you from making desperate and often suboptimal decisions (like being forced to take out payday loans in order to eat)

- Spending unsustainably CAN’T generate happiness (because you know you’ll eventually have to stop and your standard of living will get squeezed immensely)

- Being on a sustainable/high probability path to long-term wealth is far more fulfilling than driving a BMW (we did) or eating out at fancy restaurants three times a week (we did that too).

When my marriage finally imploded (after we lost our fifth baby, which set in motion many other horrible things) I was cleaned out in the divorce. My net worth was -$50,000, my income was $20,000 (all from my Army pension) and I felt shattered and like I’d wasted the last five years of my life.

Within three years of committing myself to rebuild my life, including finances, health, and career, I’ve managed to increase my annual income (from 27 different sources) to $192,000 (top 6% of all Americans) and my net worth to $257K (top 10% of my age group and top 32% of all Americans).

Most importantly, because I’ve been both rich (well I feel rich at least, relative to those dark days in Alabama) and poor, I know the mistakes to avoid that will keep my hard earned money safe and working for me in low-risk/high probability investments where it can grow exponentially over time.

That’s why, even though my income has grown almost 10 fold in three years, I maintain a very lean lifestyle (90% post-tax savings rate). That way I can afford to save most of what I make (working 12 hour days six days per week) and invest it into my retirement portfolio that’s now 100% low-risk blue-chip dividend stocks.

That portfolio is paying me $13,172 per year (about $1,100 per month) and those dividends are growing at double-digits (13.8% CAGR over the last five years).

What about total returns? Well, I also care about those but here’s the thing. As my biggest winners show, you don’t have to make crazy risky bets with your money. My biggest winners include dividend aristocrat A.O Smith (25 consecutive years of dividend growth).

AOS I bought for the first time in the late 2018 correction, telling my readers that this industrial blue-chip was trading at the best valuations in over five years due to China trade war and 2019 recession fears (that were way overblown). I bought an initial position, and then doubled down when it fell even lower. I didn’t catch the exact bottom, but market timing is a fool’s errand and my only goal is to follow the Warren Buffett approach of buying great companies at good to great prices.

I bought AOS at a great price, and now am sitting on a nearly 30% total return including dividends after just six months. Illinois Tools Works, a dividend aristocrat with 44 straight years of dividend growth to its credit, was bought at the same time as AOS, and for the same reasons.

The Street was obsessed with what a trade war and possible recession might mean for 2019 and 2020 earnings. I made the low-risk/high probability bet that this proven winner would keep on winning over the long-term and thus the lowest valuation in over five years was probably a good time to buy. Now, six months later my total return is 28%.

Apple, BlackRock and Texas Instruments were all similarly low-risk “fat pitch” blue-chip buys. Each one had plausible short-term risks that bears said made them “dead money” or likely to keep falling. I didn’t try to time the bottom, just bought them at their best valuations in five to 10 years and am up handsomely as a result.

My biggest winner of all, EPR Properties, I bought in early 2018, at the end of a two year REIT bear market. The market absolutely HATED EPR because of two popular memes on the Street. First, fears that rising rates would hammer REITs because they were treated as “bond alternatives” for so many years, and second movie theaters were dying (theaters make up about 35% of the REIT’s rents).

I knew that REITs are actually not at all like bonds and that EPR’s theaters were some of the best in the country (it owns 3% of the theaters in North America which bring in 7% of all box office income). So I bought EPR at a 7.5% yield that two dividend hikes later means I’m getting 8% of my investment back each year in a safe monthly dividend.

For context, the market’s historical return is 9.1% meaning that within a few years (EPR is growing the dividend 4% per year) I’ll be earning market-beating returns from safe dividends alone. And in the meantime, I’m sitting on a 45% total return in about a year.

Basically, I’m saying that my days of wild-eyed gambling (I’ve tried everything from day trading currencies to speculating in naked options at high leverage) are done. There is no need to try to hit a grand slam when the much less risky and more likely road to riches is in safe dividend stocks.

I just need to buy them when the market hates the most, which is why I recently invested $28,000 into four blue-chip healthcare stocks. One of those was UnitedHealth, which I manage to pay about 14 times cash flow for an industry leading giant, who is growing earnings at about 13% over the long-term (including 14% in 2019 per management guidance and 23% in Q1 2019).

That $6,000 investment, representing 2.5% of my net worth, is a low-risk/high-probability bet that UnitedHealth is a great Buffett style blue-chip buy, and that will deliver 13% to 20% annualized total returns over the next five years.

With the market frequently offering low-risk/high probability opportunities to earn 10% to 25% five-year total returns in dividend paying blue-chips, who needs high risk “swing for the fences” gambling such as in cryptocurrencies? Will I be wrong? Sure, plenty of times. But even legendary investor Peter Lynch, who delivered 29% CAGR total returns from 1977 to 1990, said: “in this business, if you’re good you’re right six times out of 10.”

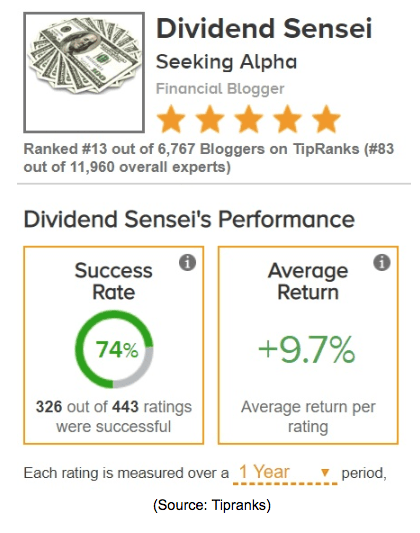

Well since I started writing at Seeking Alpha, my recommendations, at least on a forward 12-month basis, are right 74% of the time, with the average recommendation (including the “wrong ones” up 9.7%, better than market’s historical norm).

The more I focus on low-risk blue-chips trading at great prices (and no longer recommend high-risk stocks) the better my success rate gets. More importantly for me, the better my retirement portfolio returns become, overcoming my early and very costly mistakes (at one point I was down $20K in realized losses, now I’m up $19,000 since inception).

Bottom Line: Getting Rich Slowly Is the Easiest and Highest Probability Path to Financial Independence

Don’t get me wrong, I’m a classic American entrepreneur, with huge ambitions, one of which is to break into the top 1% of income earners and also by net worth. Or, as Shark Tank’s Kevin O’Leary (aka “Mr. Wonderful”) would say “I want to become stinking, filthy rich.”

But I’m also a student of market history, and more importantly, human nature. I know that the biggest curse many “lucky” people face is getting rich too quickly. While massive windfalls might seem like a wonderful thing, never forget that many people who obtain a mountain of money end up losing it.

That’s because, as the saying goes “a fool and his money are soon parted.” Obtaining large wealth isn’t easy, because to become rich you don’t just have to earn millions, more importantly, you have to keep it too.

I’ve frequently described an investment portfolio as a business, but the truth is that your entire life is like a business. And just like any large business venture, it takes time, discipline, and a lifetime of learning from your mistakes to succeed.

While many might seek that elusive “get rich quick scheme” out of either greed or desperation, the truth is that the habits that let self-made billionaires become legends are the same ones you and I can use to obtain financial independence.

- Work hard (grind for as long as it takes to succeed)

- Learn from your mistakes (try not to make the same mistake twice)

- Live beneath your means (the lower your expenses the safer you can invest and still achieve your financial goals)

- Remember Buffett’s two rules of investing “rule #1, never lose money, rule #2, never forget rule #1)

- Learn to love the journey as much as you look forward to the destination (patience and discipline are two of the most crucial factors to long-term success)

As someone who has been investing for 23 years, I’ve tried every “get rich quick” scheme there is. What I’ve learned is that the biggest mistake investors make is not respecting what money truly is (power) and thus forgetting that as Spider Man’s uncle Ben “with great power comes great responsibility”.

Ultimately, the real trick to becoming rich is that it’s easy to do IF you know what approach to take, and set yourself up for success. That means not reaching for outlandish returns via super high-risk strategies (trying to hit grand slams) but accepting the time tested lessons that the best investors in history, as well as dozens of studies, have shown us.

Consistent savings, into high-probability investments, like undervalued dividend paying blue-chips, is ultimately all you need to become financially independent, as long as you enough time, discipline and patience. Because, like Warren Buffett, the greatest investor of all time famously said

“Wall Street is designed to transfer money from the active to the patient.”

About the Author: Adam Galas

Adam has spent years as a writer for The Motley Fool, Simply Safe Dividends, Seeking Alpha, and Dividend Sensei. His goal is to help people learn how to harness the power of dividend growth investing. Learn more about Adam’s background, along with links to his most recent articles. More...

9 "Must Own" Growth Stocks For 2019

Get Free Updates

Join thousands of investors who get the latest news, insights and top rated picks from StockNews.com!

Top Stories on StockNews.com

Best & Worst Performing Mega Cap Stocks for July 10, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 9, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 8, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.

Best & Worst Performing Mega Cap Stocks for July 7, 2025

AEXAY leads the way today as the best performing mega cap stock, closing up 13.49%.